Product / Service

Bereavement

support

What to do when someone close to you dies

A step-by-step guide

We hope this guide answers any questions you might have.

It gives you practical information on how to notify and

confirm a death, what happens to someone’s accounts when

they die, what you’ll need to close their accounts and how to

get help with funeral costs.

We also appreciate that sorting out these issues may be the

last thing on your mind. So if you’d like to talk to someone to

help you through the steps you need to take, have a look at the

‘contact us’ page at the back of this leaflet. It tells you how you

can get in touch.

To help you remember everything you need to do, we’ve

included a checklist at the back too.

3

Contents

The legal terms and phrases explained Page 4

Registering the death Page 5

Letting us know Page 6

Letting other financial providers know Page 7

Help with expenses Page 8

The will and the estate Page 9

Dealing with their tax and benefits Page 10

What we need to see to close a Nationwide account Page 10

What happens to the accounts they held Page 11

Debt with Nationwide Page 16

Payment information Page 16

Checklist Page 19

Useful websites Page 22

Contact us Page 23

4

The legal terms and phrases explained

There are many legal terms used when someone dies. Here’s some of the most common

ones you’re likely to come across.

Administrator

The person appointed when either no will can be found or there is no executor to carry out

the intentions of the will.

Beneficiary

Someone who is entitled to receive a specific gift, sum of money or share of the estate.

Death Certificate

This is either the medical document issued by a qualified doctor, certifying the death of a

person and stating the cause if known, or more commonly the legal document you get

afterwards from a registrar, confirming the date, location and cause of the person’s death.

Estate

A person’s estate includes everything they own and everything that’s registered in their name.

Executor

The person or persons named in a will to deal with the estate following a person’s death.

Grant of Probate

This is the official document that confirms to the executors that they have authority to act

and which validates the will. Where there’s a will, this will be a ‘Grant of Probate’. Where

there’s no will, it will be ‘Letters of Administration’. In Scotland, this is known as ‘Certificate

of Confirmation’.

Inheritance Tax

A tax on the estate that generally applies when someone dies and when the value of their

estate is above a specific threshold. The tax is paid before the estate can be distributed to

the beneficiaries.

Intestate/Intestacy

When someone dies without leaving a valid will in place.

Letters of Administration

This is the official document that appoints people to handle a person’s estate, where there is

no will, no executors appointed in the will, no executors still living, or no executors willing to

carry out the executor’s duties.

Personal representative

This is the executor or administrator managing the deceased’s estate.

The personal representative is responsible for administering the estate, which means they

need to collect all the assets and pay all bills and debts that need to be paid. Depending on

how much money and assets the person who died had, the personal representative may

need to apply for a Grant of Probate – if so, then no accounts can be closed until they have

this document.

5

Probate

Probate is the legal process of dealing with someone’s estate after they’ve died. It involves

collecting all of the person’s assets; their money, property and belongings – as well as

settling debts and paying any taxes due, then sharing out what’s left as directed in the will.

It’s usually the executor of their will who administers the estate, shares out its assets and

clears its debts. To get authority to do that, they usually need to get a legal document called

a ‘Grant of Probate’. For more information on how to do this, please visit the government

website on gov.uk

Will

A legal document which indicates who should benefit from the estate and how. It also

appoints an executor to administer and distribute the estate, and may appoint guardians or

contain funeral wishes.

Registering the death

The government’s website – gov.uk/registeradeath – is a good place to find everything

you need to know including who can register the death and what they’ll need to do.

Once you’ve registered the death, you’ll be given:

•

a death certificate, and

•

a certificate for burial or cremation.

It’s a good idea to ask for extra copies of the death certificate, as many organisations will

need to see an original version (there can be a fee for this).

The government’s Tell Us Once service

When someone dies, there are a number of government departments you’ll need to

inform. To help, the government offers a Tell Us Once service which lets you contact

several departments in one go, such as:

•

Department of Work and Pensions

•

Passport Office

•

HMRC

•

Local Authority

•

DVLA

This service is offered by most local authorities but isn’t available in Northern Ireland or

if the person was living permanently abroad. You can access this service online or by

phone when you register the death. You’ll need a unique reference number from the

registrar to do this.

If you don’t want to use Tell Us Once or it’s not available to you, our checklist at the back

includes the individual government departments you may need to tell about the death.

The government provides more guidance at www.gov.uk/afteradeath

6

Letting us know

If you don’t yet have a death certificate

If you don’t yet have the death certificate and want to safeguard the account and stop

marketing, you can let us know by making an appointment in your local branch, by phone on

0800 464 3018, online through the Bereavement Support section of our website, or by

writing to Bereavement Services (address on page 22).

What we’ll need to know

•

Their full name, address, date of birth and the date of death.

•

The notifier’s name, address, telephone number, relationship to the deceased and,

optionally, their email address.

•

The personal representative’s name and address (if you know this yet) – this tells us who

to write to and who we can give information to.

What we’ll do once you let us know

•

If we know who the personal representative is, then we’ll write to them to let them know

what the next steps are. If this information is not provided we will take reasonable steps

to identify the personal representative so that we can get in touch.

•

We will restrict any withdrawals on sole accounts to safeguard them.

•

We will suppress any marketing (please note there may be occasions when marketing

material continues to arrive because it was already prepared for mailing, but this should

only be for a short period of time)

Once you have a death certificate

Once you have the original death certificate, or the coroner’s interim certificate, you can

register the death with us. Please just take the certificate or a certified copy into a branch or

send it to us by writing to Bereavement Services (address on page 22).

A ‘certified copy’ is a photocopy of the original document that has been certified to confirm

the original has been seen. We can do this for you in branch. When you register the death at

the registrar’s office you can alternatively pay for several copies of the death certificate so

you don’t have to go to the trouble of getting someone to endorse (certify) a photocopy.

If you’d like to go through the steps you need to take with one of our advisers in branch, this

is a good time to make an appointment. You can find your local branch’s phone number at

nationwide.co.uk/branchfinder or phone the bereavement Helpdesk on 0800 464 3018

If you’re the personal representative and you’re not a Nationwide member, we’ll need to see

your D such as a valid full UK passport or valid full photocard driving licence and a recent

proof of address such as a utility bill or bank statement. You can find details of acceptable

D at nationwide.co.uk or ask in branch or call us.

Your information may also be used for the prevention of money laundering. For more details

on how Nationwide use your information, please see nationwide.co.uk/privacy.

We’ll write to the personal representative to let them know what the next steps are and how

and when the accounts will be closed.

7

Letting other nancial providers know

If the person who died had accounts with a number of different providers, there’s a free

online Death Notification Service (DNS) that lets you complete one notification that will be

sent to all the participating financial institutions you need to contact. For more information,

please go to deathnotificationservice.co.uk

The providers taking part in this service include:

•

Nationwide

•

Bank of Scotland

•

Barclaycard

•

Barclays

•

Halifax

•

HSBC

•

Lloyds Banking Group

•

Santander UK

•

Scottish Widows

•

The Royal Bank of Scotland/NatWest.

The full list of member organisations is available on the DNS website.

Please note that this is an online notification service only. If you use it, those organisations

will update their records and contact you within ten days to let you know the next steps.

Help with expenses

Paying for the funeral

If you’re arranging the funeral, you may need to pay for this upfront. There may be a life

insurance policy or sole funeral plan that’s already paid for the funeral but if there isn’t we

can release money from the accounts of the person who’s died. If there isn’t enough money

in the account to pay all of the costs, we’ll release the available funds to help towards the

final bill.

To request funds for the cost of the funeral, please complete our ‘Personal Representative’s

request for funds to cover costs’ (F21) form and return it to us. To get hold of a copy of the

form, you can either:

•

find and print a copy from our website by searching ‘F21’

•

pick one up from one of our branches

•

or, give us a call on 0800 464 3018 and we can post one to you.

To return it to us, either take it to one of our branches or post it to Bereavement Services at

the address on page 22.

Please note if it’s an estimate we’ll only pay the deposit, if it’s the final invoice, we’ll pay the

full amount. All cheques will be made out to the Funeral Service provider. In exceptional

circumstances, you may be able to give us instructions to make an electronic payment

instead. There are more details about this in the ‘Payment information’ section of this

leaflet. You can call us on 0800 464 3018 if you want to discuss this with us.

If the funeral bill has been paid by the executor, as well as the funeral invoice, we’ll also need to

see a bank statement or credit card bill with their name and address, showing the payment.

Paying for Grant of Probate/Letter of Administration fees

You may need money to pay for other urgent expenses such as fees for Grant of Probate/

Letter of Administration. To cover these fees, just fill in a ‘Personal Representative’s request for

funds to cover costs’ (F21) form and return it to us in branch or by posting it to us at the

address on page 22. We don’t need to see the bill as we’ll make the cheque out to the court.

Paying Bills

We’re sorry, but we can’t release funds from the deceased member’s account to pay bills for

care home fees or utility bills. This is because there is generally an order of priority in which

the deceased’s estate debts should be settled. The Personal Representative of the estate will

manage all of this. Creditors such as care homes and utility providers will usually contact the

Personal Representative to manage the individual debts owed to them.

If you’d like some guidance on dealing with the financial affairs of someone who has died,

you may find these websites helpful:

Citizen’s Advice Bureau – citizensadvice.org.uk/family/deathandwills/dealingwiththe

financialaffairsofsomeonewhohasdied

Money Helper moneyhelper.org.uk/en/familyandcare/deathandbereavement/dealing

withthedebtsofsomeonewhohasdied

Bereavement Advice Centre bereavementadvice.org/topics/probateandlegal/insolvent

estates

8

9

The will and the estate

The will

If there’s a will, we won’t need to see it to close or release funds from an account.

You can find out more information about wills, probate and inheritance tax at

gov.uk/willsprobateinheritance

Dealing with the estate

After someone dies, their estate is shared out according to their will or given to their next of

kin if no will was left. A person’s estate includes everything they own and everything that’s

registered in their name, things like:

•

money (cash, bank or building society accounts, money owed by others)

•

property

•

personal possessions (such as jewellery or a car)

•

insurance policies

•

stocks and shares.

Personal Representative

Being a personal representative (the ‘executor’ or ‘administrator’) is an important role as it’s

that person’s responsibility to carry out the administration of the estate. This can include:

•

collecting all the assets of the estate

•

dealing with any paperwork

•

settling any debts, taxes, funeral and administration costs

•

appointing a solicitor

•

applying for probate where needed.

Dealing with the estate yourself

You can deal with the estate yourself rather than appointing someone else to do it.

You can find out more about Grant of Probate at gov.uk

Appointing someone to administer the estate

You might find it easier to appoint a solicitor, chartered accountant, specialist probate

service or bank to handle the administration. Many personal representatives do this. Before

you do, however, bear in mind you’ll have to pay for these services.

10

Dealing with their tax and benets

When someone dies, their tax, benefits and National Insurance will need to be sorted out

as soon as possible. There may be tax to pay, or their estate might be owed some tax back.

We can issue tax statements for the member’s sole accounts up until the date of their

death. If this would help, please call our bereavement helpdesk on 0800 464 30 18. Just

so you know, we’re only able to provide tax and interest information on joint accounts up

to the date the member died.

Inheritance Tax

If you’ve been named as the personal representative, you’ll be responsible for paying any

inheritance tax (HT) using funds from the person’s estate.

For payment of inheritance tax, please fill out a ‘HT423’ form and return it to us by post

(at the address on page 22) or by bringing it into one of our branches. You can search for

and download the form at gov.uk/inheritancetax. Once we receive the form we’ll pay

HMRC via an electronic payment.

You can find out more information about inheritance tax at gov.uk/inheritancetax

What we need to see to close a

Nationwide account

We’ll need to see different things to close an account depending on how much money is

held in it. The amount in the account also affects when the money can be released. We will

send you a ‘Request to Close Account(s)’ form when we have registered the death. If you’re

applying for a Grant of Probate, the original or certified copy of this document will need

to be sent to us, along with the request to close account forms.

Less than £50,000

We’ll need a completed ‘Request to Close Account(s)’ form.

£50,000+

We’ll need a completed ‘Request to Close Account(s)’ form and the Grant of Probate/

Letters of Administration.

What happens to the accounts they held

Current account

Joint current accounts

If the person who has passed away held a joint account, we’ll change the account to the

other account holder’s name only when we receive the death certificate. The other account

holder can then continue to use it.

Joint cards and chequebooks

We’ll cancel any cards and chequebooks that belonged to the person who died when we

receive the death certificate. You don’t need to return them. Any cards and chequebooks

owned by the other account holder won’t be affected.

Joint Direct Debits and standing orders

To cancel any Direct Debits, such as electricity or gas payments, the other account holder

should contact the relevant organisations.

To cancel any standing orders, the other account holder can either come into a branch or

call us on 03457 30 20 11. Lines are open 8am to 8pm, 7 days a week. They’ll need to give us

the account and payee details.

Sole current accounts

If the person who has passed away held a current account with us just in their name, it will

stay open until we receive the documents to close it.

Payments into the account, such as from the Department for Work and Pensions, may be

recalled.

Sole cards and chequebooks

We’ll cancel their card and chequebook when we receive the death certificate. You don’t

need to return them.

Sole Direct Debits and standing orders

Once we’ve received the death certificate, all Direct Debits and standing orders will be

cancelled. The personal representative will need to cancel any Direct Debits directly with

the organisations. They don’t need to do this for standing orders.

If there’s a Direct Debit to pay for home insurance, please check with the insurance

company that the house is still covered while the estate is being dealt with.

Overdrafts

If the account is overdrawn, the overdraft will need to be repaid from the estate.

Our probate partner, Phillips & Cohen Associates (UK), will contact the personal

representative to help with this. The personal representative can also phone them directly

on 0333 555 10 50. Lines are open MondayThursday 8am to 8pm, Friday 8am to 5.30pm

and Saturday 9am to 1pm (closed Sundays and bank holidays).

11

What happens to the accounts they held

Savings

Cash SAs

An SA remains open until it’s closed or administration of the estate is complete, whichever

is earlier. During this time, it maintains its taxfree status.

After 3 years, if the account hasn’t been closed, we’ll move the balance into a taxable savings

account. It stays there until the personal representative asks for the money to be released.

Inheriting an SA allowance

If you’re the spouse or civil partner of the person who has died, you may be able to inherit an

additional SA allowance.

Members who died on or before 5 April 2018

SAs were closed from the date that the member’s death was registered. Money is held in a

nonSA account until the personal representative asks for it. Any interest, dividends or

gains from after the date of death may be taxable (depending on allowances).

Bonds

Joint accounts

If the person who has passed away held a joint account, we’ll change the account to the

other account holder’s name only when we receive the death certificate. It then becomes

solely theirs.

Sole accounts

If the bond is only in the name of the person who died, it will remain open until we receive

the documents to close it. There are no fees to pay, even if the account is closed early. We

automatically cancel the bond certificates.

eBonds

Joint accounts

If the person who has passed away held a joint account, and had eBonds linked to that

account, we’ll change the account to the other account holder’s name only when we receive

the death certificate. The account and the eBonds then become solely theirs.

Sole accounts

Because eBonds are linked to a Nationwide current account, they’ll be closed along with that

current account when we receive the death certificate. There won’t be any charges.

12

13

Other savings accounts

Joint accounts

If the person who has passed away held a joint account, we’ll change the account to

the other account holder’s name only when we receive the death certificate. It then

becomes solely theirs.

Alternatively, the personal representative can close the account without having to pay

any fees or lose any interest. We’ll automatically cancel any related cards.

Sole accounts

An account that’s only in the name of the person who died remains open until we receive

the documents to close it.

Credit Card

If no money is owed on the card, we’ll close the account automatically when we receive

the death certificate.

Any outstanding money owed on the card will need repaying from the estate.

Our probate partner, Phillips & Cohen Associates (UK), will contact the personal

representative to help with this. The personal representative can also phone them

directly on 0333 555 10 50. Lines are open Monday to Thursday 8am to 8pm, Friday

8am to 5

:

30pm and Saturday 9am to 1pm (closed on Sundays and bank holidays).

If the account has a credit balance

The account will stay open until we receive the documents to close it.

If the person who died was the primary card account holder

The primary card account holder is the person who took out the card account with us

and was responsible for paying the bills.

The account will be closed when we receive the death certificate, and any additional

cards linked to it will be cancelled. Any additional card holder will need to apply for a

new credit card if they’re eligible.

If the person who died was an additional card holder on someone else’s

Nationwide credit card

Additional card holders have no responsibility for paying the bills. We’ll remove their

name from the account once we receive the death certificate, and the primary card

holder can continue to use the card.

14

What happens to the accounts they held

Mortgages

Once we’ve been told about the death, we’ll freeze the mortgage account. Doing this

means we won’t take any regular payments during that time, although interest will still

be charged.

• If it’s a joint account: we’ll freeze it for 3 months. After that time, we’ll recalculate

payments over the remaining term of the mortgage to take in to account any

increase in balance. If the remaining account holder or personal representative would

prefer not to have the mortgage frozen, they can call us and ask us not to do this.

• If it’s a sole account: we’ll freeze it for 12 months as standard – this period can’t be

cancelled. After that time, the mortgage will need to be repaid. We’ll recalculate

payments over the remaining term of the mortgage to take in any increase in balance.

The personal representative can set up a standing order or bank transfer payment if

they wish to continue making payments to the mortgage.

If the personal representative has any questions about this, they can call the

Bereavement Helpdesk on 0800 464 30 18. Lines are open MondayFriday 9am to 5pm,

and between 9am and 12pm on Saturdays. Or, by post to Bereavement Services at the

address on page 22.

Personal loan

Joint loans

If the person who has passed away held a joint loan, we’ll change the loan to the other loan

holder’s name only when we receive the death certificate. It then becomes solely theirs.

Sole loan accounts

If the loan is only in the name of the person who has died, we’ll let the personal

representative know how much needs to be repaid. The amount owed could be covered

by life or payment insurance. But if there’s no policy in place or it cannot cover the total

amount owed, it will need repaying from the estate.

Our probate partner, Phillips & Cohen Associates (UK), will contact the personal

representative to help with this. The personal representative can also phone them

directly on 0333 555 10 50. Lines are open Monday to Thursday 8am to 8pm, Friday

8am to 5

:

30pm and Saturday 9am to 1pm (closed on Sundays and bank holidays).

Investments

The person who has died may have had an investment plan with Nationwide. If so,

please contact our investments provider, Aegon, to discuss this.

You can phone Aegon UK on 0345 272 00 89.

15

Home insurance

If the policy is in the name of the person who died

If the person who has died was the other policy holder’s spouse or civil partner, we’ll let

our insurer know what’s happened. They can update the policy so it’s in the other policy

holder’s name, and the cover will continue until the probate is finished. To do this, the

insurance company will contact the personal representative to get some further details.

The personal representative can also phone them directly on 0800 145 60 60. Lines

are open 24 hours a day, 7 days a week.

Once probate is complete, the beneficiary will need to arrange a new policy.

If there are any changes at the property (for example, if it’s no longer lived in), the

personal representative will need to let the insurer know.

Finally, if the policy was paid by Direct Debit, the personal representative should check

that the house is still covered while the estate is being dealt with.

Joint policies

If the person who has passed away held a joint policy, we’ll notify our insurer when we

receive the death certificate. They will change the policy to the other account holder’s

name only and send them confirmation of this.

Trustee accounts

If there’s a trust deed

If there’s a trust deed for the account, it should explain what happens when a trustee dies.

If there’s no trust deed

If there’s no trust deed for the account, the personal representative of the deceased

trustee can choose to:

•

add a new trustee

•

leave it with any remaining trustee(s) to manage the account

•

transfer the account to the beneficiary

•

close the account.

If you’re the personal representative and not sure what to do, please get legal advice.

Life Insurance

The person who has died may have had a life insurance policy with Nationwide. If so,

please contact our life insurance provider, Legal & General, to discuss this.

You can phone Legal & General on 0345 674 07 83.

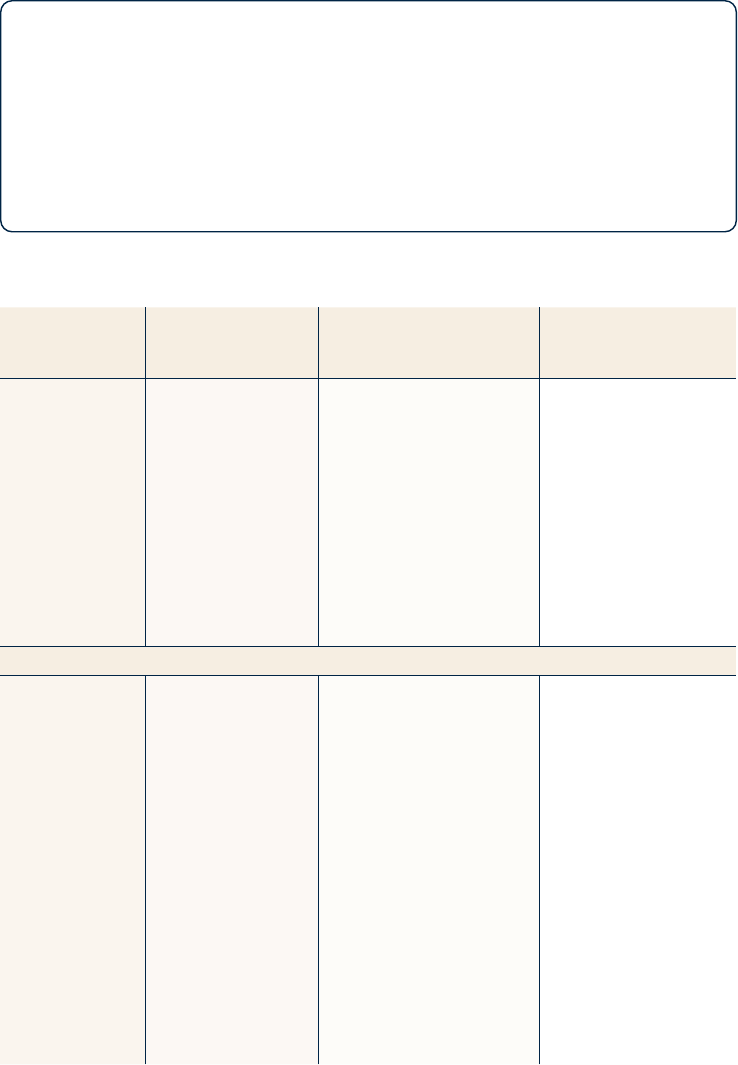

Payment information

Payment type When we receive

your payment

instructions

When payments

normally arrive at the

recipient’s bank

Can you cancel your

instruction?

Internal

Transfers (to a

Nationwide

account)

Once we have

received your

completed ‘Request

to Close Account(s)’

form, we may call

you to confirm the

payment details

with you, and your

payment instruction

may be taken on the

phone during that

conversation.

Your payment will arrive

within 1 working day of us

sending it. Payments are

made on working days only.

No, you cannot

normally cancel a

payment after we have

accepted your

instruction.

Payment types made by exception

CHAPS –

payments within

the UK in

pounds sterling

Once we have

received your

completed ‘Request

to Close Account(s)’

form, we may call

you to confirm the

payment details

with you (including

any transaction fee),

and your payment

instruction is given

to us on the phone

during that

conversation.

Your payment will arrive

within 1 working day of us

sending it. Payments are

made on working days only.

We’ll send the money from

the savings account to a

Nationwide Sundries

account, which supports

external payments.

Once the money is in our

Sundries account, we’ll

send the payment by

CHAPS. This payment will

arrive at the receiving bank

by the end of the next

working day following the

date of payment.

No, you cannot

normally cancel a

payment after we have

accepted your

instruction.

16

Debt with Nationwide

If there was any borrowing with us, such as a credit card, a loan or an overdraft in only their

name, that debt will need to be repaid, if the estate has enough money to cover it.

Our probate partner Phillips & Cohen Associates (UK) will contact the personal

representative to help with this. If you want to contact them directly, their phone number

is 0333 555 1050.

Please remember, we’re here to help so if you’ve got any questions about this, please call

our bereavement helpdesk on 0800 464 30 18.

17

SWFT – an

international

payment; or a

foreign currency

payment to

another account

within the UK

Once we have

received your

completed Request

to Close account(s)

form, we may call

you to confirm the

payment details

(including any

transaction fee) and

the exchange rate

that will apply to

your payment. Your

payment instruction

is given to us on the

phone during that

conversation.

For a payment in an EEA

currency or pounds

sterling to a country in the

EEA: your payment will

arrive at the receiving

bank within 1 working day.

For a payment to a country

within the EEA or the UK

that is not in an EEA

currency: your payment

will normally arrive within

4 working days.

Payments made outside

the EEA will take longer

– please ask us for details.

Payments are made on

working days only.

If the payment is being

made from a savings

account, we’ll send the

money from the savings

account to a Nationwide

Sundries account, which

supports external

payments.

No, you cannot

normally cancel a

payment after we have

accepted your

instruction.

SEPA Credit

Transfer – a

payment in

euros to an

account in the

Single Euro

Payments Area.

Once we have

received your

completed Request

to Close account(s)

form, we may call

you to confirm the

payment details

(including any

transaction fee) and

the exchange rate

that will apply to

your payment. Your

payment instruction

is given to us on the

phone during that

conversation.

Your payment will arrive

within 1 working day of us

sending it. Payments are

made on working days only.

If the payment is being

made from a savings

account, we’ll send the

money from the savings

account to a Nationwide

Sundries account, which

supports external

payments.

You can ask us to cancel

a SEPA payment and

ask the recipient’s bank

to return the money if

you’ve made duplicate

payments by mistake,

there has been a

technical fault or

someone else has

fraudulently made the

payment from your

account. You must ask

us to cancel the

payment within 10

working days of the

payment date but there

is no guarantee that the

recipient’s bank will

return the payment.

18

Important information about the

payment service:

Terms and Conditions

1. These conditions will apply when you post your ‘Request to Close Account(s)’ form

(SF220) to us. They apply in addition to the terms and conditions which applied to

the account before it was closed, and they take priority if they are different to those

account terms and conditions.

2. You need to complete the ‘Request to Close Account(s)’ form and post it back to us

following instructions set out in the form.

3. W

e may call you about your request – your agreement given during the phone call

is your consent for us to make the payment in accordance with the ‘Request to

Clo

se Account(s)’ form, the details set out in the table above and these conditions.

4.

In order to process your payment instruction, we need a correctly completed

‘Request to Close Account(s)’ form, for the account the funds are to be paid to. We

will confirm your name and address to make sure we are meeting our obligations

under UK Money Laundering Regulations. If any information on the form is missing,

incomplete or we require further information or documentation (such as D), we’ll

reject the instruction and let you know using any of the contact details we have for

you. If this happens, you may need to complete a new ‘Request to Close Account(s)’

form and resubmit it along with the required evidence.

5.

For SWFT or SEPA payments in a foreign currency, we will convert your payment into

your chosen currency using our standard outbound exchange rate which applies at

the time we process the payment. We will tell you what that is when we call you to

confirm a few details about the payment instruction. Details of our standard

outbound exchange rates can be found at nationwide.co.uk/exchangerates

6.

After your payment is processed, we’ll send you written communication confirming

details of the transaction.

7.

These terms and conditions are governed by English law and the language we use

in them and in our communications with you is English. If you want to bring a claim

against us in the courts, you can do so in the courts of England and Wales or in the

courts which are local to where you live.

8.

We won’t be liable if things go wrong as a result of things beyond our control, such

as abnormal or unforeseeable circumstances, the consequences of which we could

not have avoided, or where they have resulted from us having to comply with law.

9. If the account is being closed to make the payment, the closing balance will include

any interest earned on the account since the last interest payment was made. This

me

ans that the closing balance may be different to the current balance held in the

account.

19

Your checklist

We’ve put together a checklist of people and organisations you may need to contact.

When you do, it’s worth having to hand the following information about the person

who has died:

•

their National Insurance number

•

their NHS number

•

their date and place of birth

•

their date of marriage or civil partnership (if applicable)

•

their tax reference number (if applicable)

•

their passport and driving licence number (if applicable).

It’s also a good idea to have their personal representatives’ names and addresses.

Don’t forget the government’s

Tell Us Once service

If you can use it, it’s such a handy service.

It covers:

•

HMRC

•

your local council

•

the Department for Work and Pensions

•

the Passport Office.

•

the DVLA

Fraud awareness

We’re committed to helping our members protect themselves against fraud.

For more information on fraud awareness you can contact us on 0800 464 3018

or visit nationwide.co.uk/support/securitycentre/fraudawareness/cardfraud

20

What you need to do: your checklist

Please treat this as a guide as it won’t be right for everyone.

Legal things to do Complete

Obtain a medical certificate from the hospital/doctor

Register the death, find out more on gov.uk/registeradeath

Obtain copies of the certified death certificate

If there is a will, check if there are any specific requests

(for example, to do with their funeral)

Contact funeral director

Notify solicitors/accountant

Notify the executors named in the will or appoint an administrator

Government organisations to contact if you’re not using the

Tell Us Once service

Complete

HM Revenue & Customs (HMRC) to deal with tax and cancel

benefits

Department for Work and Pensions (DWP) to cancel any benefits

such as Income Support

HM Passport Office (HMPO) to cancel a passport

Driver and Vehicle Licensing Agency (DVLA) to cancel a driving

licence (you will need to send the registration certificate V5C)

The local council, to cancel housing benefit, council tax benefit,

a Blue Badge, inform council housing services and remove the

person from the electoral register

Housing: who to contact Complete

Their mortgage provider, landlord or local authority

Royal Mail to arrange a redirection service

Utility companies such as phone, water, gas, electric

Any private organisation or agency providing home help

TV or internet companies

21

Financial things to sort out

Complete

Bank or building society accounts and National Savings

Direct Debits and standing orders

Check bank statements for regular payment credits and contact

those firms to stop the receipt of payments into the account

Credit cards and store cards

Subscriptions to clubs, groups or magazines

Recurring VSA payments, for example Netflix

Insurance policies such as house, car, travel, medical. If the person

who has died was named first on an insurance policy, make contact

as early as possible to ensure you’re still insured

Pensions providers and life insurance companies

Mobile phone contracts

Companies with which they may have had

rental, hire purchase or loan agreements

Other organisations and people to contact

Complete

Clubs, trade unions or associations to cancel their membership

and possibly secure a refund

Their doctor or hospital to cancel any appointments

Their dentist and optician

Their church or regular place of worship

22

Useful websites

Help and Bereavement Support

•

Cruse Bereavement Care – cruse.org.uk

Help with understanding and coping with grief following the death of someone close.

•

The Samaritans – samaritans.org

A completely confidential service offering support for any type of emotional distress.

•

Child Bereavement UK – childbereavementuk.org

Information, training and specialised support for when a child dies or a child is

bereaved.

•

Age UK – ageuk.org.uk

Free help and advice from the UK’s largest charity dedicated to helping people make

the most of later life.

•

Widowed and Young

Support group for young widowed men and women across the UK, married or not,

with children or without.

Tel: 0300 012 4929

Web: widowedandyoung.org.uk

Funeral services

•

National Association of Funeral Directors – nafd.org.uk

Help with finding a registered funeral director in your area.

•

The British Humanist Association – humanism.org.uk/ceremonies

Help with arranging nonreligious funerals and ceremonies.

•

The Natural Death Centre – naturaldeath.org.uk

A charity offering support and guidance when planning a funeral.

Financial and legal advice

•

The Probate Service – theprobateservice.org

Guidance for dealing with probate and inheritance tax.

•

Citizens Advice Bureau – citizensadvice.org.uk

Free legal advice and support.

•

HM Revenue & Customs

Pay As You Earn and Self Assesment

HM Revenue and Customs, BX9 1AS, United Kingdom

Tel: 0300 200 3300

or visit www.hmrc.gov.uk

•

The General Register Office

PO Box 2, Southport PR82 2JD

Email: [email protected].uk

23

Contact us

In branch

Book an appointment to speak to one of the team at your local branch. You can pop in to

make an appointment or if you’d rather do it over the phone, you can find your branch’s

phone number at nationwide.co.uk/branchfinder

By post

You can write to us at:

Bereavement Services

Specialist Customer Support

Nationwide Building Society

Swindon

Wiltshire

SN38 3FN

By phone

Call our bereavement team on:

0800 464 30 18

Lines are open:

Mon to Fri 9am to 5pm, Sat 9am to 12pm

Specialist Support Services

Our team have received specialist training to provide a confidential service for

customers affected by illness or an unexpected change in their personal circumstances.

Find out more at nationwide.co.uk/help/challengingtimes

P3162 (April 2024)

Ask in branch

Call 0800 464 30 18

Visit the Help & Support pages of our website

Nationwide Building Society. Head Office: Nationwide House, Pipers Way, Swindon, Wiltshire SN38 1NW.

You can receive this document and others like it, in Braille, large

print or on audio CD.

Just call 03457 30 20 11 or visit your local branch if you’d like us

to arrange this for you.

If you have hearing or speech difficulties:

•

You can use Text Relay if you have a textphone. Dial 18001,

followed by the phone number you want to ring

•

SignVideo is also available if you’re deaf and use British Sign

Language. Just visit Signvideo.co.uk

To find out about other

ways we may be able to help, search

‘accessibility tools’ on nationwide.co.uk

C003270C003270