GLOBAL REAL

ESTATE DEI

SURVEY

VOLUME III

A survey of diversity, equity and inclusion practices and

benchmarking metrics among commercial real estate rms globally

The Global Real Estate DEI Survey is the only corporate study of diversity, equity and inclusion (DEI)

management practices and data benchmarking in the commercial real estate (CRE) industry.

This third iteration of the Global Real Estate DEI Survey is the result of the collaboration between six sponsoring associations NAREIM,

NCREIF, PREA, REALPAC, ULI and Ferguson Partners, as well as 14 supporting associations AFIRE, AIA, APREA, AREF, BOMA, BPF, CFMA,

CoreNet Global, CREFC, EPRA, NAIOP, OSCRE, PFA and RICS.

This is a summary report of high-level results providing a view of DEI metrics relating to:

• DEI program structure, resources and ownership.

• Policies focused on recruitment, retention and promotion, inclusive culture, tracking and accountability, and pay equity.

• Employee demographics by gender and race/ethnicity, across seniority and job function, as well as DEI hiring, promotion and

departure trends year-over-year.

Survey participants receive a spreadsheet with full data, providing for an in-depth look and suitable for benchmarking DEI policies and

achievements against peers.

The Global Real Estate DEI Survey Volume III represents 296,902 full-time real estate employees, $1.98 trillion of assets under

management, and a cross-section of the commercial real estate industry in terms of size, region and business classication. The Survey

brings together participation from 216 unique organizations which provided 236 submissions detailing their DEI practices in North

America (79.2% of respondents), Europe (11.9%) and Asia-Pacic (8.9%). Data was collected between July 17 and September 29, 2023.

This summary report includes 46 pages of key trends relating to DEI management practices and metrics. As the sample of respondents

changes from year to year, conclusions based on changes should be interpreted cautiously.

We extend our sincere thanks and appreciation to all participating organizations for providing valuable information.

The Global Real Estate DEI Survey Volume III

INTRODUCTION

Global Real Estate DEI Survey Volume III 1

Lindsay Wilhusen

Survey Director, Ferguson Partners

Meredith Doucette

Vice President, Ferguson Partners

Zoe Hughes

CEO, NAREIM

Dan Dierking

President, NCREIF

Gail Haynes

President, PREA

Michael Brooks

CEO, REALPAC

Sonia Huntley

Senior Vice President,

Diversity, Equity & Inclusion, ULI

If you would like to take part in the next Global Real Estate DEI Survey in 2025, please contact your local real estate industry association.

INTRODUCTION

Global Real Estate DEI Survey Volume III 2

3 Executive summary

7 Global Real Estate DEI Survey Volume III – Results

8 Note to participants

9 Respondent demographics

10 236 submissions received. Here’s who participated.

11 Company types | Ownership status and CRE business

12 Real estate employees | Gross real estate AUM

13 CRE gender and ethnicity YoY changes 2021 to 2023

14 Employee demographics – Asia-Pacic

15 Asia-Pacic employee demographics by gender & seniority

16 Asia-Pacic hires, promotions & departures

17 Employee demographics – Europe

18 Europe employee demographics by gender & seniority

19 Europe hires, promotions & departures

20 Employee demographics – Canada

21 Canada employee demographics by gender & seniority

22 Canada hires, promotions & departures

23 Employee demographics – US

24 US demographics by gender & seniority

25 US demographics by ethnicity & seniority

26 US demographics for POC by ethnicity & seniority

27 US CRE functions by gender & race/ethnicity

28 US hires, promotions & departures

29 US hires, promotions & departures continued

30 US reasons for departure

31 US carried interest and equity/equity-like currencies allocation

32 DEI program & initiatives

33 DEI programs & budgets

34 Dimensions of diversity

35 DEI goals and success

36 Ten most impactful DEI policies

37 DEI decision-making

38 Top strategies for recruitment & retention

39 Top 5 DEI partners, by region

40 Top 5 retention & promotion strategies

41 Top 5 inclusive work culture strategies

42 Top DEI metrics tracked

43 Pay equity strategies

44 Top 7 DEI obstacles

45 Survey participants

47 Sponsoring and supporting associations

48 Sponsoring associations

49 Supporting associations

Contents

Executive summary

Global Real Estate DEI Survey Volume III 3

Diversity at work: The building blocks of fairness

EXECUTIVE SUMMARY

Global Real Estate DEI Survey Volume III 4

With the support of 19 industry associations, the Global Real

Estate DEI Survey Volume III better captures the

representation of professional services rms, architectural

practices, construction companies and brokerages in the

commercial real estate industry globally.

The composition of commercial real

estate (CRE) rms that responded to

this year’s report diers slightly from

the previous year. Where the previous

Survey received 210 submissions from

192 organizations, this edition received

236 submissions from 216 distinct

organizations. Real estate private

equity rms/real estate investment

managers continue to be the largest

respondent group. However, this year

there are more architectural/

engineering/construction companies,

professional services, and commercial

brokerages, which can contribute to

year-on-year changes.

With that in mind, the 216 rms that

participated in this year’s Survey

employ 296,902 full-time real estate

employees and represent nearly $2

trillion of AUM. Of the rich data bank

provided by respondents, a small

selection of data is presented in

this report.

Headline data shows the

representation of women ranged

from 39.8% to 45.6% across the

regions surveyed. Of US CRE rms,

29.7% of full-time employees (FTEs)

were professionals from

underrepresented racial/ethnic

groups. This year, for the rst time, we

are reporting North American

demographic data for Canadian

employees and, separately,

employees in the United States.

Fighting DEI fatigue

This year’s Survey comes at an

especially important juncture as global

conicts, inationary pressures and

high interest rates are causing concern

that companies, CRE rms included,

are pulling back on DEI aspirations.

Just as DEI is not an afternoon’s

training, or something to ponder only

during Black History Month, DEI is a

process and movement to change

culture and correct inequities. Fighting

DEI fatigue is not only the right thing to

do for underrepresented peoples, but

can also lead to improved performance.

With global fears that DEI

commitments might be stalling, it is

notable that almost all respondents

(95.8%) said they have either a formal

DEI program or some initiatives

and/or policies in place. Of these

respondents, 97.9% said DEI ranked as

GLOBAL

56.4%

have a formal DEI program in

place, compared to the

previous year when 53.6% of

that cohort reported having

one in place

51%

have dened hiring targets for

underrepresented groups

64.7%

said improved employee

engagement/productivity was

among the most important

outcomes of DEI eorts

97.9%

of respondents who have a

DEI program/policies say DEI

ranked as a higher priority or

at the same level as a year ago

A spreadsheet containing the complete Survey results – including data

broken down by region, number of full-time employees, AUM and business

classication – is available to Survey respondents. The data can be used for

peer-to-peer comparison purposes, and to gather data points for any

aspects of DEI eorts of particular interest.

a higher priority or at the same level

as it was one year ago.

Broadening the eort

CRE rms continue to focus on

gender parity and race/ethnicity as

the two main DEI dimensions. It has

become standard practice to gather

information on gender and age. At

the same time, they are also collecting

data on physical disability, family

status, languages spoken and

LGBTQ+ status.

Trends on hires, promotions and

departures over a 12-month period

for each region help observe change.

Globally, 61.1% of firms said they are

broadening or being flexible on

experience and educational

requirements when hiring, to capture

candidates that may not have had

traditional paths or backgrounds.

Firms are also offering scholarships/

internships, reaching outside the CRE

pool, reviewing job postings for

hidden bias, and ensuring the hiring

team includes those from

underrepresented groups.

But CRE rms acknowledge that hiring

practices are insucient to make the

necessary headway. Instead, a myriad

of strategies must work in concert,

including making employees feel

included. For example, 85% of

companies surveyed are already

holding inclusive social events. With a

further 4.7% seeking to introduce

social events in the next 12 months,

this strategy is edging closer to

universal adoption. In another

example of inclusion, just over half

said their company communicated

with employees on current events

such as denouncing violence against

specic ethnic groups.

Two-thirds of companies said they are

actively striving to identify gender-

based pay gaps to achieve pay equity.

Some 44.6% rms are taking a step

further to analyze pay disparities

based on race, ethnicity or age.

Determining who holds the ultimate

responsibility for achieving corporate

goals through DEI initiatives is key.

The trend is shifting away from

decision-making by a DEI team or

committee, towards decision-making

by senior executive(s).

Increasing impact

There has also been a shift in what

companies said are their most

impactful DEI policies. At the top

of this year’s ranking is the creation

of scholarships/internships to

increase the number of

underrepresented individuals in

candidate pools. In the previous year,

more firms said their most impactful

strategy was offering work/life

balance programs, although this may

be due to changes in the sample of

responding firms.

This change could be potentially

related to companies looking to

strengthen their future employee

pool, which represents a structurally

changing society, and moving

away from work/life balance, which

may have been a legacy of the

pandemic.

Year-on-year differences in data

should not be relied upon alone to

draw conclusions given this new

report has expanded to include more

types of CRE firms whose inclusion

could be the reason for some

percentage changes. However, all

the types of firms share one thing

in common.

Having a goal or objective is

necessary for success. In terms of

desired output, respondents said the

top outcome desired was achieving

greater diversity throughout the

entire organization. They also sought

higher employee retention as well as

engagement/productivity.

EXECUTIVE SUMMARY

Global Real Estate DEI Survey Volume III 5

THE US

41.4%

of employees are women,

with year-on-year rises at

most levels of seniority,

although this could be due

to changes in the sample

of respondents

5.7%

of board directors are

Black or African American,

the largest of any

underrepresented racial/

ethnic group

42.2%

of those working in securities

(REITs, CMBS etc) are women

CANADA

45.6%

of employees at the company

overall are women, the

highest representation out of

all regions surveyed

11.8%

is the departure rate for senior-

level women, the lowest of any

organizational level in Canada

Notably, 56.4% of companies have

implemented formal DEI programs.

Indeed, up to 81% of the very largest

companies in terms of FTEs and AUM

have formal DEI programs in place.

Furthermore, 36.3% of those with a

formal DEI program (or some

initiatives in place) now have a

dedicated DEI budget.

More than a third of respondents

(36.3%) with a formal DEI program or

some initiatives in place now have a

dedicated DEI budget. That is up from

30.4% a year ago.

Among respondents that have a

dedicated DEI budget, 4.9% say that

the DEI budget is 5% or more of the

organization’s operating budget. The

majority (80.5%) says their rms spend

less than 1% of the operating budget

on DEI matters.

Momentum pointers

Change is happening.

For US participants, approximately a

quarter of executive management

hires were people of color. Board of

director hires are now evenly split

between men and women.

Furthermore, in 2023, men and

women from underrepresented

groups were hired as board directors

in 63% of cases.

Many CRE companies are

progressing. The days when diversity

was lacking among CRE executive

teams, partners, event panelists, and

overall makeup of the industry

should be a thing of the past. But

there is also a danger to the progress

achieved to date if the industry does

not carefully and proactively lead

from the front on DEI.

Some 98.3% of CRE respondents

said they feel DEI will be a higher

priority or at the same level one

year from now. That is a reason to

feel optimistic.

EXECUTIVE SUMMARY

Global Real Estate DEI Survey Volume III 6

EUROPE

77.8%

are broadening or being more

exible on educational

requirements and previous

job experience for new hires

56%

have a dedicated DEI budget

68%

of rms have a formal DEI

committee for employees to

participate in voluntarily

ASIAPACIFIC

70%

of promotions at executive

management level within

the past year were granted

to women

52.4%

of rms believe DEI will likely

be a higher priority one year

from now versus 34.8% in

North America

66.7%

of rms ensure the hiring team

includes employees from

underrepresented groups

We appreciate your support in

helping to track DEI eorts.

Thank you to all who participated.

Global Real Estate DEI Survey Volume III – Results

Global Real Estate DEI Survey Volume III 7

Note to participants

SURVEY NOTES

Global Real Estate DEI Survey Volume III 8

With 216 organizations

providing 236 Survey

submissions for the

Asia-Pacific, European and

North American regions,

across different types of

commercial real estate

organizations, the scale of

data on DEI practices and

employee demographics is

unprecedented.

This report reflects data provided by

those participants. Despite being one

of the most comprehensive reports

of its kind globally, note that figures

are averages for the respondent set

of that particular year, rather than the

entire CRE industry.

To aid analysis and review, the

participating associations and

Ferguson Partners have created an

accompanying Excel document

allowing DEI Survey Volume III

participants access to the full data set

for select questions. As can be seen

from the report, DEI demographic and

practice results have been broken

down by the following categories:

• Gender: Male/Female/Nonbinary

• Region: Asia-Pacic, Europe and

North America with employees in

Canada and/or the United States

• Race/ethnicity: Sucient data

was only collected for North

America, the categories for which

include: Hispanic or Latino; White

(not Hispanic of Latino), Black or

African American; Native Hawaiian

or other Pacic Islander; Asian;

American Indian or Alaska

Native/Aboriginal/Indigenous

people (e.g., member of a First

Nation, Inuit, Métis); multiracial

(two or more races); individuals

who did not disclose or specify a

race/ethnicity

• Seniority: Company overall;

board of directors; executive

management; senior-level

professionals; mid-level

professionals; junior-level

professionals

• Size of rm, global full-time

employees (FTEs): Less than 50

FTEs; 50–149 FTEs; 150–599 FTEs;

600 FTEs and greater

• Size of rm, AUM: Less than

$3bn AUM; $3bn–$9.9bn AUM;

$10bn–$29.9bn AUM; $30bn AUM

and greater

• Type of business/business

category:

All companies;

REITs/REOCs; REPE/REIM rms;

AEC rms; professional services

rms

Throughout the report, key acronyms

will be used including:

AEC: Architecture/Engineering/

Construction

AUM:

Assets under management

CRE: Commercial real estate

DEI: Diversity, equity & inclusion

FTE: Full-time employees

POC: People of color

REIM: Real estate investment

management

REIT: Real estate investment trust

REOC: Real estate operating company

REPE: Real estate private equity

Other notes:

• Underrepresented group is a

subset(s) of the employee

population with a smaller

percentage than the overall

employee population.

• At least ve (5) companies must

provide a response for any given

data point in order to provide

meaningful results.

• ‘–’ is shown in instances where the

result is 0.0%.

• ‘ISD’ is shown in circumstances

where there is insucient data on

which to report (i.e., fewer than

ve observations).

• All spellings are US English.

• All data is displayed in USD. Please

note that the following

conversion rates are used in this

report. Currency conversions used

are based on the average

conversion rate over a two-year

period (104 weeks).

Currency Conversion

CAD to USD 0.762137

EUR to USD 1.075630

GBP to USD 1.253090

USD to USD 1

Global Real Estate DEI Survey Volume III 9

Respondent demographics

CONTENTS

This section outlines various company demographic metrics. Specic analyses include:

• Respondent geographic region

• CRE rms by region

• Company ownership

• Company type

• Company full-time employees

• Company assets under management

Note: The Global Real Estate DEI Survey Volume III received 236 distinct submissions on behalf of 216 unique organizations. Asia-Pacific received 21 submissions to comprise

8.9% of responses, Europe received 28 submissions to comprise 11.9% of responses, and North America received 187 submissions to comprise 79.2% of responses.

As the sample of respondents changes from year to year, conclusions based on changes should be interpreted cautiously.

An Excel spreadsheet containing all respondent demographic data is provided to Survey respondents.

236 SUBMISSIONS RECEIVED. HERE’S WHO PARTICIPATED.

Global Real Estate DEI Survey Volume III 10

RESPONDENT DEMOGRAPHICS

Nearly four-fifths of respondents in the third iteration of the Global Real Estate DEI Survey were from North America, while

90% have operations in the region. The expanded Survey is supported by 19 industry associations meaning the

composition of the respondent group has changed year-over-year, with architectural/engineering/construction

companies, professional services and commercial brokerages gaining greater representation. The proportion of real estate

private equity and investment management firms fell to 45.4% in 2023 from 56.8%. Survey participants can access the full

data in the accompanying spreadsheet.

90.3%

35.2%

27.8%

6.5%

4.6%

Africa/

Middle East

South America

Asia-Pacic*

Europe

North America

CRE rm operations by region

Respondent geographic region

Asia-Pacic

(8.9%; 21 responses)

Europe

(11.9%; 28 responses)

North America

(79.2%; 187 responses)

* Includes Australia and New Zealand.

Duplicate entries for organizations submitting on behalf of more than one region have been removed.

In addition to indicating the region for which they are completing the survey, participating firms also listed all regions

in which they have operations.

COMPANY TYPES | OWNERSHIP STATUS AND CRE BUSINESS

Global Real Estate DEI Survey Volume III 11

RESPONDENT DEMOGRAPHICS

Company ownership status

Other

(0.5%)

Government-owned

(1.9%)

Aliate of a listed

(public) company

(3.2%)

Listed (public)

(20.8%)

Non-listed (private)

(73.6%)

7.4%

4.6%Commercial brokerage/services rm

3.7%

Corporate real estate divison

of a non-real estate entity

3.7%Developer

2.8%

Combined investments manager,

developer and/or operator

2.3%Institutional investor

1.9%Mortgage nance company

Professional services rm

Architecture/Engineering/

Construction (AEC) rm

Real estate investment trust (REIT)/

Real estate operating company (REOC)

Real estate private equity (REPE)/

Real estate investment management (REIM)

Type of CRE business

45.4%

17.1%

11.1%

Note: Other includes nonprofit.

REAL ESTATE EMPLOYEES | GROSS REAL ESTATE AUM

Global Real Estate DEI Survey Volume III 12

RESPONDENT DEMOGRAPHICS

# of real estate FTEs globally

>600

(18.5%)

150–599

(26.4%)

50–149

(26.9%)

<50

(28.2%)

$0.43

$3.05

$3.00

$7.10

$1.57

$7.30

$6.77

$24.40

$8.08

$22.96

$25.80

75th percentile

Median

25th percentile

Gross AUM as of December 31, 2023 ($bn)

$2.98

Global $22.11

Asia-Pacic $4.09

Average

Europe $13.79

North America $19.48

Average

Responses are out of the 45.4% of organizations that indicated they are a REPE or REIM in question 2.

Duplicate entries for organizations submitting on behalf of more than one region have been removed.

Duplicate entries for organizations submitting on behalf of more than one region have been removed.

CRE GENDER AND ETHNICITY YOY CHANGES 2021 TO 2023

Global Real Estate DEI Survey Volume III 13

EMPLOYEE DEMOGRAPHICS GLOBAL

2023 (60.6% of Survey participants) 2022 (81.4% of Survey participants) 2021 (77.1% of Survey participants)

United States Men Women Men Women Men Women

Company overall 58.6% 41.4% 57.5% 42.5% 59.0% 41.0%

Hispanic or Latino 5.4% 4.0% 5.2% 4.4% 5.0% 4.0%

White (not Hispanic or Latino) 42.4% 26.4% 39.1% 25.5% 44.0% 25.0%

Black or African American 3.2% 4.0% 3.1% 3.7% 3.0% 4.0%

Native Hawaiian or other Pacic Islander 0.1% 0.1% 0.1% 0.1% – –

Asian 5.1% 4.7% 5.9% 5.9% 5.0% 5.0%

American Indian or Alaska Native 0.1% 0.2% 0.1% 0.2% – 1.0%

Multiracial (two or more races) 1.5% 1.3% 1.5% 1.1% 1.0% 1.0%

Did not disclose/specify 0.8% 0.7% 2.5% 1.6% 1.0% 1.0%

2023 (18.6% of Survey participants) 2022 2021

Canada Men Women Men Women Men Women

Company overall 54.1% 45.6% N/A N/A N/A N/A

2023 (11.9% of Survey participants) 2022 (12.4% of Survey participants) 2021 (16% of Survey participants)

Europe Men Women Men Women Men Women

Company overall 60.2% 39.8% 60.5% 39.5% 62.0% 38.0%

2023 (8.9% of Survey participants) 2022 (6.2% of Survey participants) 2021 (6.9% of Survey participants)

Asia-Pacic Men Women Men Women Men Women

Company overall 55.2% 44.8% 50.0% 50.0% 53.0% 47.0%

Distribution of responses: Gender and race/ethnicity at commercial real estate rms (2021 to 2023)*

This chart depicts the proportion of men and women in full-time positions at the overall company level at CRE rms globally

as provided by respondents to the Global Real Estate DEI Survey. In 2023, the Survey expanded to a total of 19 CRE industry

associations and their members.

* While most of the data collected in 2021 and 2022 represented employees in the United States, the Survey only requested data on behalf of employees in North America in those years. This year (2023), data was collected separately for employees in

the United States and in Canada.

Employee demographics – Asia-Pacic

Global Real Estate DEI Survey Volume III 14

CONTENTS

This section provides highlights of employee demographic metrics for Asia-Pacic.

Specic analyses include:

• Demographics by gender & seniority

• Hires, promotions & departures

Note: Responses in this section are based on the survey participants who completed the survey on behalf of Asia-Pacific (8.9%).

The nonbinary/nonconfirming category has been removed throughout the demographics section, as we did not receive enough data to report on it.

As the sample of respondents changes from year to year, conclusions based on changes should be interpreted cautiously.

An Excel spreadsheet containing full demographic data collected for Asia-Pacic is provided to Survey respondents.

ASIAPACIFIC EMPLOYEE DEMOGRAPHICS BY GENDER & SENIORITY

Global Real Estate DEI Survey Volume III 15

EMPLOYEE DEMOGRAPHICS ASIAPACIFIC

Men

Women

55.2% 44.8%

50.0% 50.0%

Junior-level professionals

(all other sta)

Mid-level professionals

Senior-level professionals

Executive management

Board of directors

Company overall

2022

2023

82.7% 17.3%

76.1% 23.9%2022

2023

77.6% 22.4%

75.4% 24.6%2022

2023

66.9% 33.1%

65.2% 34.8%2022

2023

58.1% 41.9%

52.5% 47.5%2022

2023

48.0% 52.0%

32.6% 67.4%2022

2023

The chart below depicts employee demographics of CRE rms in Asia-Pacic. Women represented 44.8% of employees at

Asia-Pacic Survey respondent rms. This is above the 39.8% representation of women in Europe. Similar to other regions, the

proportion of women declines as we move up the organizational hierarchy, from a majority of 52% at the junior level to 41.9%

at the mid-level and gradually decreasing to 17.3% at the board of director level.

Data is reflective of the 8.9% of respondents who completed the survey on behalf of Asia-Pacific. Demographic breakdowns reflect average values.

ASIAPACIFIC HIRES, PROMOTIONS & DEPARTURES

Global Real Estate DEI Survey Volume III 16

EMPLOYEE DEMOGRAPHICS ASIAPACIFIC

The table below displays a noteworthy observation: 70% of promotions at the executive management level in 2023 were

granted to women. This percentage is signicantly higher than at other levels, suggesting deliberate action is being taken to

address the gender imbalance. However, drawing conclusive insights becomes challenging due to insucient data on hiring

and departures at the executive management level.

52%

Slightly more than half of junior

positions in Asia-Pacific were held

by women (52%). They were also

promoted at a greater level

(56.8%) than their male

counterparts, although more

junior women proportionately

also left their firms (53.7%).

Executive

management

Senior-level

professionals

Mid-level

professionals

Junior-level professionals

(all other staff)

% of employee population

Men

(77.6%)

Women

(22.4%)

Men

(66.9%)

Women

(33.1%)

Men

(58.1%)

Women

(41.9%)

Men

(48.0%)

Women

(52.0%)

Total hired in past year ISD ISD 71.7% 28.3% 53.3% 46.7% 54.6% 45.4%

Total promoted in past year 30.0% 70.0% 63.5% 36.5% 55.8% 44.2% 43.2% 56.8%

Total departed in past year ISD ISD 40.5% 59.5% 66.2% 33.8% 46.3% 53.7%

46.7%

Among Asia-Pacic respondents, 46.7% of mid-level employees

hired were women, a higher rate than their current representation

(41.9%). At this level, the proportion of women promoted (44.2%)

is also higher than those who departed (33.8%). However, the

stakes are raised at the next level, of senior-level professionals: just

over one-third (36.5%) promoted were women, a smaller

percentage were hired (28.3%) and, concerningly, nearly six in ten

professionals who departed (59.5%) were women.

59.5%

The highest proportion of

departures among full-time CRE

employees occurred among

senior-level women (59.5%).

Women at the senior level are

also hired at the lowest

proportion (28.3%) among all

levels and genders in Asia-Pacic.

Data is reflective of the 8.9% of respondents who completed the survey on behalf of Asia-Pacific. Demographic backgrounds reflect average values.

Employee demographics – Europe

Global Real Estate DEI Survey Volume III 17

CONTENTS

This section provides highlights of employee demographic metrics for Europe.

Specic analyses include:

• Demographics by gender & seniority

• Hires, promotions & departures

Note: Responses in this section are based on the survey participants who completed the survey on behalf of Europe (11.9%).

As the sample of respondents changes from year to year, conclusions based on changes should be interpreted cautiously.

An Excel spreadsheet containing full demographic data collected for Europe is provided to Survey respondents.

EUROPE EMPLOYEE DEMOGRAPHICS BY GENDER & SENIORITY

Global Real Estate DEI Survey Volume III 18

EMPLOYEE DEMOGRAPHICS EUROPE

Men

Women

60.2% 39.8%

60.5% 39.5%

Junior-level professionals

(all other sta)

Mid-level professionals

Senior-level professionals

Executive management

Board of directors

Company overall

2022

2023

80.8% 19.2%

84.2% 15.8%2022

2023

74.6% 25.4%

87.1% 12.9%2022

2023

72.4% 27.6%

81.6% 18.4%2022

2023

63.5% 36.5%

60.0% 40.0%2022

2023

50.3% 49.7%

42.8% 57.2%2022

2023

The chart below depicts employee demographics of CRE rms in Europe. The percentage of women at the overall company

level remained steady around 39%, ticking up 0.3% from 2022 and 1% from 2021, although this may be due to changes in the

sample of responding rms. In Europe, there has been an increase in the representation of women at the senior level and

higher. The proportion of women in executive management almost doubled to 25.4% in 2023 from 12.9% the previous year,

although, again, this may be due to changes in the sample of responding rms.

Data is reflective of the 11.9% of respondents who completed the survey on behalf of Europe. Demographic breakdowns reflect average values.

EUROPE HIRES, PROMOTIONS & DEPARTURES

Global Real Estate DEI Survey Volume III 19

EMPLOYEE DEMOGRAPHICS EUROPE

This year, there were enough responses to yield information on executive management promotions in Europe, unlike the

previous Survey in 2022. Over four in ten promotions (44.4%) among executive management were of women, making it the

highest proportion for any level. At the senior, mid and junior levels, the proportion of women promoted increased relative to

the data received in the previous year.

Executive

management

Senior-level

professionals

Mid-level

professionals

Junior-level professionals

(all other staff)

% of employee population

Men

(74.6%)

Women

(25.4%)

Men

(72.4%)

Women

(27.6%)

Men

(63.5%)

Women

(36.5%)

Nonbinary

(0.0%)

Men

(50.3%)

Women

(49.7%)

Total hired in past year 65.0% 35.0% 66.5% 33.5% 55.9% 43.9% 0.2% 51.9% 48.1%

Total promoted in past year 55.6% 44.4% 63.1% 36.9% 67.3% 32.7% – 63.4% 36.6%

Total departed in past year 66.5% 33.5% 68.7% 31.3% 47.8% 52.2% – 54.0% 46.0%

44.4%

Over four in ten (44.4%) promotions of executive managers at CRE rms

in Europe are of women. This is the highest rate of promotions for

women across all levels where data is available. However, only three in

ten promotions (32.7%) at the mid-level were awarded to women. This

is an improvement over last year when 26.3% of women at the mid-level

were promoted, although this could be due to changes in the sample of

responding rms. There was insucient data for executive level

promotions last year.

52.2%

Over half of the professionals at the mid-level departing CRE rms in

Europe last year were women (52.5%). This is over two-thirds higher than

the previous Survey in 2022, when only 30% of leavers at this level were

women, although this may be due to changes in the sample of

responding rms. While over 96% of women departing at the mid-level

did not disclose a reason, those who did cited joining/starting a

competing rm as the main driver. The second main reason given was

family care.

Data is reflective of the 11.9% of respondents who completed the survey on behalf of Europe. Demographic breakdowns reflect average values.

Employee demographics – Canada

Global Real Estate DEI Survey Volume III 20

CONTENTS

This section provides highlights of employee demographic metrics for North American rms with

employees in Canada.

Specic analyses include:

• Demographics by gender & seniority

• Hires, promotions & departures

Note: Participants who completed the survey on behalf of their North American operations (79.2%) were given the option to submit demographic data for Canada,

the United States, or both. Responses in this section are based on the 18.6% of total participants who submitted demographic data for employees in Canada.

The nonbinary category has only been included where there was sufficient data to report on it.

As the sample of respondents changes from year to year, conclusions based on changes should be interpreted cautiously.

An Excel spreadsheet containing full demographic data collected for Canada is provided to Survey respondents.

CANADA EMPLOYEE DEMOGRAPHICS BY GENDER & SENIORITY

Global Real Estate DEI Survey Volume III 21

EMPLOYEE DEMOGRAPHICS CANADA

Men

Women

Nonbinary

54.1% 45.6%

Junior-level professionals

(all other sta)

Mid-level professionals

Senior-level professionals

Executive management

Board of directors

Company overall

72.6% 27.4%

74.5% 25.5%

66.7% 33.0%

56.3%43.5%

49.1% 50.5%

For the rst time, the Global Real Estate DEI Survey presents break out data for Canada; dened as North American CRE rms

with employees in Canada. Women represented 45.6% of this demographic surveyed. This is above the level reported by

European respondents, and roughly the same as in Asia-Pacic. In Canada, women are underrepresented at the top three

levels but are well balanced at the mid and junior levels, forming a majority (50.5%) at the latter. More data on Canada

demographics can be found in the Excel spreadsheet provided to respondents.

Data is reflective of the 18.6% of respondents who completed the survey on behalf of North America and have employees in Canada. Demographic breakdowns reflect average values.

CANADA HIRES, PROMOTIONS & DEPARTURES

Global Real Estate DEI Survey Volume III 22

EMPLOYEE DEMOGRAPHICS CANADA

What follows is data showing how to analyze and understand the promotions, hires and departures data. As can be seen

below, the Survey data from Canada shows that the proportion of women both hired and promoted at the senior, mid and

junior levels exceeded those who left. Note, to move the needle on the diversity of a given employee group, the

proportion of promotions and hires must be greater than the percentage of that group’s baseline employee population,

with the departure rate also lower.

48.4%

At the mid-level, women at

Canadian CRE rms comprised

almost half of promotions

(48.4%), as well as hires

(47.6%). Both these levels

exceed the overall

representation of women at

this level (43.5%).

47%

Among men and women

who left their rms to

join/start a competing rm or

join another industry, 47% did

so for compensation reasons.

A lack of opportunities/

career progression was cited

by 48.4%.

29.2%

Among the Canadian

men at the senior level

that departed their

rms in the past year,

nearly three in ten

(29.2%) cited joining

another industry as

a reason.

11.8%

The lowest proportion of

departures for Canadian CRE

women was among senior-level

professionals (11.8%). At the

average Canadian firm, the

proportion of women who left was

below those hired for each level,

except executive management.

Data is reflective of the 18.6% of respondents who completed the survey on behalf of North America and have employees in Canada. Demographic breakdowns reflect average values.

Executive

management

Senior-level

professionals

Mid-level

professionals

Junior-level

professionals

% of employee population

Men

(74.5%)

Women

(25.5%)

Men

(66.7%)

Women

(33.0%)

Men

(56.3%)

Women

(43.5%)

Nonbinary

(0.2%)

Men

(49.1%)

Women

(50.5%)

Nonbinary

(0.4%)

Total hired in past year 83.3% 16.7% 71.3% 28.7% 51.9% 47.6% 0.5% 47.6% 52.4% –

Total promoted in past year 72.7% 27.3% 70.2% 29.8% 51.6% 48.4% – 48.0% 50.7% 1.3%

Total departed in past year 76.4% 23.6% 88.2% 11.8% 55.2% 44.8% – 55.8% 44.2% –

Employee demographics – US

Global Real Estate DEI Survey Volume III 23

CONTENTS

This section provides highlights of employee demographic metrics for North America.

Specic analyses include:

• Gender & race/ethnicity demographics by seniority

• Real estate function demographics by gender

• Real estate function demographics by race/ethnicity

• Hires, promotions & departures by gender & race/ethnicity

• Reasons for departure

• Carried interest and equity/equity-like currencies allocation by gender & race/ethnicity

Note: Participants who completed the survey on behalf of their North American operations (79.2%) were given the option to submit demographic data for Canada, the United

States, or both. Responses in this section are based on the 69.5% of total participants who submitted demographic data for employees in the US.

The nonbinary category has only been included where there was sufficient data to report on it.

As the sample of respondents changes from year to year, conclusions based on changes should be interpreted cautiously.

An Excel spreadsheet containing full demographic data collected for the United States is provided to Survey respondents.

US DEMOGRAPHICS BY GENDER & SENIORITY

Global Real Estate DEI Survey Volume III 24

EMPLOYEE DEMOGRAPHICS US

Men

Women

Nonbinary

58.6% 41.4%

57.5% 42.5%

Junior-level professionals

(all other sta)

Mid-level professionals

Senior-level professionals

Executive management

Board of directors

Company overall

2022

2023

76.7% 23.3%

74.6% 25.4%2022

2023

74.3% 25.7%

77.0% 23.0%2022

2023

67.9% 32.0%

0.1%

70.4% 29.6%2022

2023

54.6% 45.4%

55.3% 44.7%2022

2023

49.9% 50.1%

50.2% 49.8%2022

2023

While the representation of women at CRE rms in the US dipped at the company level to 41.4% in 2023 from 42.5% in 2022,

women have made gains at every level within the rm except board of directors. Year on year changes may be due to

changes in the sample of responding rms, however the data shows women at the executive management level witnessed

the most signicant gains, up 2.7% in 2023 to 25.7%. The proportion of women at the average rm ranges from 23.3% at the

board level to 50.1% at the junior level.

Data is reflective of the 69.5% of respondents with employees in the United States. Demographic breakdowns reflect average values.

US DEMOGRAPHICS BY ETHNICITY & SENIORITY

Global Real Estate DEI Survey Volume III 25

EMPLOYEE DEMOGRAPHICS US

The chart below shows the demographics of full-time employees by ethnicity and seniority at CRE rms in the US. At the

company level, the proportion of employees of color fell from 31.3% in 2022 to 29.7% in 2023, albeit above the 28.8% seen in

2021, although this may be due to changes in the sample of respondents. At the junior level, 41.4% of professionals are from

underrepresented racial/ethnic groups.

White

Total POC

Did not disclose/specify

68.8% 29.7%

64.6% 31.3%

Junior-level professionals

(all other sta)

Mid-level professionals

Senior-level professionals

Executive management

Board of directors

Company overall

2022

2023

82.4% 14.6%

90.7% 9.3%2022

2023

85.0% 14.7%

82.0% 15.6%2022

2023

82.4% 16.7%

77.2% 18.6%2022

2023

69.9% 27.9%

66.9% 29.0%2022

2023

57.3% 41.4%

54.1% 41.1%2022

2023

Data is reflective of the 69.5% of respondents with employees in the United States. Demographic breakdowns reflect average values.

US DEMOGRAPHICS FOR POC BY ETHNICITY & SENIORITY

Global Real Estate DEI Survey Volume III 26

EMPLOYEE DEMOGRAPHICS US

The overall ethnic composition of employees in US CRE rms is 68.8% white, 29.7% POC and 1.5% undisclosed. This

proportion is most closely mirrored at the mid-level. At the junior level, over four in ten junior-level professionals are people

of color. Professionals at the highest levels of the rm are overwhelmingly white – over eight in ten. As in prior years, the

executive management level is less balanced, comprised 85% of white professionals.

Data is reflective of the 69.5% of respondents with employees in the United States. Demographic breakdowns reflect average values.

2023

White

Total POC

Did not

disclose/

specifyAsian

Hispanic or

Latino

Black or

African

American

Multiracial

(two or more

races)

Native

Hawaiian or

other Pacific

Islander

American

Indian or

Alaska Native

Company overall 68.8% 9.8% 9.4% 7.2% 2.8% 0.2% 0.3% 1.5%

Board of directors 82.4% 5.0% 3.0% 5.7% 0.7% – 0.2% 3.0%

Executive management 85.0% 7.0% 3.8% 2.4% 1.3% – 0.2% 0.3%

Senior-level professionals 82.4% 7.4% 3.8% 3.4% 1.8% 0.1% 0.2% 0.9%

Mid-level professionals 69.9% 9.6% 8.6% 6.4% 2.4% 0.3% 0.6% 2.2%

Junior-level professionals

(all other sta)

57.3% 10.5% 14.9% 11.2% 3.9% 0.7% 0.2% 1.3%

9.8%

The largest group of employees from an underrepresented racial/ethnic group is Asians,

which comprise 9.8% of professionals at an average US CRE rm. The next two largest

groups are Hispanic/Latino at 9.4% and Black or African American at 7.2%. Professionals

from each of these groups make up over 10% of employees at the junior level.

5.7%

The largest representation of people of color at the

board of director level is Black or African Americans, at

5.7%. This compares with 7.2% at the company overall

and 11.2% at the junior level.

US CRE FUNCTIONS BY GENDER & RACE/ETHNICITY

Global Real Estate DEI Survey Volume III 27

The tables on this page

depict the percentage of

roles held by men/women

and by white/POC

employees. Where the

overall representation at

US CRE firms is

approximately 60/40

men/women and 70/30

white/POC, numerous

disparities are apparent in

real estate functions. The

top three CRE functions

held by women are leasing

(60.6%), property

management (56.5%) and

IR & reporting (56.2%). For

underrepresented

racial/ethnic groups, the

top three functions are

engineering/maintenance,

property management

and leasing. In the

previous Survey, the

capital raising and IR &

reporting were grouped as

one function.

EMPLOYEE DEMOGRAPHICS US

Top 10 CRE roles held by men

(58.6% company overall)

2023 2022

Engineering/maintenance 91.4% 93.3%

Capital markets 79.1% 75.3%

Transactions 78.3% 80.0%

Research 75.0% 74.9%

Capital raising* 73.4% –

Construction/architecture 73.2% 71.5%

Portfolio management 73.2% 76.4%

Development 70.1% 72.0%

Asset management 69.9% 70.7%

Loan orig/underwriting/srvc 66.0% 65.8%

Top 10 CRE roles held by women

(41.4% company overall)

2023 2022

Leasing 60.6% 58.4%

Property management 56.5% 60.7%

IR & reporting* 56.2% 56.8%

Securities 42.2% 20.2%

Loan orig/underwriting/srvc 34.0% 34.2%

Asset management 30.1% 29.3%

Development 29.9% 28.0%

Construction/architecture 26.8% 28.5%

Portfolio management 26.7% 23.6%

Capital raising* 26.6% –

* In 2022, data was collected for investor relations (capital raising/reporting/ marketing/support). This year, that job function was divided into capital raising and investor relations (IR) &

reporting. Data is reflective of the 69.5% of respondents with employees in the United States. Demographic breakdowns reflect average values.

Top 10 CRE roles held by white professionals

(58.8% company overall)

2023 2022

Transactions 79.2% 83.2%

Capital markets 78.8% 78.4%

IR & reporting* 77.8% 75.7%

Asset management 77.1% 75.1%

Portfolio management 75.9% 72.6%

Development 75.7% 73.0%

Construction/architecture 75.3% 74.0%

Securities 74.6% 68.1%

Capital raising* 74.3% –

Loan orig/underwriting/srvc 71.8% 59.8%

Top 10 CRE roles held by people of color

(29.7% company overall)

2023 2022

Engineering/maintenance 54.9% 42.9%

Property management 40.5% 41.4%

Leasing 32.6% 34.1%

Research 30.1% 28.1%

Capital raising* 24.6% –

Securities 24.3% 28.8%

Loan orig/underwriting/srvc 23.5% 35.0%

Portfolio management 23.2% 24.5%

Construction/architecture 22.5% 20.8%

Asset management 22.0% 19.2%

US HIRES, PROMOTIONS & DEPARTURES

Global Real Estate DEI Survey Volume III 28

EMPLOYEE DEMOGRAPHICS US

Data is reflective of the 69.5% of respondents with employees in the United States. Demographic breakdowns reflect average values. Data was not collected for the category did not disclose/specify.

A combination of tactics is crucial if rms are to deliver on DEI targets. In order to increase representation over time for any

given group within an organization, we must look at its current rate of representation. What follows are two-pages of data

showing how to analyze and understand the promotions, hires and departures data. This page provides an indepth look at

trends taking place at the senior level. The following page provides data for all other seniority levels. In short, to move the

needle on DEI the proportion of promotions and hires must be greater than the percentage of one group’s employee

population, and the departure rate lower.

7%

In 2023, women of color accounted for 7% of senior-level

departures. This is half the level of 2022, although this could

be due to changes in the sample of respondents.

17.9%

In the past 12 months, almost one-fth of hires at the senior

level were men of color. They also comprised 12.4% of

promotions.

40%

Survey respondents reported that women at

their rms, on average, were granted 40%

of the promotions at the senior level. Of

senior-level women promoted, three-

quarters were white and the remainder were

POC women. Women also accounted for

nearly as many hires (37.6%). At the

executive management level, 45% of hires

were women, although only 27.1% of

promotions were. The largest proportion of

departures were white men (59.8%).

Senior-level professionals

White men White women POC men POC women

% of total employee population 57.8% 24.5% 9.4% 7.3%

Total promoted in past year 47.6% 29.2% 12.4% 10.8%

Total hired in past year 44.2% 29.3% 17.9% 8.3%

Total departed in past year 59.8% 23.0% 10.2 7.0%

Senior level

Women make up 32% of the US

CRE workforce at the senior level.

The promotion rate of 40%, hiring

rate of 37.6% and attrition rate of

30% indicates a positive trend

towards increased representation

of women at this level.

This trend is also evident among

senior-level professionals from

underrepresented racial/ethnic

groups, where 26.2% of hires and

23.2% of promotions went to

POC, which exceeds the current

employee population of 16.7% as

well as 17.2% departure rate.

However, the data shows twice as

many POC men versus POC

women were hired at the senior

level. Additionally, more men

from underrepresented

racial/ethnic groups were

promoted than women, and more

men than women also departed.

US HIRES, PROMOTIONS & DEPARTURES continued

Global Real Estate DEI Survey Volume III 29

EMPLOYEE DEMOGRAPHICS US

Executive management

White

men

White

women

POC

men

POC

women

% of employee population 64.3% 20.7% 9.7% 5.0%

Total promoted in past year 60.9% 15.9% 12.0% 11.2%

Total hired in past year 35.8% 38.2% 19.2% 6.8%

Total departed in past year 53.9% 30.4% 7.3% 8.4%

Data on promotions, hires and retention by level of seniority at US CRE rms is presented below. Employees at the junior level

are the most equally distributed among white men, men of color, white women and women of color. However, white men, as

well as men and women from underrepresented racial/ethnic groups departed their rms at a higher rate than their

employee population. While 17% of mid-level hires were of POC men, only 10.7% of promotions were.

Mid-level professionals

White

men

White

women

POC

men

POC

women

% of employee population 40.4% 29.5% 13.1% 14.8%

Total promoted in past year 42.2% 31.9% 10.7% 15.1%

Total hired in past year 36.3% 28.7% 17.0% 17.8%

Total departed in past year 38.3% 31.3% 15.5% 14.9%

Junior-level professionals (all other staff)

White

men

White

women

POC

men

POC

women

% of employee population 29.9% 27.4% 19.4% 22.0%

Total promoted in past year 31.0% 28.7% 19.6% 20.3%

Total hired in past year 29.6% 24.2% 23.0% 23.2%

Total departed in past year 30.8% 23.3% 21.5% 24.2%

Data is reflective of the 69.5% of respondents with employees in the United States. Demographic breakdowns reflect average values. Data was not collected for the category did not disclose/specify.

6.8%

Among executive

management hires in the past

year, only 6.8% were of POC

women. On the other hand,

38.2% of hires were of white

women, the highest among

all groups.

20%

POC men and women each

comprised about 20% of

promotions among junior-level

employees. For POC men, this

proportion of promotions is

nearly double that of the

executive management and

mid-levels.

The main reason for employee departure where known

is to join or start a competing rm. More than half of

men both white and POC did so, while three to four in

ten women cited this reason for leaving their

organizations. About the same percentage of white

men and women retire, as do those from

underrepresented racial/ethnic groups.

Both POC men and women were more likely to leave

for other family care (3.9% and 5.5%, respectively) than

their white counterparts (11.2% and 3.3%, respectively).

58.8%

The top reason men cited for leaving was to join or start a

competing rm. This was particularly acute for men of

color. Where 52.4% of white men left for this reason, almost

60% of POC men sought opportunities elsewhere. About

17.7% of POC men left to join a competing industry, while

26.2% of white men cited the same reason.

US REASONS FOR DEPARTURE

Global Real Estate DEI Survey Volume III 30

EMPLOYEE DEMOGRAPHICS US

The data below shows, where available, reasons for employee departures at US CRE rms. In over 90% of cases, reasons are

unknown. However, data where available can provide insight into how rms can better retain talent. Data is more readily

available for white employees than for professionals from underrepresented racial/ethnic groups.

* Care for any family member other than a minor child (e.g., disability care, geriatric care, hospice care, etc.)

Note: Insufficient data was received to report on Board of directors departures.

The prior demographics questions provided averages of the employee demographic breakdowns for each firm. The data on this page represents the aggregated data for all departing employees at the 69.5% of participating firms with employees in

the US. Data was not collected for the category did not disclose/specify.

0%

No men reported departing due to childcare. Only

4% of women did: 2.2% by white women and

1.8% by POC women. Both POC men and women

were more likely to leave for other family care

(3.9% and 5.5%, respectively) than their white

counterparts (11.2% and 3.3%, respectively).

23.6%

Women of color cited

personal health as the

third main reason for

departure. This is more

than twice the level of

other groups.

White

men

POC

men

White

women

POC

women

% of departures with reason known 8.5% 5.2% 9.1% 5.5%

Childcare – – 2.2% 1.8%

Family care* 1.2% 3.9% 3.3% 5.5%

Joining/Starting a competing rm 52.4% 58.8% 44.5% 34.5%

Joining another industry 26.2% 17.7% 26.1% 27.3%

Personal health 7.1% 11.8% 10.9% 23.6%

Retirement 13.1% 7.8% 13.0% 7.3%

% of departures with reason not known/given 91.5% 94.8% 90.9% 94.5%

US CARRIED INTEREST AND EQUITY/EQUITYLIKE CURRENCIES ALLOCATION

Global Real Estate DEI Survey Volume III 31

EMPLOYEE DEMOGRAPHICS US

* Carried interest allocation was only completed by firms identified as REPE/REIMs in Question 3.

Equity-like currencies include real equity ownership, as well as currencies designed to economically mimic ownership interests (e.g., profit sharing programs). Responses are reflective of the 31.6% of participants with employees in the US that offer

equity/equity-like currencies and/or carried interest to their employees. Demographic breakdowns reflect average values. Data was not collected for the category did not disclose/specify.

4.8%

Women of color received

4.8% of equity and equity-

like distributions, despite

comprising 14.3%

of professionals at the

average firm. Men of color

received 12.3% of equity

awards.

82.9% and 80.6%

Within US CRE firms, white professionals receive the lion’s share of carried

interest and equity or equity-like awards, with 80.6% and 82.9% of distributions

made to this group despite making up 68.8% of overall FTEs within the average

firm. In particular, white men comprise less than half of all professionals (42.4%),

but receive the majority of carried interest (66.2%) and equity or equity-like

awards (59.2%). On the other hand, white women received 14.4% of carried

interest and 23.7% of equity distributions despite making up over a quarter of

employees (26.4%).

13.3%

POC men received

13.3% of carried

interest. They also

received 12.3% of

equity or equity-like

currency awards,

versus the 59.2% that

went to white men.

Data on remuneration serves the purpose of assisting companies in benchmarking themselves to their peers in areas that can

contribute to talent retention and promote equality. Within the US CRE industry, 79.5% of carried interest recipients were

men, up from 77.9% in 2022, although this may be due to changes in the sample of responding rms. Men were also awarded

71.5% of equity or equity-like currencies. Detailed information on these awards can be found in the accompanying

spreadsheets provided to respondents, categorized by race/ethnic group, company size and company type.

White

men

POC

men

White

women

POC

women

Company overall 42.4% 15.4% 26.4% 14.3%

Carried interest* 66.2% 13.3% 14.4% 6.1%

Equity/equity-like currencies 59.2% 12.3% 23.7% 4.8%

Global Real Estate DEI Survey Volume III 32

DEI program & initiatives

CONTENTS

This section outlines metrics related to DEI program structure. Specic analyses include:

• DEI programs & budgets

• Dimensions of diversity

• DEI goals & success

• DEI policies

• DEI decision-making

• Recruitment & retention strategies

• DEI partners

• Retention & promotion strategies

• Inclusive work culture strategies

• DEI metrics tracked

• Pay equity strategies

• DEI obstacles

Note: The Global Real Estate DEI Survey Volume III received 236 distinct submissions on behalf of 216 unique organizations. Asia-Pacific received 21 submissions to

comprise 8.9% of responses, Europe received 28 responses to comprise 11.9% of responses, and North America received 187 responses to comprise 79.2% of responses.

As the sample of respondents changes from year to year, conclusions based on changes should be interpreted cautiously.

An Excel spreadsheet containing full data on DEI programs & initiatives is provided to Survey respondents.

DEI PROGRAMS & BUDGETS

Global Real Estate DEI Survey Volume III 33

DEI PROGRAM & INITIATIVES

A rm’s commitment to DEI can be demonstrated in various ways, including having a program or some initiatives to address

inequality, establishing a formal committee to lead eorts, and dedicating budgets to doing so. According to Survey

respondents, 95.8% of rms address DEI in some measure, up slightly from 95.3% in 2022, although this may be due to

changes in the sample of responding rms. Some 36.3% of rms report having dedicated DEI budgets.

Do you have a dedicated budget?

30.4%

55.2%

14.4%

2

0

2

3

2

0

2

2

No

(26.1%)

No, our DEI initiatives are funded from the budgets

of other business areas (e.g., HR budget)

(37.6%)

Yes

(36.3%)

Note: Outer circle denotes 2023 data and inner circle represents 2022 data.

Data is reflective of the 95.8% of participants with either a formal DEI

program or some initiatives and/or policies.

Do you have a formal committee?

71.1%

28.9%

2

0

2

3

2

0

2

2

No

(36.3%)

Yes

(63.7%)

2

0

2

3

How do you address DEI?

53.6%

41.7%

4.7%

2

0

2

2

We do not have a

formal DEI program,

but we enact some

DEI initiatives

and/or policies

to improve DEI

at our company

(39.4%)

We have a formal

DEI program in place

at our company

(56.4%)

We do not

have a

DEI program

(4.2%)

Note: Outer circle denotes 2023 data and inner circle represents 2022 data.

A formal DEI program refers to a fully documented, holistic program that

has been approved by the firm’s senior leaders and adopted as a means of

directing, and ensuring accountability for, the firm’s DEI initiatives.

Note: Outer circle denotes 2023 data and inner circle represents 2022 data.

Data is reflective of the 95.8% of participants with either a formal DEI

program or some initiatives and/or policies.

DIMENSIONS OF DIVERSITY

Global Real Estate DEI Survey Volume III 34

2022

2023 57.0%

2022

2023 55.6%

2022

2023 47.5%

2022

2023 39.5%

2022

2023 38.1%

2022

2023 36.8%

2022

2023 36.8%

2022

2023 10.3%

2022

2023 57.8%

2022

2023 62.8%

Sexual orientation

Gender and/or gender identity

Race/ethnicity/nationality

93.9%

100.0%

79.1%

Age

66.8%

Family status*

5.1%

Physical disability (visible)

57.1%

Physical disability (not visible)

56.1%

Mental health condition

44.4%

Religion

49.5%

Veteran status**

42.3%

Refugee status

41.8%

Socioeconomic background

38.3%

Mental or cognitive disability/neurodiversity

10.2%

2022

2023 96.4%

2022

2023 93.7%

2022

2023 72.6%

DEI PROGRAM & INITIATIVES

This chart shows the diversity dimensions addressed by the average CRE organization’s DEI initiatives. Globally, over nine in

ten rms address race/ethnicity/nationality (96.4%), followed by gender and/or gender identity (93.7%). The next dimensions

most addressed are sexual orientation (72.6%), age (62.8%) and family status (57.8%). Physical disabilities both visible and

invisible are addressed by over half of respondents.

* Family status includes: marriage/partnership status, parent/guardian status, caregiver status. ** Veteran status was only asked of participants completing the survey on behalf of their North American operations.

Data is reflective of the 95.8% of participants with either a formal DEI program or some initiatives and/or policies.

DEI GOALS AND SUCCESS

Global Real Estate DEI Survey Volume III 35

DEI PROGRAM & INITIATIVES

Inclusion of written goals/objectives

Yes, we set both

quantitative/measurable

and qualitative goals

(28.4%)

Yes, we have

qualitative goals

(23.9%)

Yes, we set quantitative/

measurable goals

(15.9%)

No, we do not set

formal/written goals/

objectives, but we plan to do

so within the next 12 months

(15.9%)

No, we do not set formal/written

goals/objectives, and we do not

currently plan to do so

(15.9%)

This dataset shows the extent to which CRE rms commit to DEI goals/objectives, and what they consider a successful

outcome. Of the rms that have a DEI program or some initiatives/policies, almost seven in 10 (68.2%) set quantitative and/or

qualitative goals. Having greater diversity throughout the organization continues to be the top measure of success as voted

by 80.8% of respondents, followed by improved employee engagement/productivity at 64.7% of rms. Dierences in data

from year to year may be due to changes in the sample of responding rms.

Data is reflective of the 95.8% of participants with either a formal DEI program or some initiatives and/or policies.

Most important outcomes

Greater diversity throughout

the organization

80.8%

Improved employee

engagement/productivity

64.7%

Greater diversity at the

senior leadership level

46.4%

Higher employee

retention

49.1%

Improved decision

making/improved

rm performance

41.5%

Improved rating/ranking

from third-party evaluation

7.1%

Up from 78.5%

Down from 57.0%

Up from 60.5%

Up from 42.5%

Down from 46.0%

Up from 6.5%

Data is reflective of the 95.8% of participants with either a formal DEI program or some initiatives and/or policies.

23.9%

Respondents cited creating or supporting affinity groups focused on

underrepresented groups as the fifth most impactful DEI outcome, with

over two in five firms that implement this strategy ranking it as one of their

most impactful.

25.5%

One-quarter of firms that currently provide DEI-related training

consider it one of their most impactful initiatives, with only

creating scholarships/internships for underrepresented groups

ranking higher.

TEN MOST IMPACTFUL DEI POLICIES

Global Real Estate DEI Survey Volume III 36

DEI PROGRAM & INITIATIVES

Which policies currently implemented have the greatest impact in achieving DEI goals? Participants were asked to rank the

three DEI polices they deemed to be the most impactful. What follows is a top 10 list of the most impactful DEI policies from

all Survey respondents. Shooting to the top of this year’s ranking is the creation of scholarships/internships to increase the

number of underrepresented individuals in candidate pools. Dierences in data from year to year may be due to changes in

the sample of responding rms.

2023 2022

Creating scholarships/internships to increase the number of underrepresented individuals in candidate pools

31.6% 18.0%

Providing DEI-related training 25.5% 14.6%

Oering programs that provide a work/life balance (e.g., childcare, exible work arrangements) 25.1% 33.7%

Ensuring there are individuals from underrepresented groups in the candidate pool before making a hiring decision

25.0% 26.3%

Creating or supporting anity groups focused on underrepresented groups 23.9% 13.2%

Gathering and analyzing feedback from employees on DEI practices and outcomes (e.g., engagement surveys)

18.4% 12.2%

Holding events to celebrate/promote/inform about specic groups (e.g., Pride Month, Black History Month, International Women’s Day, etc.) 17.8% 14.6%

Ensuring the hiring team includes employees from underrepresented groups

13.8% 9.8%

Evaluating employees based on well-dened, pre-determined criteria (job performance reviews) 13.8% 20.5%

Providing mentorship or formal sponsorship/advocacy for individuals from underrepresented groups

12.9% 6.3%

Determining who, or which

party, holds the ultimate

responsibility for achieving

corporate goals through DEI

initiatives is important. In this

year’s Survey, nearly one-third

of respondents (32.3%) said

that the C-suite (executives

excluding the chief diversity

ocer) takes the lead in

decision-making on DEI policies

and initiatives. Last year, one-

quarter of respondents said so.

There has been a signicant

decrease from 27% to 18.6% of

companies making decisions

through a DEI team or

committee, although it remains

the second most popular

method. In third place is

decision-making by a senior-

level DEI employee, including a

chief diversity ocer, which has

increased from 11.5% to 16.8%.

There has also been a decline in

those giving this responsibility

to the board of directors, from

6.5% to 3.1%.

32.3%

25.0%

18.6%

27.0%

16.8%

11.5%

14.2%

12.0%

8.0%

9.5%

3.5%

2.0%

6.5%

3.5%

1.5%

3.1%

Board of directors

Other senior leadership*

Other committee**

CEO

Human resources

A senior-level DEI employee

(including chief diversity ocer)

DEI team/committee

C-suite (other executives

excluding chief diversity ocer)

2022

2023

2022

2023

2022

2023

2022

2023

2022

2023

2023

2023

2022

2023

DEI DECISIONMAKING

Global Real Estate DEI Survey Volume III 37

DEI PROGRAM & INITIATIVES

* Other senior leadership includes: any higher-level positions that are not covered under the other categories listed, including positions such as managing directors, partners and senior/executive vice presidents of non-HR departments.

** Other committee includes: ESG committee, risk committee.

Data is reflective of the 95.8% of participants with either a formal DEI program or some initiatives and/or policies.

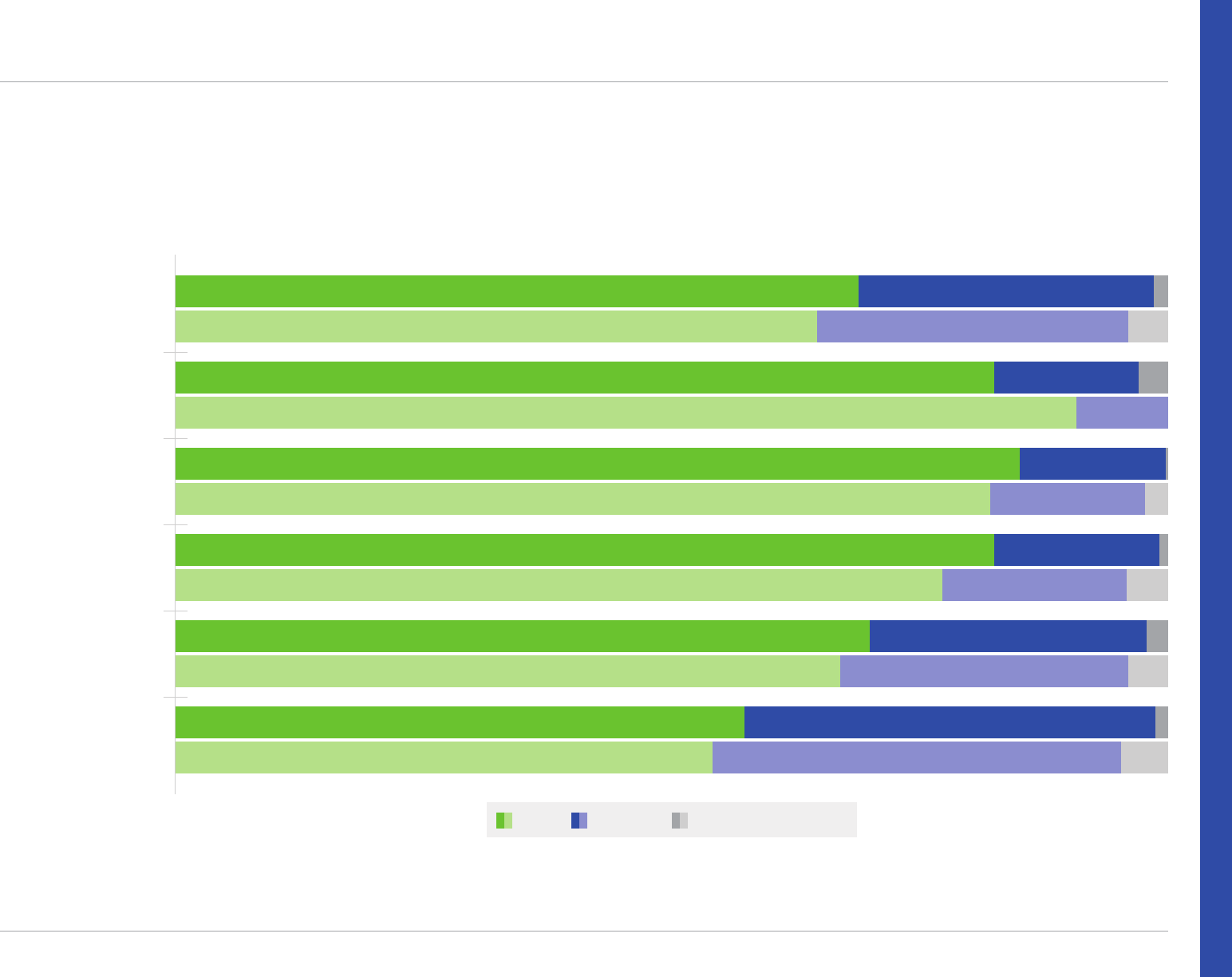

28.2%10.7%61.1%

31.6%10.3%58.1%

22.6%13.2%64.2%

16.7%17.5%65.8%

23.0%10.3%66.7%

13.7%22.9%63.4%

2022

2023

2022

2023

2022

2023

Creating scholarships/internships to increase the number of

underrepresented individuals in candidate pools

Broadening or being exible on educational and

experience requirements for new hires

19.6%18.4%62.0%

15.6%18.1%66.3%

2022

2023

Ensuring there are individuals from underrepresented groups

in the candidate pool before making a hiring decision

21.3%12.4%66.3%

27.8%10.2%62.0%

2022

2023

Reaching outside the CRE industry to increase your pool

of candidates from underrepresented groups

Reviewing postings, application processes, and assessments

to eliminate adverse impact or bias

Currently implemented

Plan to implement in the next 12 months

No current plans to implement

58.1%

Nearly six in ten (58.1%) rms said they are creating scholarships or

internships to increase the number of underrepresented individuals

in candidate pools. A further 10.3% plan to do so in 12 months.

65.8%

Almost seven in ten (65.8%) respondents say they are reviewing their processes

to eliminate adverse impact or bias when hiring. This is the top strategy for

increasing the number of hires from underrepresented groups.

TOP STRATEGIES FOR RECRUITMENT & RETENTION

Global Real Estate DEI Survey Volume III 38

DEI PROGRAM & INITIATIVES

The ve most popular strategies for boosting recruitment and retention of underrepresented groups are shown below.

Respondents continue eorts to ensure representation of candidates from underrepresented groups in candidate pools and

to broaden the scope of requirements of new hires. For a full list of strategies on recruitment and retention, please refer to the

accompanying spreadsheet sent to all Survey respondents.

TOP 5 DEI PARTNERS, BY REGION

Global Real Estate DEI Survey Volume III 39

DEI PROGRAM & INITIATIVES

Asia-Pacic CRE rms companies lean heavily on university alumni connections and campus diversity groups

to increase diversity within their organizations. The Urban Land Institute (ULI) also plays a signicant role by

oering two distinct partnerships for Asia-Pacic CRE rms to benet from: Women’s Leadership Initiative and

Young Leaders Group. Additionally, nearly one in ten rms in the region look to the Champions of Change

Coalition as a means to promote diversity.

Asia-Pacific

Europe

North America

In Europe, university alumni and campus diversity groups are commonly seen as go-to partners for increasing

diversity, similar to the Asia-Pacic region. The Urban Land Institute’s Young Leaders Group is also a signicant

partner for real estate rms surveyed. Moreover, Europe has access to specic organizations such as Real

Estate Balance and Women Talk Real Estate, which are frequently mentioned partners in the eort to foster a

more diverse pool of professionals.

In North America, the CRE Women Network (CREW) is most frequently cited as a partner by respondents. As in

Asia-Pacic and Europe, alumni networks and campus diversity groups remain important, as are Historically

Black Colleges and Universities, the latter of which is tapped into by one-third of respondents. SEO/PREA is

another major aide for diversity hiring initiatives. The complete lists of partners for all regions is available in an

Excel spreadsheet provided to Survey respondents.

University alumni and campus diversity groups 33.3%

ULI Women’s Leadership Initiative 19.0%

Women’s leadership groups within chambers

of commerce

9.5%

ULI Young Leaders Group 9.5%

Other 23.8%

University alumni and campus diversity groups 35.7%

ULI Young Leaders Group 32.1%

Women in Real Estate Network (WIRE) 28.6%

Real Estate Balance 21.4%

Other 39.3%

Commercial Real Estate Women Network

(CREW)

38.1%

University alumni and campus diversity groups 37.5%

Historically black colleges and universities 33.9%

Sponsors for Educational Opportunity/

PREA Foundation

30.4%

Other 31.0%

TOP 5 RETENTION & PROMOTION STRATEGIES

Global Real Estate DEI Survey Volume III 40

DEI PROGRAM & INITIATIVES

6.3%5.8%87.9%

7.3%6.1%86.6%

9.5%8.7%81.8%

11.7%18.6%69.7%

8.8%22.4%68.8%

3.9 3.992.2%

9.1%3.087.9%

8.0% 4.587.5%

2.9%

11.7%85.4%

2.9%

6.3%90.8%

Currently implemented

Plan to implement in the next 12 months

No current plans to implement

2022

2023

2022

2023

2022

2023

2022

2023

2022

2023

Providing DEI-related training

Evaluating employees based on well-dened,

pre-determined criteria (job performance reviews)

Implementing anti-discrimination policies with

whistleblowing/complaint mechanisms

Oering programs that provide a work/life balance

(e.g., childcare, exible work arrangements)

Outlining job requirements and setting clear expectations

87.9%

Almost nine in ten (87.9%) of respondents say they oer programs that

provide work/life balance (such as childcare and exible work arrangements)

and a further 3% plan to implement this in the next 12 months.

18.6%

Almost seven in ten rms (69.7%) provide DEI-related training as a

retention and promotion strategy. Among rms that do not yet provide

this, 18.6% intend to introduce such training within 12 months.

A counterpart to getting diverse employees through the door is retaining and promoting them. The Survey shows a

consistent approach from CRE firms when it comes to strategies to keep and grow talent from underrepresented groups.

Outlining job requirements and setting clear expectations is the top strategy, followed by offering work/life balance

programs and implementing anti-discrimination policies. For a full list of strategies on retention and promotion, please

refer to the accompanying spreadsheet sent to all Survey respondents.

11.4%87.1%

19.2%5.5%75.3%

21.3%75.3%

24.7%72.8%

19.2%4%76.8%

4.785.1%

16.2%82.1%

15.4%77.7% 6.9%

3.4

8.8% 19.6%71.6%

7.8%

10.2%

10.8%81.4%

Currently implemented

Plan to implement in the next 12 months

No current plans to implement

2022

2023

2022

2023

2022

2023

2022

2023

2022

2023

Ensuring dress code requirements are inclusive

(e.g., provisions for natural hair,

religious garments/accessories, etc.)

Providing a breastfeeding room

Expansion of time o

(e.g., additional holidays, mental health days, etc.)

Providing access to external mental health/

family counseling/non-work-related support

Promoting inclusive employee social events

1.7

2.5

1.5

TOP 5 INCLUSIVE WORK CULTURE STRATEGIES