https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

969 | P a g e

e-ISSN: 2715-4203, p-SSN: 2715-419X

DOI: https://doi.org/10.31933/dijdbm.v4i5

Received: 16 June 2023, Revised: 19 July 2023, Publish: 23 August 2023

https://creativecommons.org/licenses/by/4.0/

Factors that Influence Intention to use Mobile Banking

Steffi Odelia Setiawan

1*

, Dipa Mulia

2

1 Faculty of Economics and Business Mercu Buana University, Jakarta, Indonesia,

55121110047@student.mercubuana.ac.id

2

Faculty of Economics and Business Mercu Buana University, Jakarta, Indonesia

,

dipa.mulia@mercbuana.ac.id

*

Corresponding Author: Steffi Odelia Setiawan

Abstract: The increase in internet penetration in Indonesia which has reached 77.02% is not

in line with the growth of Bank Mandiri mobile banking users to the number of customers

which is still low. This study evaluates perceived ease of use, trust, compatibility, security, and

convenience on intention to use m-banking with the mediation of perceived usefulness. This

study distributed online questionnaires collected through social media and obtained 210

respondents in the Jabodetabek area. This research method uses quantitative with the Partial

Least Square (PLS) - Structural Equation Modeling (SEM) method using the Smart PLS 3.0

program. The results state that perceived usefulness affects intention to use m-banking,

perceived ease of use and trust affect perceived usefulness. Perceived usefulness variables can

mediate perceived ease of use and trust in intention to use m-banking.

Keywords: Perceived Ease of Use, Perceived Usefulness, Trust, Compatibility, Security,

Convenience, Intention to Use Mobile Banking

INTRODUCTION

The Indonesian Internet Service Providers Association (APJII) states that in 2021-2022

there will be 210.03 million internet users. Until the 2021-2022 period, the internet penetration

rate in Indonesia has reached 77.02% of the total population of 277.7 million people. Until

finally, several sectors are competing to be able to renew services into digital services,

including the banking sector. Mobile banking is a banking transaction service through a digital

application that has various features that can be used to make various kinds of payments such

as transfers, balance checks, create accounts or other financial transactions such as buying

electricity tokens, topping up credit, and refilling electronic cards only through smartphones

(Styarini et al. 2020). In order to provide better services, banks in Indonesia continue to make

innovations to improve customer convenience in using mobile banking. Some banks present

more up to date m-banking starting from 2019 by presenting a variety of new features so that

customers can transact, create accounts, invest, and other activities with just one application.

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

970 | P a g e

Fig 1. Data on the percentage growth of BCA, CIMB, BNI, BRI, Mandiri m-banking users to the total

number of customers.

Based on the figure above, the percentage increase in internet penetration in Indonesia,

which has reached 77.02%, the growth of m-banking users compared to total customers at

Mandiri bank is still relatively low. With the various advantages offered by banks through m-

banking services and the costs and efforts that have been made in creating mobile banking

services, it should be able to attract customers and user market penetration in a short time

(Amihsa et al. 2020). The low growth of mobile banking users compared to total customers at

Bank Mandiri, of course, is based on customer interest in determining to use m-banking.

Therefore, to be able to increase users of the Mandiri Livin App, it is necessary to know the

factors that influence intention to use mobile banking.

LITERATURE REVIEW

Technology Acceptance Model (TAM)

The Technology Acceptance Model (TAM) was introduced by Davis in 1989 which is a

behavior used to explain individual acceptance of the use of information technology systems

(Davis 1989 in Amihsa et al. 2020). The TAM model itself is an adoption of the Theory of

Reasoned Action (TRA) model which is a theory of reasoned action with a premise that an

individual's reaction and perception of something can determine that person's attitude and

behavior so that the user's reaction and perception of information technology (IT) will affect

the attitude in accepting the technology.

In TAM, there are factors that influence acceptance in the use of technology, namely

perceived usefulness (PU) which is explained as a perception of the benefits of technology

which is used with the aim of benefiting and perceived ease of use (PEOU), namely the

perception of using technology.

Preceived Usefulness

According to Davis (1989), perceived usefulness is the degree of trust in a technology

that can improve one's performance and productivity. Perceived usefulness is described as a

benefit for users related to productivity, work effectiveness, performance, and

overallusefulness (Handayani, 2007 in Atarwaman 2022).

Preceived Ease of Use

Perceived ease of use is defined as individual belief that using a technology does not

require great effort (Davis, 1989 in Wahyudi and Yanthi 2021). According to Wibowo (2017),

perceived ease of use is a person's level of belief that a technology is easy to understand and

2019 2020 2021

BCA

42,60% 61,30% 65,30%

BNI

17,42% 17,35% 17,14%

BRI

4,23% 10,22% 10,90%

Mandiri

3,90% 8,65% 12,89%

CIMB

32,50% 34,30% 35,70%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

971 | P a g e

use which can improve one's work performance. According to Kim et al. (2015) that ease of

use is felt when consumers believe that using m-banking services is easy and does not require

more effort to learn.

Trust

According to Mowen and Minor in Donni Juni (2017) Trust is all the knowledge

possessed by consumers and all the conclusions that consumers have made regarding objects,

attributes and benefits. Trust is one of the important aspects of business relations, with trust

there will be a commitment between the two parties. Ba and Pavlou (2002) explain that trust is

an assessment of one's relationship with others in making certain transactions in accordance

with the expectations of each party in an environment full of uncertainty. Mulia, D, et al (2022)

state that the many products offered by banks make some customers hesitant or afraid to use

online transactions, so banks must be able to convince customers and make them trust and be

willing to adopt and use technology-based products and services continuously.

Compatibility

Compatibility is the extent to which the use of technology is considered consistent with

the values, experiences, and needs of the user (Moore & Benbasat, 1991). According to Wang

et al., (2017) compatibility is how a new technology can match the expertise of the previous

technology that already exists and is related to the technology. If a new technology does not

have compatibility with experience and lifestyle, it will have an impact on the time a person

will spend understanding how to use the technology which will result in wasted time and also

reduce the view of the usefulness of the technology (Gumussoy et al., 2018). The scope of

compatibility in research is a balanced fit between individual needs and better technological

innovation so that when customers realize that m-banking services match their lifestyle and

preferences, customers tend to decide to use m-banking (Muslim, 2022).

Security

Security is a process of preventing risks received from using a service (Kumala et al.,

2020). Security can also be interpreted as protection from various unknown data usage access

(Vemuri and Chen, 2021). According to Whitman and Mattord (2010), security is a form of

protection for information and the important elements in it such as confidentiality, integrity,

and availability, including the system and hardware to store and send the information.

Convenient

Convenience has been defined as "easy to reach; accessible" and "suitable or appropriate

to one's comfort, purpose, or needs". In the context of service encounters, convenience has been

described in terms of lifestyle, not having to travel, personal safety, and not having to wait

(Lichtenstein and Williamson, 2006). Convenience can influence consumption behavior and

service convenience is also seen as instrumental when consumers make service choices and

evaluate company service performance. In regional consumer service research, convenience is

increasingly recognized as a prominent product attribute and as a basis for making purchasing

decisions (Voli, 1998 in Clemes et al. 2012).

Intention to use

According to Davis (1989), interest in use is a user's tendency to be loyal in using a

technology. According to Ahmadi (2009) in Desvronita (2021) interest in use is the user's

interest in using a system, so that it becomes a behavioral tendency to believe and continue to

use the system. Interest in use can be interpreted as a person's desire and interest in behaving

in a certain way which aims to own, dispose of, or use (Wulandari, 2019).

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

972 | P a g e

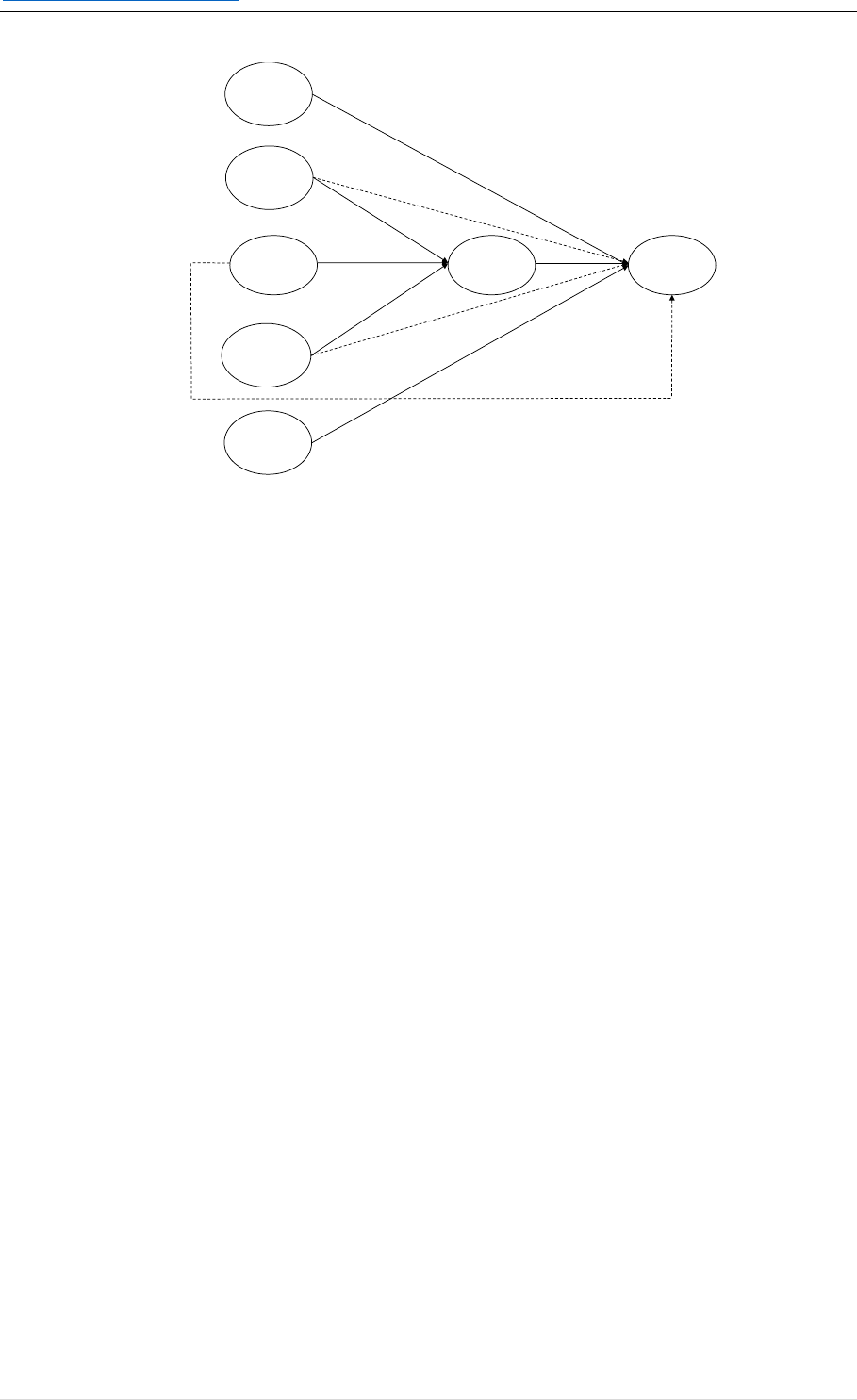

Fig 2. Research Framework

Hypothesis testing aims to test the relationship between variables and analyze the

similarities or differences that might be found. The hypotheses proposed for this study are as

follows:

H1 : Perceived ease of use has a direct effect on intention to use m-banking

H2 : Trust has a direct effect on intention to use m-banking

H3 : Compatibility has a direct effect on intention to use m-banking

H4 : Security has an effect on intention to use m-banking

H5 : Convenience affects the intention to use m-banking

H7 : Perceived ease of use affects perceived usefulness of m-banking

H8 : Trust affects perceived usefulness

H9 : Compatibility affects perceived usefulness

H10 : Perceived ease of use affects intention to use m-banking through mediation

of perceived usefulness

H11 : Trust affects intention to use m-banking through the mediation of perceived

usefulness

H12 : Compatibility affects intention to use m-banking through the mediation of

perceived usefulness

RESEARCH METHODS

This research is a quantitative study to determine causal relationships. The population

studied was Mandiri bank customers who did not use mobile banking, who lived in

Jabodetabek. The sampling technique used was purposive sampling method by using an online

questionnaire distributed through social media. The questionnaire was using a Likert scale with

a range of 1-5 for each indicator. The data collected were 210 respondents. This study used

Partial Least Square (PLS) - Structural Equation Modeling (SEM) with SmartPLS 3.0 software.

FINDINGS AND DISCUSSION

The characteristics of respondents in this study are based on age, occupation and income.

From 210 respondent data, 59.5% were in the productive age category, namely 18-45 years old

and 40.5% in the elderly category, namely over 45 years old. For occupation category, 10.5%

are civil servants, 29% are private employees, then 11.4% are students / students, 31.9% are

H4

H1

H7

H2

H5

H8

H3

H6

H9

Perceived

Ease of Use

Trus t

Compa tibility

Perceived

Usefulness

Intention

to

use mobile

Convenience

Security

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

973 | P a g e

self-employed, and 4.8% are housewives, and those who do not work are 4.8%. For income

category, based on these results, respondents with an income of <Rp. 1,500,000 per month

were 9%. Respondents who have an income of Rp. > 1,500,000 to Rp. 2,500,000 per month

17.1%. 14.8% earn Rp. > 2,500,000 to Rp. 3,500,000 per month. Respondents who have an

income of> Rp. 3,500,000 per month 50.5%. And those who do not have income are 8.6%.

Table 1. Construct Validity anf Discriminant Validity

Variable

Indicator

Outer

loadings

Cronbach’s

Alpha

Composite

Reliability

(AVE)

Perceived Ease

of use

PEOU 1

0.955

0.951

0.969

0.911

PEOU 2

0.966

PEOU 3

0.943

Trust

TRT 1

0.808

0.788

0.873

0.697

TRT 2

0.837

TRT 3

0.858

Compatibility

COM 1

0.905

0.815

0.884

0.718

COM 2

0.878

COM 3

0.751

Security

SEC 1

0.925

0.872

0.912

0.776

SEC 2

0.84

SEC 3

0.875

Convenience

CON 1

0.832

0.815

0.889

0.729

CON 2

0.92

CON 3

0.805

Perceived

Usefulness

PU 1

0.835

0.811

0.887

0.724

PU 2

0.838

PU 3

0.879

Intention to

use

INT 1

0.899

0.805

0.883

0.717

INT 2

0.884

INT 3

0.75

The examination of composite reliability, Cronbach's Alpha and Average Variance

Extracted aims to test the reliability of instruments in the research model. If all latent variables

have reliability or Cronbach alpha > 0.7, it means that the construction is reliable or the

questionnaire used as a tool in this study is reliable or consistent.

Table 2. R Square and Q Square

R Square

Q Square

Perceived Usefulness

0.423

0.282

Intention to use

0.149

0.083

R square is between 0.25 - 0.50, indicating that the model has a weak relationship, while

Q square values greater than 0 indicate that the model has predictive relevance.

Tabel 3. F-square

Variable

Perceived Usefulness

Intention to use

Perceived Usefulness

0.127

Perceived Ease of use

0.18

0.003

Trust

0.07

0.002

Compatibility

0.002

0.000

Security

0.000

Convenience

0.001

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

974 | P a g e

There is a large value of medium influence on the F-Square value of 0.15 in H6. The

other large influence values are small with the F-Square value criterion being at the value of

0.02.

A model will be considered fit if it has an SRMR value below 0.10 or 0.08. The Normed

Fit Index value produces a value of 0 to 1, a good NFI value is a value close to 1. The NFI

value is obtained from 1 minus the Chi-square.

Table 3. Fit Measures

Godness of Fit

Saturated

Model

Estimated

Model

SRMR

0.081

0.083

Chi-Square

816.059

820.159

NFI

0.730

0.728

rms Theta

0.199

From the table above, it can be seen that the model is fit based on the data because the

SRMR is 0.081. Meanwhile, in the Variance Inflation Factor (VIF) table below, none of the

model values exceed 5, so it can be concluded that there is no multicollinearity in the model.

Table 4. VIF

Variable

Perceived Usefulness

Intention to use

Perceived Usefulness

1.792

Perceived Ease of use

1.995

2.488

Trust

2.006

2.314

Compatibility

1.681

1.922

Security

1.219

Convenience

1.594

Table 5. Direct Effect

Hypothesis

Original

Sample

T

Statistics

P

Values

Description

[H1] Perceived Ease of use ->

Intention to use

-0.074

0.801

0.423

Rejected-

Not Significant

[H2] Trust ->

Intention to use

-0.061

0.716

0.474

Rejected-

Not Significant

[H3] Compatibility ->

Intention to use

0.010

0.123

0.902

Rejected-

Not Significant

[H4] Security ->

Intention to use

0.020

0.192

0.847

Rejected-

Not Significant

[H5] Convenience ->

Intention to use

0.041

0.5122

0.609

Rejected-

Not Significant

[H6] Perceived Usefulness ->

Intention to use

0.440

6.155

0.000

Accepted- Positively

Significant

[H7] Perceived Ease of use ->

Perceived Usefulness

0.455

6.315

0.000

Accepted- Positively

Significant

[H8] Trust -> Perceived

Usefulness

0.285

4.042

0.000

Accepted- Positively

Significant

[H9] Compatibility -> Perceived

Usefulness

-0.047

0.715

0.475

Rejected-

Not Significant

Table 6. Indirect Effect

Hypothesis

Original

Sample

T

Statistics

P

Values

Description

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

975 | P a g e

[H10] Perceived Ease of use ->

Perceived Usefulness -> Intention

to use

0.200

4.215

0.000

Accepted-

Positively

Significant

[H11] Trust ->

Perceived Usefulness ->

Intention to use

0.126

3.421

0.001

Accepted-

Positively

Significant

[H12] Compatibility ->

Perceived Usefulness ->

Intention to use

-0.021

0.696

0.487

Rejected-

Not Significant

Hypothesis 1 has a P value of 0.423 with a T statistic of 0.801. The results showed that

perceived ease of use has no effect on intention to use mobile banking. This can be interpreted

that the perception ease of use is not enough to make someone interested in using m-banking.

This result was aligned with previous research conducted by Al-Jabri, I. (2015) which states

that perceived ease of use has no effect on intention to use. This can be due to consumers using

alternatives to mobile banking or not being able to express perceived ease of use accurately

with consumer experience, therefore consumers have difficulty evaluating the ease of use of

m-banking. However, the results of the study contradict the research of Setiyono, C, et, al

(2019) that perceived ease of use has an effect on intention to use.

Hypothesis 2 has a P value of 0.474 and a T statistic of 0.716. The results showed that

trust has no effect on intention to use mobile banking. This result was aligned with previous

research conducted by Amalia Ratna Pramudita (2020) and Sulistyowati et.al (2022) that trust

does not show a prominent role in predicting intention to using mobile banking, because the

results of the study show that mobile banking services can be trusted and transactions will be

appropriate. Even though they trust, this trust does not have an impact on intention to using

mobile banking.

Hypothesis 3 has a P value of 0.902 with a T statistic of 0.123. The results showed that

compatibility has no effect on intention to use mobile banking. This can be interpreted that

mobile banking is not in accordance with work style, lifestyle or individual needs in

transactions. This result was aligned with previous research conducted by Mandrata, M. I., &

Sutarso, Y. (2019), that customers only need convenience in transactions, but not to manage

their finances which can lead to consumptive living and customers only use services in certain

circumstances.

Hypothesis 4 has a P value of 0.857 with a T statistic of 0.192. The results showed that

security has no effect on intention to use mobile banking. This shows that customers do not

pay attention to security in the mobile banking application, meaning that security is not the

main reason for determining whether to use mobile banking. This result was aligned with

previous research conducted by Wandira, R., & Fauzi, A. (2022), that security is a risky thing

in financial services, but customers do not make security a reason for using mobile banking

services.

Hypothesis 5 has a P value of 0.609 with a T statistic of 0.512. The results showed that

convenience has no effect on intention to use mobile banking. This means that convenience is

not a factor that makes customers use m-banking. This result was aligned with previous

research conducted by Sari, R. et, al (2022) which states that convenience has no effect on

interest in use. Contradict to the research of Park et, al (2019) which states that convenience

has an influence on intention to use.

Hypothesis 6 has a P value of 0.000 with a T statistic of 6.155. The results showed that

there is a positive and significant effect of perceived usefulness on interest in using m-banking.

This can be interpreted that user interest is driven through perceived usefulness, where people

will use m-banking if they understand its benefits. Therefore, m-banking must develop a variety

of services and features that can meet the needs of m-banking users from various groups and

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

976 | P a g e

generations. This result was aligned with previous research conducted by Bustami, E. et, al.

(2021) research, that individuals will use m-banking if they believe it can provide benefits such

as time efficiency. Raza, et. al (2017), Najiba and Fahmab (2020) state that benefits have a

favourable and strong effect on interest in using m-banking.

Hypothesis 7 has a P value of 0.000 with a T statistic of 6.315. The results showed that

perceived ease of use has a significant positive effect on perceived usefulness. This can be

interpreted that the more perceived convenience of mobile banking, the more perceived

benefits or usefulness for users. This result was aligned with previous research conducted by

Widiar, G. et, al. (2023), that the convenience provided makes a person faster and more

productive with mobile banking. The results of this study are in accordance with research

conducted by Makanyeza (2017) and Kurniawan et, al (2022) that perceived convenience has

a significant effect on perceived usefulness.

Hypothesis 8 has a P value of 0.000 with a T statistic of 4.042. The results showed that

trust has a positive and significant effect on perceived usefulness. This can be interpreted that

a high level of trust makes customers want to utilize the service. By trusting the m-banking

manager, namely the bank, it can make m-banking more useful. So, m-banking service

providers must strive to build customer trust.

This result was aligned with previous research conducted by Al-Jabri, I. (2015) which

states that the more customers believe that financial transaction management is safe, the higher

the customer's belief that m-banking is useful. Trust will reduce learning and mental efforts in

understanding, monitoring, and checking every detail related to customer financial

transactions. Research in an effort to test trust in perceived usefulness is supported in research

by Najib, M., & Fahma, F. (2020). The results of the study are contradicted with the research

of Kumar, S. et, al (2021) which states that trust has an effect on perceived usefulness.

Hypothesis 9 has a P value of 0.475 with a T statistic of 0.715. This shows that customer

suitability is not a factor in intention to use m-banking. This result was aligned with previous

research conducted by Kumar, S, et, al (2021) which states that compatibility has no effect on

perceived usefulness, which means that the more a technology suits a person, the lower the

interest in using mobile banking. Contradict to the research of Siyal, et. al (2019) which states

that compatibility is important and influential so that system adjustments with the latest

technology are needed to facilitate customers with high-speed M-banking transactions between

banks and differentiating M-banking services with a wider variety according to user

preferences.

Hypothesis 10 has a P value of 0.000 with a T statistic of 4.215. The results showed that

perceived ease of use has a significant positive effect on intention to use m-banking through

the mediation of perceived usefulness. This shows that perceived ease of use can increase

intention to using mobile banking by building perceived usefulness in m-banking users.

Perceived ease of use cannot directly influence intentio to use m-banking because m-banking

users are used to simplicity. People are used to the existence of mobile phones and various

other platforms that offer the same convenience as offered by m-banking.

The results show that understanding the process of transacting through mobile banking

can make customers find it useful to use mobile banking. Therefore, this ease of use must also

be followed by the benefits that will be received by users. If users feel the benefits of mobile

banking, it will increase their interest in using mobile banking. This result was aligned with

previous research conducted by Widiar, G et. al (2023) which shows that perceived

convenience can contribute to usage interest indirectly by facilitating the impact of perceived

usefulness on usage interest.

Hypothesis 11 has a P value of 0.001 with a T statistic of 3.421. The results showed that

trust has a significant positive effect on intention to use m-banking through the mediation of

perceived usefulness. With the increasing number of mobile banking substitution platforms as

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

977 | P a g e

easy-to-use payment applications, it provides various options for users to choose applications

that can be trusted to meet their needs. Mobile banking officially issued by banking institutions

provides advantages as a trustworthy application (Widiar, G et. al 2023).

The results of the descriptive analysis show that the highest average indicator is achieved

by the accuracy and speed of service that will be provided by the bank if there are problems

with mobile banking, this states that a high level of trust in the mobile banking provider, namely

the bank, in processing any obstacles allows customers to take advantage of mobile banking

services. Al-Jabri's research, I, (2015) states that trust can reduce learning and mental efforts

in understanding, monitoring, and checking every detail related to financial transactions. This

result was aligned with previous research conducted by Kabakuş, A. K, et al (2022) which

states that trust affects interest in use through perceived usefulness as mediation.

Hypothesis 12 has a P value of 0.487 with a T statistic of 0.696. Compatibility has no

influence on interest in using m-banking through the mediation of perceived usefulness. This

can be interpreted that mobile banking is not in accordance with the style of managing finances

and the work style of customers so that they do not feel the benefits of m-banking services so

that it cannot increase interest in using m-banking. This research contradicts the results of

research by Dewi, C, et. Al (2022) which states that compatibility affects interest in use through

perceived usefulness.

CONCLUSION AND RECOMMENDATION

Based on research that has been conducted with twelve hypothesis tests in the conceptual

framework, five hypotheses were found to be accepted. While the other hypotheses are

rejected. Therefore, some managerial suggestions are that Bank Mandiri is advised to equip

customers with more detailed and easier knowledge and information regarding how to activate

mobile banking. Providing information can be done directly or online, it can be done by

socializing to customers who are over 45 years old where at this age they are not used to

technology, because in the characteristics of the respondents as many as 40% of the respondents

are> 45 years old.

Second, it is recommended that Bank Mandiri can increase the transaction limit to

unlimited, of course followed by all applicable provisions and policies, so that customers can

use mobile banking according to their needs.

Third, bank Mandiri needs to evaluate to continue to increase customer trust in m-

banking services, by providing transparent services and responsive services because accuracy

and reliability can increase the interest of bank Mandiri customers to use m-banking. A good

perception of bank Mandiri can provide the right assessment so that customers are interested

in using mobile banking.

BIBLIOGRAPHY

Al-Jabri, I. (2015). The intention to use mobile banking: Further evidence from Saudi Arabia

(Vol. 46, Issue 1). http://ssrn.com/abstract=2598905

Bramastio Wahyudi & Merlyana Dwinda Yanthi (2021). Acceptance of TAM Theory on the

Use of Mobile Payment with Compatibility as an External Variable. Accountability Vol.

15, No. 1, 2021.

Bustami, E., Situngkir, S., Yacob, S., & Octavia, A. (2021). Customers’ behavioral intention

on mobile banking services in Indonesia. International Journal of Research in Business

and Social Science (2147- 4478), 10(7), 353–362.

https://doi.org/10.20525/ijrbs.v10i7.1403

Desvronita (2021). Factors Affecting Interest in Using the E-Wallet Payment System Using

the Technology Acceptance Model. Akmenika Journal Vol 18 No 2

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

978 | P a g e

Dewi, C., Sisiawan, R. (2022). The Role of Compatibility, Perceived Usefulness, Convenience

Perception and Convenience Perception on Electronic Money (e-Wallet) Usage Interest

Grace. http://journalppw.com

Gumussoy, C. A., Kaya, A., & Ozlu, E. (2018). Determinants of mobile banking use: an

extended TAM with perceived risk, mobility access, compatibility, perceived self-

efficacy and subjective norms. In Industrial Engineering in the Industry 4.0 Era, 225–

238. https://doi.org/10.1007/978-3-319-71225-3_20

Kabakuş, A. K., & Küçükoğlu, H. (2022). The effect of trust on mobile banking usage.

Ekonomski Vjesnik, 35(2), 231–246. https://doi.org/10.51680/ev.35.2.1

Kim, Y. J., Park, Y.-J., Choi, J., & Yeon, J. (2015). An Empirical Study on the Adoption of

“Fintech” Service: Focused on Mobile Payment Services. April, 136–140.

https://doi.org/10.14257/astl.2015.114.26

Kumar, S., Leonie, A., Yukita, K. (2021). Millennials Behavioral Intention in Using Mobile

Banking: Integrating Perceived Risk and Trust into TAM (A Survey in Jawa Barat)

Kurniawan, I. A., Mugiono, M., & Wijayanti, R. (2022). The effect of Perceived Usefulness,

Perceived Ease of Use, and social influence toward intention to use mediated by Trust.

Jurnal Aplikasi Manajemen, 20(1), 117–127

Lichtenstein, S., & Williamson, K. (2006). Understanding Consumer Adoption of Internet

Banking: An Interpretive Study in the Australian Banking Context. Journal of Electronic

Commerce Research, 7, 50-66.

Makanyeza, C. (2017). Determinants of consumers’ intention to adopt mobile banking services

in Zimbabwe. International Journal of Bank Marketing, 35(6).

https://doi.org/10.1108/IJBM-07-2016-0099

Mandrata, M. I., & Sutarso, Y. (2019). The Effect of Usability, Suitability, Relative Advantage,

Hedonic Motivation and Perceived Risk on the Use of Bank Mandiri Surabaya Mobile

banking Mediated by Customer Behavioral Intention. Journal of Business & Banking,

9(1). https://doi.org/10.14414/jbb.v9i1.1501

Moore, G. C., & Benbasat, I. 1991. Development of an Instrument to Measure the Perceptions

of Adopting an Information Technology Innovation. Information Systems Research,

2(3), 192–222

Mulia, D., Usman, H., & Parwanto, N. B. (2020). The role of customer intimacy in increasing

Islamic bank customer loyalty in using e-banking and m-banking. Journal of Islamic

Marketing, 12(6), 1097–1123. https://doi.org/10.1108/JIMA-09-2019-0190

Najib, M., & Fahma, F. (2020). Investigating the adoption of digital payment system through

an extended technology acceptance model: An insight from the Indonesian small and

medium enterprises. International Journal on Advanced Science, Engineering and

Information Technology, 10(4), 1702–1708.

https://doi.org/10.18517/ijaseit.10.4.11616

Pramudita, Amalia Ratna. 2020. “The Effect of Perceived Ease, Perceived Benefits, Trust, and

Risk on Customer Interest in Using Mobile Banking with Usage Attitude as an

Intervening Variable”. E-Jurnal. Semarang: IAIN Salatiga

Rahim Amihsa, A. R., Saferian, E., & Syahrir, S. (2020). Factors Affecting the Use of Mobile

Payment in Indonesia. Jurnal Ekonomi, Sosial & Humaniora. E-ISSN 2686 5661 VOL

02 NO 03

Raza, S. A., Umer, A., Shah, N. (2017). New determinants of ease of use and perceived

usefulness for mobile banking adoption. International Journal of Electronic Customer

Relationship Management. https://doi.org/10.1504/IJECRM.2017.086751

Rita J.D. Atarwaman (2022). The Effect of Risk Perception, Usability, Trust and Ease of Use

on Attitudes towards Using Mobile banking in Ambon City. E-Qien Journal of

Economics and Business, Vol. 10 No.2

https://dinastipub.org/DIJDBM Vol. 4, No. 5, August 2023

979 | P a g e

Sari, R. L., Habibi, A. B., & Hayuningputri, E. P. (2022). Impact of Attitude, Perceived Ease

of Use, Convenience, and Social Benefit on Intention to Use Mobile Payment. Asia

Pacific Management and Business Application, 011(02), 143–156.

https://doi.org/10.21776/ub.apmba.2022.011.02.2

Setiyono, C., Shihab, M. R., Azzahro, F. (2019). The role of initial trust on intention to use

branchless banking application: Case study of jenius. Journal of Physics: Conference

Series. https://doi.org/10.1088/1742-6596/1193/1/012022

Siyal, Abdul Waheed; Ding, Donghong; Siyal, Saeed (2019). M-banking barriers in Pakistan:

a customer perspective of adoption and continuity intention. Data Technologies and

Applications, (), DTA-04-2018-0022–. doi:10.1108/DTA-04-2018-0022

Sulistyowati, W. A., Alrajawy, I., Isaac, O., Yulianto, A., & Ameen, A. (2022). Examining The

Intention To Use Mobile banking During Period Of Covid-19: Technology Acceptance

Model With Trust. Journal of Southwest Jiaotong University, 57(6), 20–32.

https://doi.org/10.35741/issn.0258-2724.57.6.3

Vemuri, R., & Chen, S. (2021). Split Manufacturing of Integrated Circuits for Hardware

Security and Trust: Methods, Attacks and Defenses. Springer.

Wandira, R., & Fauzi, A. (2022). TAM Approach: Effect of Security on Customer Behavioral

Intentions to Use Mobile banking. Daengku: Journal of Humanities and Social Sciences

Innovation, 2(2), 192–200. https://doi.org/10.35877/454ri.daengku872

Wang, X., Xi, Y., Xie, J. and Zhao, Y. (2017), ", Vol. 21 No. 6, pp. 1580-1595.

https://doi.org/10.1108/JKM-03-2017-0091 Organizational unlearning and knowledge

transfer in cross-border M&A: the roles of routine and knowledge compatibility",

Journal of Knowledge Management

Whitman, M.E., & Mattord, H.J. (2017), Management of Information Security, Third Edition,

Boston: Course Technology

Wibowo, A. (2017). A Study of Information System User Behavior with the Technology

Acceptance Model (TAM) Approach. National Conference on Information Systems, 1-

8.

Widiar, G., Yuniarinto, A., & Yulianti, I. (2023). Perceived Ease of Use’s Effects on

Behavioral Intention Mediated by Perceived Usefulness and Trust. Interdiscipline Social

Studies.

Wulandari, F. (2019). Use of Electronic Money (Study on Go-Pay Users in Malang City).

Student Scientific Journal FEB, 7(2): 1-14.