2Q 2023 Preliminary Results

1

Ally Financial Inc.

2Q 2023 Earnings Review

July 19, 2023

Contact Ally Investor Relations at (866) 710-4623 or [email protected]

2Q 2023 Preliminary Results

2

Forward-Looking Statements and Additional Information

This presentation and related communications should be read in conjunction with the financial statements, notes, and other information contained in our Annual Reports on Form 10-K,

Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K. This information is preliminary and based on company and third-party data available at the time of the presentation or

related communication.

This presentation and related communications contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements can be

identified by the fact that they do not relate strictly to historical or current facts—such as statements about the outlook for financial and operating metrics and performance and future

capital allocation and actions. Forward-looking statements often use words such as “believe,” “expect,” “anticipate,” “intend,” “pursue,” “seek,” “continue,” “estimate,” “project,” “outlook,”

“forecast,” “potential,” “target,” “objective,” “trend,” “plan,” “goal,” “initiative,” “priorities,” or other words of comparable meaning or future-tense or conditional verbs such as “may,” “will,”

“should,” “would,” or “could.” Forward-looking statements convey our expectations, intentions, or forecasts about future events, circumstances, or results. All forward-looking statements,

by their nature, are subject to assumptions, risks, and uncertainties, which may change over time and many of which are beyond our control. You should not rely on any forward-looking

statement as a prediction or guarantee about the future. Actual future objectives, strategies, plans, prospects, performance, conditions, or results may differ materially from those set forth

in any forward-looking statement. Some of the factors that may cause actual results or other future events or circumstances to differ from those in forward-looking statements are

described in our Annual Report on Form 10-K for the year ended December 31, 2022, our subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K, or other

applicable documents that are filed or furnished with the U.S. Securities and Exchange Commission (collectively, our “SEC filings”). Any forward-looking statement made by us or on our

behalf speaks only as of the date that it was made. We do not undertake to update any forward-looking statement to reflect the impact of events, circumstances, or results that arise after

the date that the statement was made, except as required by applicable securities laws. You, however, should consult further disclosures (including disclosures of a forward-looking

nature) that we may make in any subsequent SEC filings.

This presentation and related communications contain specifically identified non-GAAP financial measures, which supplement the results that are reported according to U.S. generally

accepted accounting principles (“GAAP”). These non-GAAP financial measures may be useful to investors but should not be viewed in isolation from, or as a substitute for, GAAP results.

Differences between non-GAAP financial measures and comparable GAAP financial measures are reconciled in the presentation.

Unless the context otherwise requires, the following definitions apply. The term “loans” means the following consumer and commercial products associated with our direct and indirect

financing activities: loans, retail installment sales contracts, lines of credit, and other financing products excluding operating leases. The term “operating leases” means consumer- and

commercial-vehicle lease agreements where Ally is the lessor and the lessee is generally not obligated to acquire ownership of the vehicle at lease-end or compensate Ally for the

vehicle’s residual value. The terms “lend,” “finance,” and “originate” mean our direct extension or origination of loans, our purchase or acquisition of loans, or our purchase of operating

leases, as applicable. The term “consumer” means all consumer products associated with our loan and operating-lease activities and all commercial retail installment sales contracts. The

term “commercial” means all commercial products associated with our loan activities, other than commercial retail installment sales contracts. The term “partnerships” means business

arrangements rather than partnerships as defined by law.

2Q 2023 Preliminary Results

3

($ millions, except per share data)

(1) The following are non-GAAP financial measures which Ally believes are important to the reader of the Consolidated Financial Statements, but which are supplemental to and not a substitute for GAAP measures: Accelerated

issuance expense (Accelerated OID), Adjusted earnings per share (Adjusted EPS), Adjusted efficiency ratio, Adjusted noninterest expense, Adjusted other revenue, Adjusted tangible book value per share (Adjusted TBVPS),

Adjusted total net revenue, Core net income attributable to common shareholders, Core original issue discount (Core OID) amortization expense, Core outstanding original issue discount balance (Core OID balance), Core pre-

provision net revenue (Core PPNR), Core pre-tax income, Core return on tangible common equity (Core ROTCE), Investment income and other (adjusted), Net financing revenue (excluding Core OID), Net interest margin (excluding

Core OID), Pre-provision net revenue (PPNR), and Tangible Common Equity. These measures are used by management, and we believe are useful to investors in assessing the company’s operating performance and capital.

Refer to the Definitions of Non-GAAP Financial Measures and Other Key Terms, and Reconciliation to GAAP later in this document.

(2) Non-GAAP financial measure – see pages 34 – 36 for definitions.

GAAP and Core Results: Quarterly

2Q 23 1Q 23 4Q 22 3Q 22 2Q 22

GAAP net income attributable to common shareholders (NIAC) 301$ 291$ 251$ 272$ 454$

Core net income attributable to common shareholders

(1)(2)

291$ 250$ 327$ 346$ 570$

GAAP earnings per common share (EPS) (diluted, NIAC) 0.99$ 0.96$ 0.83$ 0.88$ 1.40$

Adjusted EPS

(1)(2)

0.96$ 0.82$ 1.08$ 1.12$ 1.76$

Return on GAAP common shareholders' equity 10.8% 10.8% 9.7% 10.0% 14.7%

Core ROTCE

(1)(2)

13.9% 12.5% 17.6% 17.2% 23.2%

GAAP common shareholders' equity per share 37.16$ 36.75$ 35.20$ 33.66$ 37.28$

Adjusted tangible book value per share (Adjusted TBVPS)

(1)(2)

32.08$ 31.59$ 29.96$ 28.39$ 32.16$

Efficiency ratio 60.1% 60.3% 57.5% 57.6% 54.8%

Adjusted efficiency ratio

(1)(2)

51.7% 55.8% 50.6% 48.2% 43.9%

GAAP total net revenue 2,079$ 2,100$ 2,201$ 2,016$ 2,076$

Adjusted total net revenue

(1)(2)

2,066$ 2,047$ 2,163$ 2,089$ 2,222$

Pre-provision net revenue

(1)(2)

830$ 834$ 935$ 855$ 938$

Core pre-provision net revenue

(1)(2)

817$ 781$ 954$ 948$ 1,084$

Effective tax rate 18.4% 17.5% 37.5% 28.1% 24.0%

2Q 2023 Preliminary Results

4

• Maintaining strong levels of liquidity and capital in a dynamic environment

• Retail deposit balances ↑$0.5 billion QoQ; FDIC insured balances ↑$1.3 billion QoQ and represent 92% portfolio

• Total available liquidity of $42.5 billion, 3.8x uninsured deposit balance

• 9.3% CET1 ratio, $3.7 billion of capital above regulatory minimum and SCB

$0.99 | $0.96

GAAP

EPS

Adj.

EPS

3.4% | 10.4%

NIM

(ex. OID)

Est. Retail

Originated Yield

Operational Highlights

2Q 2023 Highlights

10.8% | 13.9%

Funding, Liquidity & Capital

• 3.5 million consumer auto applications driving $10.4 billion of origination volume

• Annualized retail auto net charge-offs of 132bps

• Insurance written premiums of $299 million

(1) Non-GAAP financial measure. See pages 34 – 36 for definitions.

(2) Estimated Retail Auto Originated Yield is a forward-looking financial measure. See page 37 for details.

(3) Consumer and Commercial Banking activity is within ‘Corporate and Other’ and ‘Corporate Finance’ businesses.

Note: Ally Bank, Member FDIC and Equal Housing Lender, which offers mortgage lending, point-of-sale personal lending, and a variety of deposit and other banking products, a consumer credit card business, a

corporate finance business for equity sponsors and middle-market companies. Additionally, we offer securities-brokerage and investment advisory services through Ally Invest.

Return on

Common Equity

Core

ROTCE

$2.1B | $2.1B

GAAP

Net Revenue

Adj. Total

Net Revenue

(1) (1)

(1)

(1)

(2)

Dealer

Financial

Services

Consumer &

Commercial

Banking

• $154.3 billion of total deposits, up $13.9 billion YoY; 2.9 million customers

• Over 1 million active credit cardholders; One Ally digital experience launched; full rebranding expected in 2023

• Corporate finance floating rate HFI loans of $10.1 billion with ~100% in first lien position

(3)

2Q 2023 Preliminary Results

5

Strong enterprise engagement

score of 84, ranking in the top

10% of companies, +8 vs.

financial services benchmark

(1)

Announced nearly $1B in giving and

capital deployment in 2023 to support

affordable housing initiatives

Purpose-Driven Culture

Treat customers

equally with honesty

and integrity

Make an impact in the

communities in which

we live and work

Powered by our “LEAD” core values and “Do it Right” approach

Invest in our people

and culture to drive

purpose

Customers

Employees

Communities

L

E

A

D

Look

externally

Execute with

excellence

Act with

professionalism

Deliver

results

Delivering long-term value for all stakeholders

See page 38 for footnotes.

170M+ digital interactions

(2)

and

4M+ customer calls supported YTD,

87% Bank customer satisfaction

(3)

,

96% customer retention

(4)

2Q 2023 Preliminary Results

6

- Expect near-term NIM compression from higher Fed Funds rate path

- Well-established hedging program positioned for ‘higher-for-longer’ rate scenario

- Positioned for NIM expansion, driven by asset-yield momentum, after short-term rate increases pause

Managing a Dynamic Environment

Interest Rates

Retail Auto Credit Performance

Potential Regulatory Changes

Balancing Near-term Headwinds with Long-term Focus

- Expect full-year retail auto NCOs of 1.8% (upper-end of range)

- Continuing to monitor impacts of inflation and elevated delinquencies

- Anticipate used vehicle values down 12% in the second half of 2023 (down 8% on a full-year basis)

- Balance sheet positioned for margin and earnings expansion as near-term headwinds abate

- Expect full-year retail auto originated yields >10.5%, driving significant earning asset-yield expansion

- High-quality, consumer deposit portfolio representing 87% of funding; stable and efficient foundation

- Maintaining strong capital and liquidity buffers informed by comprehensive scenario analysis

- Preparing for ↑ overall capital and liquidity and more stringent requirements for Category IV firms

Positioned for long-term earnings expansion despite volatile market backdrop

2Q 2023 Preliminary Results

7

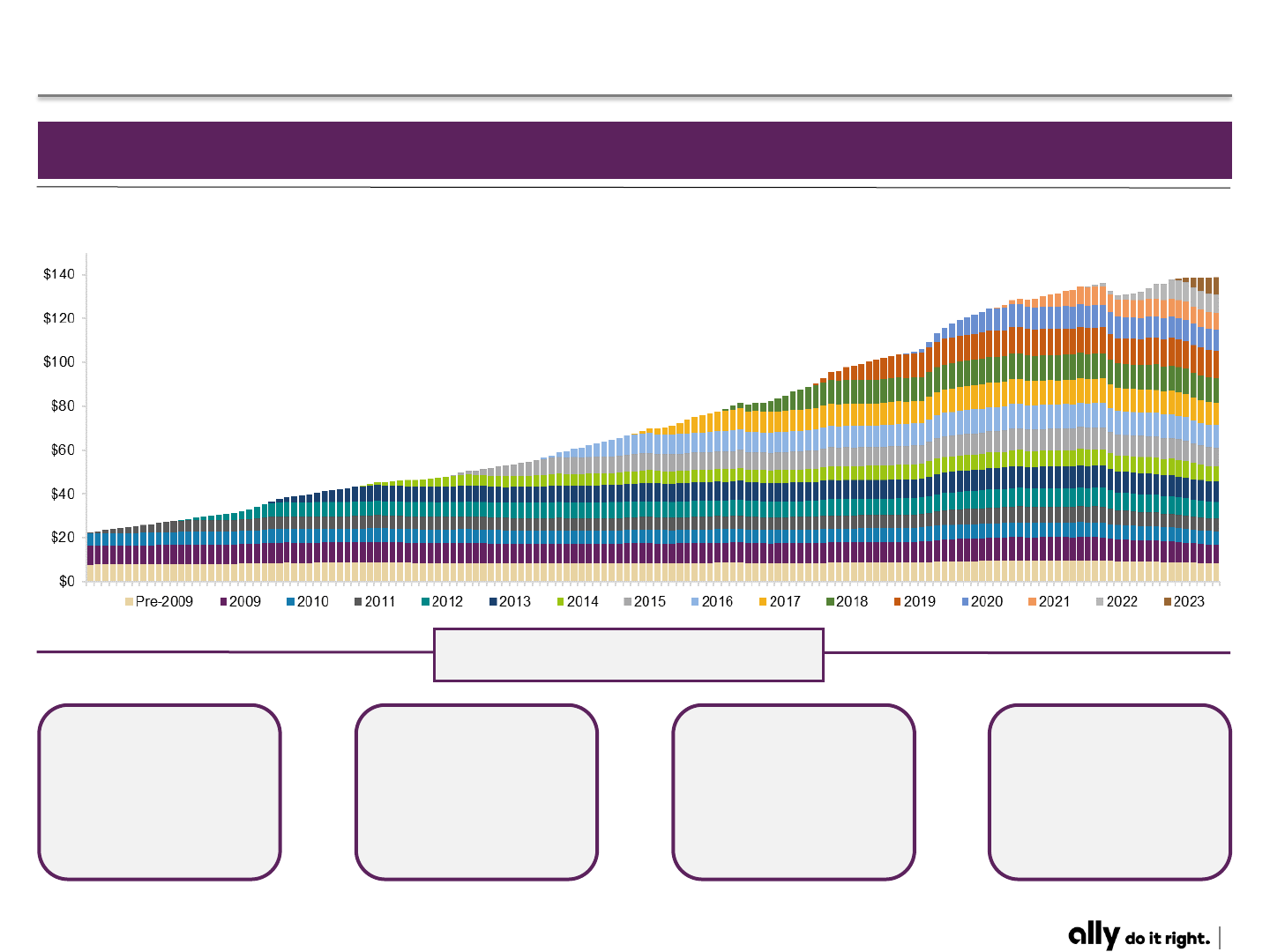

Diversified Consumer Deposits Franchise

96%

Customer

retention

(1)

92%

of retail deposit

balances are

FDIC insured

~$50k

Avg. customer

deposit balance

Ally Retail Deposits by Vintage

2.9M

Retail deposit

customers

Highlights

Stable and growing deposit vintages since the inception of Ally Bank

($ billions)

See page 37 for footnotes.

2Q 2023 Preliminary Results

8

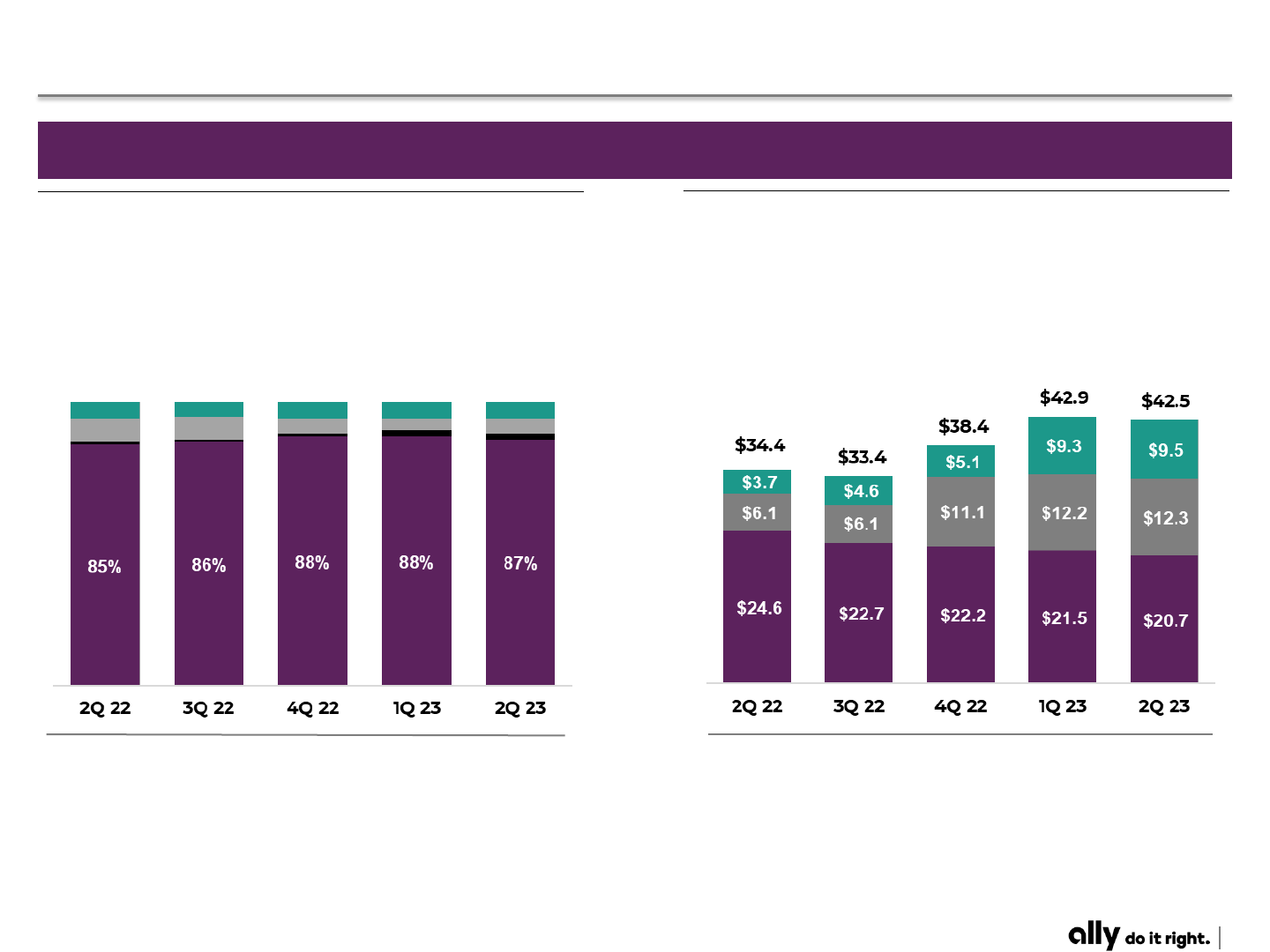

Funding Composition

Funding and Liquidity

Total Available Liquidity

Stable, high-quality deposit funding and strong liquidity position

Available Liquidity vs. Uninsured Deposits

2.3x 2.2x 2.5x 3.6x

Loan to Deposit Ratio

(1)

100% 99% 96% 95% 96%

Unencumbered Highly Liquid Securities

Cash and Equivalents

FHLB Unused Pledged Borrowing Capacity

Total Deposits

Unsecured Debt

FHLB / Other

Secured Debt

Note: Excludes (i) estimated incremental funding capacity if securities were pledged to Bank Term Funding Program at

par relative to market value (~$1.8B) and (ii) Fed Discount Window based on pledged collateral ($2.1B) as of 6/30/23.

($ billions)

3.8x

(1) Total loans and leases.

2Q 2023 Preliminary Results

9

2Q 2023 Financial Results

(1) Non-GAAP financial measure. See pages 34 – 36 for definitions.

(2) Contains non-GAAP financial measures and other financial measures. See pages 34 – 37 for definitions.

($ millions, except per share data)

Increase / (Decrease) vs.

Consolidated Income Statement

2Q 23

1Q 23 2Q 22 1Q 23 2Q 22

Net financing revenue 1,573$ 1,602$ 1,764$ (29)$ (191)$

Core OID

(1)

12 11 10 0 2

Net financing revenue (ex. Core OID)

(1)

1,585 1,613 1,774 (29) (189)

Other revenue 506 498 312 8 194

Repositioning and change in fair value of equity securities

(2)

(25) (65) 136 40 (161)

Adjusted other revenue

(1)

481 433 448 48 33

Provision for credit losses 427 446 304 (19) 123

Memo: Net charge-offs 399 409 153 (10) 246

Memo: Provision build / (release) 28 37 151 (9) (123)

Noninterest expense 1,249 1,266 1,138 (17) 111

Pre-tax income 403$ 388$ 634$ 15$ (231)$

Income tax expense 74 68 152 6 (78)

Net loss from discontinued operations - (1) - 1 -

Net income 329$ 319$ 482$ 10$ (153)$

Preferred stock dividends 28 28 28 - -

Net income attributable to common stockholders 301$ 291$ 454$ 10$ (153)$

GAAP EPS (diluted) 0.99$ 0.96$ 1.40$ 0.03$ (0.41)$

Core OID, net of tax

(1)

0.03 0.03 0.02 0.00 0.01

Change in fair value of equity securities, net of tax

(2)

(0.06) (0.17) 0.33 0.10 (0.40)

Repositioning, discontinued ops., and other, net of tax

(2)

- 0.00 - (0.00) -

Adjusted EPS

(1)

0.96$ 0.82$ 1.76$ 0.13$ (0.80)$

2Q 2023 Preliminary Results

10

(1) Mortgage includes held-for-investment (HFI) loans from the Mortgage Finance segment and the HFI legacy mortgage portfolio in run-off at the Corporate and Other segment.

(2) Unsecured lending from point-of-sale financing.

(3) Includes Community Reinvestment Act and other held-for-sale (HFS) loans.

(4) Includes retail, brokered, and other deposits (inclusive of sweep deposits, mortgage escrow and other deposits).

(5) Includes FHLB borrowings and Repurchase Agreements.

(6) Non-GAAP financial measure. See pages 34 – 36 for definitions.

($ millions)

(3)

Balance Sheet and Net Interest Margin

Average

Balance

Yield

Average

Balance

Yield

Average

Balance

Yield

Retail Auto Loans 84,097$ 8.81% 83,615$ 8.49% 79,695$ 6.82%

Auto Leases (net of depreciation) 10,110 7.60% 10,435 6.84% 10,615 6.66%

Commercial Auto 19,709 6.94% 18,650 6.60% 16,211 3.65%

Corporate Finance 10,240 9.15% 10,606 8.96% 8,351 5.02%

Mortgage

(1)

19,325 3.22% 19,621 3.25% 18,980 3.01%

Consumer Other - Ally Lending

(2)

2,114 9.99% 2,037 9.97% 1,346 11.94%

Consumer Other - Ally Credit Card 1,701 21.88% 1,618 21.84% 1,093 19.71%

Cash and Cash Equivalents 7,401 4.70% 5,731 3.95% 3,761 0.61%

Investment Securities & Other

(3)

31,958 3.17% 32,578 3.04% 35,050 2.35%

Earning Assets 186,655$ 6.99% 184,891$ 6.71% 175,103$ 5.11%

Total Loans and Leases 147,717 7.93% 146,992 7.63% 136,663 5.93%

Deposits

(4)

152,382$ 3.74% 152,752$ 3.23% 139,814$ 0.76%

Unsecured Debt 10,618 6.27% 10,357 6.20% 8,806 6.02%

Secured Debt 2,879 5.61% 2,552 6.04% 1,154 6.61%

Other Borrowings

(5)

7,592 3.00% 6,503 2.74% 11,966 1.75%

Funding Sources 173,471$ 3.89% 172,165$ 3.44% 161,740$ 1.16%

NIM (as reported) 3.38% 3.51% 4.04%

Core OID

(6)

824$ 5.77% 835$ 5.56% 868$ 4.72%

NIM (ex. Core OID)

(6)

3.41% 3.54% 4.06%

1Q 23

2Q 22

2Q 23

2Q 2023 Preliminary Results

11

• Net interest margin trough in 4Q assuming Fed Funds peak of 5.50% in 2Q ‘23 with no easing in 2023

– End of 2023 Fed Funds ↑ 100bps vs. 3/31 curve, putting incremental pressure on NIM trough

• Net interest margin expansion driven by earning asset yield momentum after rate increases pause

– Margin expansion will accelerate when benchmark rates decline

• Retail auto portfolio yield expected to reach 9% in 4Q ‘23

– Recent originated yields >10% replacing older vintages over medium-term, driving portfolio yield >9% in 2024

Retail Auto Pricing Dynamics

Deposit Pricing Dynamics

Estimated

Originated

Yield

(1)

Portfolio

Yield

EoP OSA

Yield

Retail

Deposit

Portfolio

Yield

Expect 2023 full-year average NIM of approximately 3.4%

(1) Estimated Retail Auto Originated Yield is a forward-looking financial measure. See page 37 for details.

Net Interest Margin Dynamics

Earning Asset Yield:

5.1% 5.6% 6.2% 6.7% 7.0% ~7.2%

Assumes peak

Fed Funds of 5.50%

and no rate cuts

QoQ Yield ↓ driven by shift

to higher credit quality mix

2Q 2023 Preliminary Results

12

Note: For more details on the final rules to address the impact of CECL on regulatory capital by allowing BHCs

and banks, including Ally, to delay and subsequently phase-in its impact, see page 37.

Note: Repurchased common shares include shares withheld to cover income taxes owed by participants related to share-based incentive plans. 301,618,768 actual shares outstanding as of 6/30/23.

Capital Ratios and Risk-Weighted Assets

2Q ‘23 CET1 and TCE Ratios

Capital Deployment Actions

Total Capital

Ratio

Tier 1 Ratio

CET1 Ratio

Risk

Weighted

Assets

• 2Q ‘23 CET1 ratio of 9.3%

• $3.7B of CET1 capital above FRB requirement of 7.0%

(Regulatory Minimum + SCB)

– 9.0% internal operating target

– Preliminary 2023 SCB unchanged at 2.5%

• Balanced approach in a dynamic environment

– Modest RWA growth while increasing capital buffer

• Ongoing scenario analysis and planning informs actions

• Announced 3Q ’23 common dividend of $0.30 per share

Capital

($ billions)

6.9%

Pro-forma CET1 in unlikely

event of immediate, full

phase-in of AFS AOCI

Common Shares Outstanding

Dividend per Share

484M

452M

426M

393M

374M

363M

313M

302M

2Q 16

4Q 16

2Q 17

4Q 17

2Q 18

4Q 18

2Q 19

4Q 19

2Q 20

4Q 20

2Q 21

4Q 21

2Q 22

4Q 22

2Q 23

$-

$0.08

$0.13

$0.17

$0.19

$0.30

2Q 16

4Q 16

2Q 17

4Q 17

2Q 18

4Q 18

2Q 19

4Q 19

2Q 20

4Q 20

2Q 21

4Q 21

2Q 22

4Q 22

2Q 23

(1)

(1) Contains a Non-GAAP financial measure. See pages 34 – 36 for definitions.

2Q 2023 Preliminary Results

13

Consolidated Net Charge-Offs (NCOs)

Note: Ratios exclude loans measured at fair value and loans held-for-sale. See page 37 for definition.

Notes: [1] Includes accruing contracts only [2] Days Past Due (“DPD”).

(1) Corp/Other includes legacy Mortgage HFI portfolio.

See page 37 for definition.

Retail Auto Net Charge-Offs (NCOs)

Retail Auto Delinquencies

Net Charge-Off Activity

($ millions)

Annualized

NCO Rate

60+

Delinquent

Contracts ($M)

60+ DPD

Delinquency

Rate

NCOs ($M)

Annualized

NCO Rate

30+ DPD

Delinquency

Rate

NCOs ($M)

Asset Quality: Key Metrics

2Q 22 3Q 22 4Q 22 1Q 23 2Q 23

Retail Auto 108$ 217$ 347$ 351$ 277$

Commercial Auto (1) - - - 4

Mortgage Finance (1) 1 - - -

Corporate Finance 26 31 - - 56

Ally Lending 13 16 26 30 27

Ally Credit Card 11 13 19 29 36

Corp/Other

(1)

(3) (2) (2) (1) (1)

Total 153$ 276$ 390$ 409$ 399$

QoQ decrease driven by seasonality

YoY increase reflects industry-wide credit normalization

2Q 2023 Preliminary Results

14

($ millions)

Note: Coverage rate calculations exclude fair value adjustment for loans in hedge accounting relationships. Note: Coverage rate calculations exclude fair value adjustment for loans in hedge accounting relationships.

Consolidated Coverage Retail Auto Coverage

Consolidated QoQ Reserve Walk

($ billions) ($ billions)

Net Charge-

off Activity

1

1Q ’23

Reserve

$3,751 $3,781

$(25)

($399) 2Q ’23 NCOs

2Q ’23

Reserve

Loan Growth

Includes macroeconomic

trends

$399 Replenished

$55

∆ In Portfolio

Size

2

All

Other

3

Reserve (%)

Reserve ($)

Reserve (%)

Reserve ($)

Asset Quality: Coverage and Reserves

2Q 2023 Preliminary Results

15

Restrictive measures on underperforming segments, including

auto decline and actions driving ↑ mix of new vehicles

Identified six underperforming microsegments; moved to auto

decline or adjusted pricing and loss assumptions

Risk premium pricing increments to lower credit tiers and

curtailment actions on lower performing segments

Retail Auto Credit Performance

Loss performance down seasonally in 2Q, pace of 30+ day DQ normalization moderating

• 2Q ‘23 NCOs of 1.3% slightly elevated versus expectations

– Elevated delinquencies entering the quarter translated to higher losses in late June

– Losses coincided with accelerated decline in used values observed late in the quarter

• 30+ day delinquencies remain elevated, but moved more in-line with expectations QoQ

– Smallest 2Q QoQ increase in 30+ day delinquencies since 2020; lowest YoY increase since 1Q ‘22

– Continuing to monitor impact of elevated delinquency and persistent inflation on loss frequency

– Severity mainly driven by used vehicle values, which are projected to decline 12% in second half of the year

2023 Retail Auto NCO Trajectory Summary of Pricing and Underwriting Actions

Seasonal NCO trajectory for full-year annualized NCO rate of ~1.8%

4Q ‘22

1Q ‘23

2Q ‘23

1H ‘22

3Q ‘22

Add’l price changes driving ↑ S-tier mix in 2Q ‘23, and additional

actions on lower performing segments

Add’l price changes resulting in ↑ originated yield going forward

See page 37 for definition.

2Q 2023 Preliminary Results

16

• 2023 used vehicle value forecast largely unchanged since 1Q ‘23 (full-year down 8% vs. 9% previously)

• Expect continued decline in used vehicle values for remainder of the year (down 12% vs. June)

• Continue to expect used values to remain elevated vs. 2019 throughout medium term

– Ongoing lack of used vehicle supply expected to keep auction prices above pre-pandemic levels well beyond 2023

Used vehicle values forecast to decline 12% in 2H ’23

Used Vehicle Value Outlook

Ally Used Vehicle Value Index

3-year-old vehicles, adjusted for seasonality, mix, mileage, and MSRP inflation

↓ 3% QoQ

↑ 5% YTD

↓ 8 %

FY’23

↓ 12%

2Q 2023 Preliminary Results

17

Ally Bank: Multi-product Relationship Customers

Note: Brokered / Other includes sweep deposits, mortgage escrow and other deposits.

Net New Retail Deposit Customers

($ billions; EoP)

Avg. Retail

Portfolio

Interest Rate

FDIC

Insured

Uninsured

• Total deposits of $154.3 billion, up $13.9 billion YoY

– Retail deposits of $139.0 billion, up $7.8 billion YoY

and $486 million QoQ

• 2.9 million retail deposit customers, up 14% YoY

– 86 thousand net new customers in 2Q

– 69% of new customers from millennial or younger generations

– Industry leading 96% customer retention rate

• 10% multi-product relationship customers

Deposit customers with an Ally Invest, Ally Home or Ally Credit Card relationship

14+

Consecutive Years of

Retail Deposit Growth

57

Consecutive Quarters

of Customer Growth

Largest All-Digital,

Direct U.S. Bank

(1)

#

1

$

139B

Retail Deposit

Balances

2.9M

Ally Bank

Deposit Customers

Total Deposits: Retail & Brokered

See page 38 or footnotes.

Note: Ally Bank, Member FDIC and Equal Housing Lender, which offers mortgage lending, point-of-sale personal lending, and a variety of deposit and other banking products, a consumer credit card

business, a corporate finance business for equity sponsors and middle-market companies. Additionally, we offer securities-brokerage and investment advisory services through Ally Invest.

Ally Bank: Deposit and Customer Trends

Brokered /

Other

2Q 2023 Preliminary Results

18

Ally Invest (Brokerage & Wealth)

Ally Credit Card

Ally Lending (Point of Sale)

EoP Portfolio Balances ($ in billions) | 56% Customer CAGR since 2017

Acquired: 4Q’21

EoP Portfolio Balances ($ in billions) | 3.3k merchant relationships

Acquired: 4Q’19

• Leading, all-digital direct bank with complementary

product suite

– 85% of new Ally Invest accounts from existing customers

– 1.1 million active cardholders, up 49 thousand QoQ and

$1.8 billion in outstanding balances

– 480 thousand point of sale customers from over 3 thousand

merchant locations primarily in high-quality home improvement

and healthcare verticals

• Modest growth in unsecured balances year-to-date,

reflective of cautious approach in current environment

Net Customer Assets ($ in billions) | Acquired: 2Q’16

% of New

Accts from

Existing

Customers

Organic growth opportunities to deepen customer relationships

Ally Bank: Leading, Growing, and Diversified

Note: Ally Bank, Member FDIC and Equal Housing Lender, which offers mortgage lending, point-of-sale personal lending, and a variety of deposit and other banking products, a consumer credit card

business, a corporate finance business for equity sponsors and middle-market companies. Additionally, we offer securities-brokerage and investment advisory services through Ally Invest.

2Q 2023 Preliminary Results

19

• Auto pre-tax income of $501 million

– Pre-tax income down YoY, primarily driven by lower net loss

performance in prior year period

• Unique dealer value proposition, combined with pullback

from peers, has allowed for strategic pricing and

underwriting actions

– Opportunity to increase originations in highest credit quality

segment to optimize risk-adjusted returns

• Higher off-lease volume and per-unit auction proceeds

driving increased lease remarketing gains QoQ

See page 38 for footnotes.

Lease Portfolio Trends

Lessee &

Dealer

Buyout %

Remarketing

Gains

($ millions)

Avg. Gain / Unit

$1,671 $1,325 $1,476 $1,932 $2,335

Auto Finance

S-Tier

A-Tier

B-Tier

C/D/E

Tier

Loss

Profile

Lower

Higher

Retail Auto Origination Mix by Credit Tier

Key Financials ($ millions) 2Q 23 1Q 23 2Q 22

Net financing revenue 1,349$ 27$ 48$

Total other revenue 83 6 11

Total net revenue 1,432 33 59

Provision for credit losses 331 (20) 103

Noninterest expense

(1)

600 (6) 55

Pre-tax income 501$ 59$ (99)$

U.S. auto earning assets (EOP) 115,397$ 1,834$ 6,581$

Key Statistics

Remarketing gains ($ millions) 70$ 23$ 20$

Average gain per vehicle 2,335$ 403$ 663$

Off-lease vehicles terminated (# units) 29,872 5,709 207

Application volume (# thousands) 3,517 199 221

Inc / (Dec) v.

2Q 2023 Preliminary Results

20

$36.4M

YTD

• Leveraging our strengths and partnership approach to continuously evolve with the industry

• Remarketing revenue, driven by SmartAuction, expected to be up over 60% in 2023 compared to 2019

– Revenue up materially despite 25%+ decline in industry wholesale volume

– White label relationships propelling growth with significant opportunity to expand even further over medium-term

• Passthrough programs enhance our value proposition to dealers, providing lending solutions without

increasing our credit exposure, while allowing for monetization of declined applications

– Ally receives fees for originating, selling and servicing declined applications that are passed through to partners

SmartAuction Units and Revenue

Passthrough Program Revenue

Units

Gross

Revenue

Significant revenue expansion enabled by scale of auto franchise

Auto Revenue Diversification

$62.4M

YTD

Lifetime pre-tax contribution

Industry Wholesale Volume

(1)

:

13.5M 11.9M 10.3M 8.9M 9.5M

↑ 60%+

↑ 400%+

(1) Estimated 2023 volume; source: Cox Automotive

2Q 2023 Preliminary Results

21

Consumer Electric Vehicles

• Unique scale and dealer engagement levels enable Ally to capitalize as EV adoption increases

• Consumer electric vehicle origination volume of $347 million in 2Q ‘23, up 42% YoY

– EV originations made up 3.4% of total consumer auto originations, up from 1.9% in 2Q ’22

• Portfolio balance of $1.5 billion, up 76% YoY, with diversification across products (lease, new and used)

– Consumer EV portfolio made up of plug-in hybrid (70%) and battery electric vehicles (30%)

• Insurance EV offerings provide additional opportunities to support dealers and customers

Well-positioned to remain an industry leader as consumer preferences evolve

Consumer EV Originations by Product

Consumer EV Portfolio Balance by Product

New

Retail

Used

Retail

Lease

New

Retail

Used

Retail

Lease

2Q 2023 Preliminary Results

22

Approval Rate

Consumer Originations Consumer Origination Mix

Auto Balance Sheet Trends

Consumer Applications and Approval Rate

See page 38 for footnotes.

#

1

Prime Auto

Lender

(1)

Leading

Insurance Provider

(F&I, P&C Products)

#

1

Bank Floorplan

Lender

(2)

Bank Retail Auto

Loan Outstandings

(3)

#

1

Dealer Satisfaction

J.D. Power Award

(4)

#

1

($ billions; % of $ originations) (% of $ originations)

($ billions; EoP, HFI only)

U.S.

Consumer

Applications

Retail

Commercial

Auto

Lease

Retail

Weighted Avg.

FICO

Growth

Stellantis

Nonprime %

of

Total Retail

Used

New

Lease

GM

Auto Finance: Agile Market Leader

2Q 2023 Preliminary Results

23

(1) Non-GAAP financial measure. See pages 34 – 36 for definitions.

For additional footnotes see page 38.

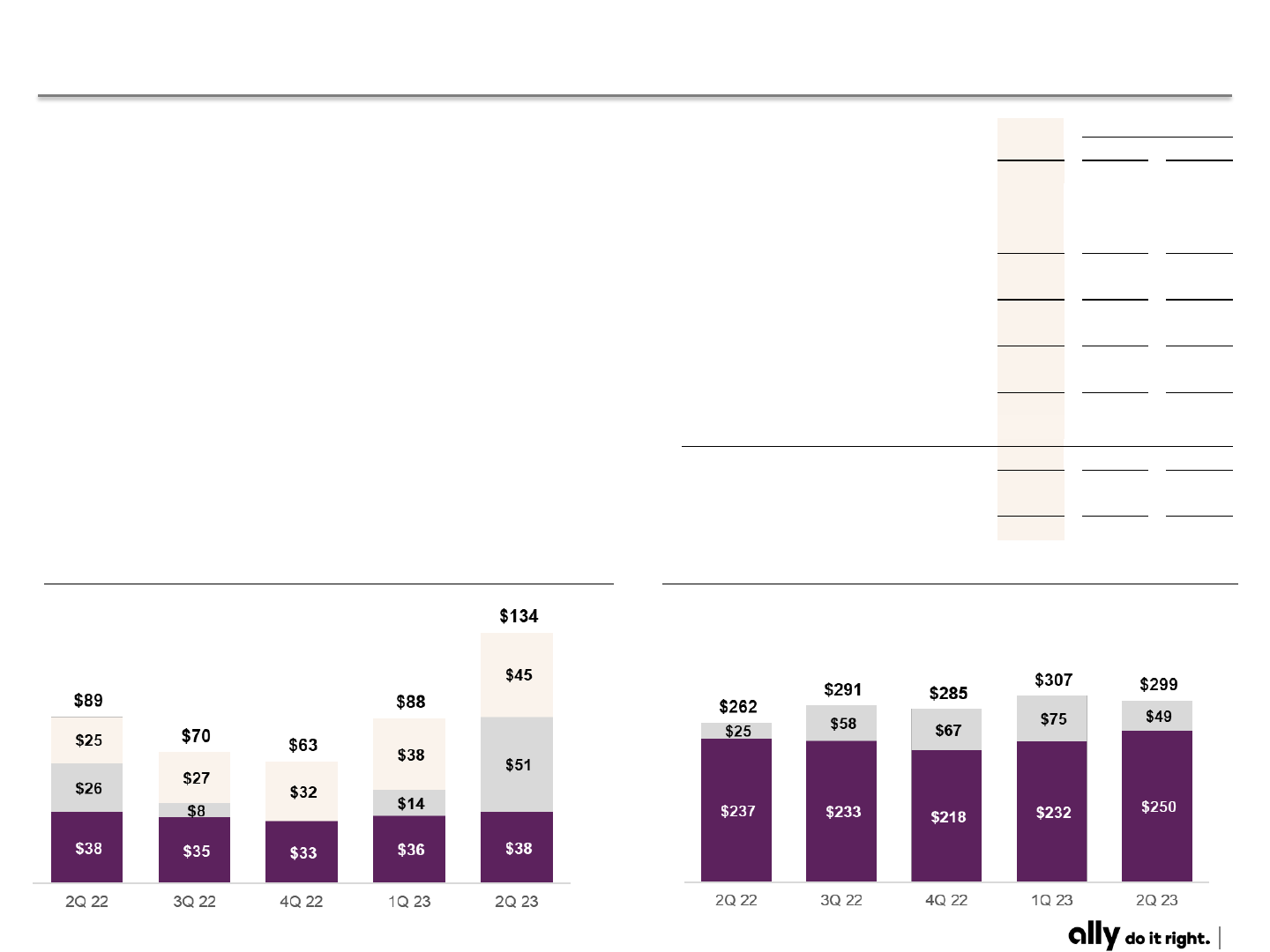

Insurance Written Premiums

Insurance Losses

Note: F&I: Finance and insurance products and other. P&C: Property and

casualty insurance products.

($ millions)

F&I

Premium

P&C

Premium

• Insurance pre-tax income of $8 million and core pre-tax

loss of $16 million

(1)

– $312 million of earned premiums, up $27 million YoY

– Other losses of $45 million, up $20 million YoY, driven by

normalization of GAP losses with lower used vehicle values and

growth in other ancillary products

– Investment income of $30 million, stable YoY and slightly down QoQ

• Severe hail activity across U.S. impacting vehicle inventory

weather losses

– Weather losses of $51 million, up $25 million YoY; June 2023

was highest single weather loss month since April 2020

• Written premiums of $299 million, up 14% YoY

– P&C premiums increasing from growing inventory and growth in

other dealer products

– F&I growth driven by product mix and higher volume in Canada

($ millions)

Weather

VSC

Other

Insurance

Key Financials ($ millions) 2Q 23 1Q 23 2Q 22

Premiums, service revenue earned and other income 312$ 3$ 27$

VSC losses 38 2 -

Weather losses 51 37 25

Other losses 45 7 20

Losses and loss adjustment expenses 134 46 45

Acquisition and underwriting expenses

(2)

224 (3) 13

Total underwriting income / (loss) (46) (40) (31)

Investment income and other 54 (44) 161

Pre-tax income 8$ (84)$ 130$

Change in fair value of equity securities

(3)

(24) 41 (160)

Core pre-tax loss

(1)

(16)$ (43)$ (30)$

Total assets (EOP) 8,890$ 23$ 71$

Key Statistics - Insurance Ratios 2Q 23 1Q 23 2Q 22

Loss ratio 43.0% 28.3% 31.2%

Underwriting expense ratio 71.5% 73.7% 74.8%

Combined ratio 114.5% 102.0% 106.0%

Inc / (Dec) v.

2Q 2023 Preliminary Results

24

• Corporate Finance pre-tax income of $72 million

– Net financing revenue up YoY reflecting higher average asset balances

• 2Q charge-off related to legacy healthcare cashflow exposure

– No P&L impact as exposures were fully reserved

– Healthcare cashflow represents 2% of portfolio

• Held-for-investment loans of $10.1B, up 20% YoY

– High quality, 100% floating-rate lending portfolio, comprised of 60%

asset-based loans, and ~100% in first lien position

• Limited commercial real estate exposure of $1.1 billion,

entirely within healthcare industry

– Less than 1% of consolidated Ally total loans

Held for Investment Loans

($ billions; EoP)

(1) Non-GAAP financial measure. See pages 34 – 36 for definitions.

For additional footnotes see page 38.

Corporate Finance

Diversified Loan Portfolio

(as of 6/30/23)

Services

All Other

Manufacturing

Key Financials ($ millions) 2Q 23 1Q 23 2Q 22

Net financing revenue 92$ (11)$ 15$

Other revenue 28 (1) 9

Total net revenue 120 (12) 24

Provision for credit losses 15 - 7

Noninterest expense

(2)

33 (12) 5

Pre-tax income

72$ -$ 12$

Change in fair value of equity securities

(3)

(1) (1) (1)

Core pre-tax income

(1)

71$ (1)$ 11$

Total assets (EOP) 10,190$ (36)$ 1,300$

Inc / (Dec) v.

2Q 2023 Preliminary Results

25

Bulk

$0.8 $1.1 $0.02 $0.01 $0.05

• Mortgage pre-tax income of $21 million

– Noninterest expense down $17 million YoY, reflecting the benefit

of partnership DTC origination model

• Direct-to-Consumer (DTC) originations of $267 million,

down 70% YoY, reflective of current environment

• Over 50% of 2Q’23 originations from existing depositors

• Continue to prioritize customer digital experience and

operational efficiency

Held-for-Investment Assets

Direct-to-Consumer Originations

See page 39 for footnotes.

($ billions) ($ billions)

DTC

Bulk

Mortgage Finance

Key Financials ($ millions) 2Q 23 1Q 23 2Q 22

Net financing revenue 53$ (1)$ (3)$

Total other revenue 5 1 1

Total net revenue 58$ -$ (2)$

Provision for credit losses - 1 -

Noninterest expense

(1)

37 (1) (17)

Pre-tax income

21$ -$ 15$

Total assets (EOP) 18,997$ (293)$ (129)$

Mortgage Finance HFI Portfolio 2Q 23 1Q 23 2Q 22

Net Carry Value ($ billions) 18.9$ 19.2$ 18.9$

Wtd. Avg. LTV/CLTV

(2)

54.5% 55.0% 53.7%

Refreshed FICO 782 781 779

Inc / (Dec) v.

2Q 2023 Preliminary Results

26

2023 Financial Outlook

9%

3.4%

5.50%

5.50%

(1) Non-GAAP Financial Measures. See pages 34 – 36 for definitions.

(2) Assumes statutory U.S. Federal tax rate of 21%

Tax Rate

Adj. Noninterest Expense

Peak Fed Funds

YE 2023 Fed Funds

18%

(2)

Retail Auto NCOs

Retail Auto Portfolio Yield (4Q ‘23)

Net Interest Margin

Prior Outlook

Current Outlook

5.25%*

4.50%

1.8%

$4.9B

9%

3.5%

21% - 22%

1.6% - 1.8%

$4.9B

Unemployment Rate (YE ‘23)

Economic Assumptions:

Financial Outlook:

4.2%4.3%

* 3/31 forward curve assumed Fed Funds of 5.25% for one month before easing; 6/30 curve assumes 5.50% peak and no easing in 2023.

$1.9B

Other Revenue

$2.0B

↑100bps

Retail Deposit Portfolio Yield (4Q ‘23)

3.6%

4.1%

(1)

2Q 2023 Preliminary Results

27

Ensure culture remains aligned with relentless focus on customers,

communities, employees, and shareholders

Continue to grow and diversify by scaling existing businesses

Constant evolution to maintain leading digital experiences and brand

Driving disciplined risk management and accretive capital deployment

Delivering sustainable, enhanced results, and value for ALL stakeholders

Differentiate as a financial ally for our consumer and commercial customers

Focused execution on driving long-term value for all stakeholders

Strategic Priorities

2Q 2023 Preliminary Results

28

Supplemental

2Q 2023 Preliminary Results

29

Supplemental

($ millions)

(1) Non-GAAP financial measure. See pages 34 – 36 for definitions.

For additional footnotes see page 39.

Results By Segment

GAAP to Core pre-tax income Walk

Segment Detail 2Q 23 1Q 23 2Q 22 1Q 23 2Q 22

Automotive Finance 501$ 442$ 600$ 59$ (99)$

Insurance 8 92 (122) (84) 130

Dealer Financial Services 509$ 534$ 478$ (25)$ 31$

Corporate Finance 72 72 60 - 12

Mortgage Finance 21 21 6 - 15

Corporate and Other (199) (239) 90 40 (289)

Pre-tax income from continuing operations 403$ 388$ 634$

15$ (231)$

Core OID

(1)

12 11 10 0 2

Change in fair value of equity securities

(2)

(25) (65) 136 40 (161)

Core pre-tax income

(1)

390$ 335$ 780$

56$ (390)$

Inc / (Dec) v.

2Q 2023 Preliminary Results

30

Maturity

Date

Weighted Avg.

Coupon

2023 1.45%

$ 1.20

2024 4.48%

$ 1.45

2025+ 6.25%

$ 8.39

Principal Amount

Outstanding

MMA/OSA/

Checking

Supplemental

(1) Excludes retail notes and perpetual preferred equity; as of 06/30/2023.

(2) Reflects notional value of outstanding bond. Excludes total GAAP OID and capitalized transaction costs.

(3) Weighted average coupon based on notional value and corresponding coupon for all unsecured bonds as of

January 1st of the respective year. Does not reflect weighted average interest expense for the respective year.

Note: Term ABS shown includes funding amounts (notes sold) at new issue and does not include private

offerings sold later. Excludes $2.35 billion of preferred equity issued in 2021. Totals may not foot due to

rounding.

Funding Mix

Unsecured Long-Term Debt Maturities

(1)

Wholesale Funding Issuance

Note: Other includes sweep deposits, mortgage escrow and other deposits. Totals may not foot due to rounding.

Deposit Mix

($ billions)($ billions)

Note: Totals may not foot due to rounding.

Deposits

FHLB / Other

Unsecured

Secured

Retail CD

Brokered /

Other

(2)

(3)

Term ABS

Term

Unsecured

Funding Profile Details

2Q 2023 Preliminary Results

31

Key Financials 2Q 23 1Q 23 1Q 22

Net financing revenue 50$ (47)$ (260)$

Total other revenue 53 46 (6)

Total net revenue 103$ (1)$ (266)$

Provision for credit losses 81 - 13

Noninterest expense 221 (41) 10

Pre-tax income / (loss) (199)$ 40$ (289)$

Core OID

(1)

12 0 2

Change in fair value of equity securities

(3)

- - (0)

Core pre-tax income / (loss)

(1)

(187)$ 40$ (288)$

Cash & securities 35,139$ (520)$ 2,815$

Held for investment loans, net

(4)

3,484 141 1,038

Intercompany loan

(5)

(510) 13 (99)

Other

(5)

7,294 (49) (37)

Total assets 45,407$ (415)$ 3,717$

Ally Invest 2Q 23 1Q 23 2Q 22

Net Funded Accounts (k) 521 523 518

Average Customer Trades Per Day (k) 26.2 29.1 33.7

Total Customer Cash Balances 1,578$ 1,622$ 2,027$

Total Net Customer Assets 14,945$ 14,060$ 13,508

Ally Lending 2Q 23 1Q 23 2Q 22

Gross Originations 436$ 440$ 591$

Held-for-investment Loans (EOP) 2,170$ 2,074$ 1,523$

Portfolio yield 10.0% 10.0% 11.9%

NCO % 5.1% 5.8% 4.0%

Ally Credit Card 2Q 23 1Q 23 2Q 22

Gross Receivable Growth (EOP) 117$ 41$ 189$

Outstanding Balance (EOP) 1,757$ 1,640$ 1,225$

NCO % 8.5% 7.2% 3.8%

Active Cardholders (k) 1,146.1 1,097.2 908.4

Inc / (Dec) v.

• Pre-tax loss of $199 million and Core pre-tax loss of

$187 million

(1)

– Net financing revenue lower YoY driven by higher interest

expense

– Provision expense higher YoY driven by growing asset

balances in unsecured lending

• Total assets of $45.4 billion, up $3.7 billion YoY,

primarily driven by higher cash balances and growth

in unsecured lending balances

Supplemental

Note: Ratings as of 06/30/2023. Our borrowing costs & access to the capital markets could be negatively

impacted if our credit ratings are downgraded or otherwise fail to meet investor expectations or demands.

Ally Financial Rating Details

($ millions)

LT Debt ST Debt Outlook

Fitch BBB- F3 Stable

Moody's Baa3 P-3 Stable

S&P BBB- A-3 Stable

DBRS BBB R-2H Stable

(1) Non-GAAP financial measure. See pages 34 – 36 for definitions.

For additional footnotes see page 39.

Corporate and Other

2Q 2023 Preliminary Results

32

Supplemental

(1) Net financing revenue impacts reflect a rolling 12-month view. See page 37 for additional details.

(2) Gradual changes in interest rates are recognized over 12 months.

($ millions)

Interest Rate Risk

Effective Hedge Notional

Net Financing Revenue Sensitivity Analysis

(1)

Change in interest rates

Gradual

(2)

Instantaneous Gradual

(2)

Instantaneous

-100 bps (109)$ (117)$ (104)$ (117)$

+100 bps 96$ 121$ 94$ 109$

Stable rate environment n/m 36$ n/m (134)$

2Q 23

1Q 23

2Q 23 3Q 23 4Q 23 1Q 24 2Q 24 3Q 24 4Q 24

Retail Auto $21B $16B $12B $12B $11B $11B $11B

AFS Securities $12B $12B $12B $12B $12B $12B $12B

Avg. Pay-Fixed Rate 2.5% 2.9% 3.1% 3.5% 3.9% 4.0% 4.0%

Avg. SOFR 5.0% 5.3% 5.4% 5.3% 4.8% 4.4% 4.2%

2Q 2023 Preliminary Results

33

Deferred Tax Asset / (Liability) Balances

$882

$1,224

$1,071

$1,009

$1,071

$5

$4 $4 $4

$5

2Q 22 3Q 22 4Q 22 1Q 23 2Q 23

Net GAAP DTA Balance Disallowed DTA

(1) GAAP does not prescribe a method for calculating individual elements of deferred taxes for interim periods; therefore, these balances are estimates.

Supplemental

($ millions)

($ millions)

Deferred Tax Asset

Deferred Tax Asset

2Q 23

(1)

1Q 23

Gross DTA

Balance

Valuation

Allowance

Net DTA

Balance

Net DTA

Balance

Net Operating Loss (Federal) 7$ -$ 7$ 261$

Tax Credit Carryforwards 1,061 (516) 545 512

State/Local Tax Carryforwards 310 (129) 181 174

Other Deferred Tax Assets / (Liabilities) 338 - 338 62

Net Deferred Tax Asset 1,716$ (645)$ 1,071$ 1,009$

2Q 2023 Preliminary Results

34

Supplemental

1) Accelerated issuance expense (Accelerated OID) is the recognition of issuance expenses related to calls of redeemable debt.

2) Adjusted earnings per share (Adjusted EPS) is a non-GAAP financial measure that adjusts GAAP EPS for revenue and expense items that are typically strategic in

nature or that management otherwise does not view as reflecting the operating performance of the company. Management believes Adjusted EPS can help the reader

better understand the operating performance of the core businesses and their ability to generate earnings. In the numerator of Adjusted EPS, GAAP net income

attributable to common shareholders is adjusted for the following items: (1) excludes discontinued operations, net of tax, as Ally is primarily a domestic company and sales

of international businesses and other discontinued operations in the past have significantly impacted GAAP EPS, (2) adds back the tax-effected non-cash Core OID, (3)

adjusts for tax-effected repositioning and other which are primarily related to the extinguishment of high cost legacy debt, strategic activities and significant other one-time

items, (4) change in fair value of equity securities, (5) excludes significant discrete tax items that do not relate to the operating performance of the core businesses, and

adjusts for preferred stock capital actions that have been taken by the company to normalize its capital structure, as applicable for respective periods. See page 40 for

calculation methodology and details.

3) Adjusted efficiency ratio is a non-GAAP financial measure that management believes is helpful to readers in comparing the efficiency of its core banking and lending

businesses with those of its peers. See page 43 for calculation details.

(1) In the numerator of Adjusted efficiency ratio, total noninterest expense is adjusted for Rep and warrant expense, Insurance segment expense, and

repositioning and other which are primarily related to the extinguishment of high-cost legacy debt, strategic activities and significant other one-time items, as

applicable for respective periods.

(2) In the denominator, total net revenue is adjusted for Core OID and Insurance segment revenue. See page 23 for the combined ratio for the Insurance

segment which management uses as a primary measure of underwriting profitability for the Insurance segment.

4) Adjusted noninterest expense is a non-GAAP financial measure that adjusts GAAP noninterest expense for repositioning items. Management believes adjusted

noninterest expense is a helpful financial metric because it enables the reader better understand the business' expenses excluding nonrecurring items. See page 45 for

calculation methodology and details.

5) Adjusted other revenue is a non-GAAP financial measure that adjusts GAAP other revenue for OID expenses, repositioning, and change in fair value of equity securities.

Management believes adjusted other revenue is a helpful financial metric because it enables the reader to better understand the business' ability to generate other

revenue. See page 45 for calculation methodology and details.

The following are non-GAAP financial measures which Ally believes are important to the reader of the Consolidated Financial Statements, but which are

supplemental to and not a substitute for GAAP measures: Accelerated issuance expense (Accelerated OID), Adjusted earnings per share (Adjusted EPS),

Adjusted efficiency ratio, Adjusted noninterest expense, Adjusted other revenue, Adjusted tangible book value per share (Adjusted TBVPS), Adjusted total

net revenue, Core net income attributable to common shareholders, Core original issue discount (Core OID) amortization expense, Core outstanding original

issue discount balance (Core OID balance), Core pre-provision net revenue (Core PPNR), Core pre-tax income, Core return on tangible common equity (Core

ROTCE), Investment income and other (adjusted), Net financing revenue (excluding Core OID), Net interest margin (excluding Core OID), Pre-provision net

revenue (PPNR), and Tangible Common Equity. These measures are used by management, and we believe are useful to investors in assessing the

company’s operating performance and capital. For calculation methodology, refer to the Reconciliation to GAAP later in this document.

Notes on Non-GAAP Financial Measures

2Q 2023 Preliminary Results

35

6) Adjusted tangible book value per share (Adjusted TBVPS) is a non-GAAP financial measure that reflects the book value of equity attributable to shareholders even if

Core OID balance were accelerated immediately through the financial statements. As a result, management believes Adjusted TBVPS provides the reader with an

assessment of value that is more conservative than GAAP common shareholder’s equity per share. Adjusted TBVPS generally adjusts common equity for: (1) goodwill and

identifiable intangibles, net of DTLs and (2) tax-effected Core OID balance to reduce tangible common equity in the event the corresponding discounted bonds are

redeemed/tendered. Note: In December 2017, tax-effected Core OID balance was adjusted from a statutory U.S. Federal tax rate of 35% to 21% (“rate”) as a result of

changes to U.S. tax law. The adjustment conservatively increased the tax-effected Core OID balance and consequently reduced Adjusted TBVPS as any acceleration of the

non-cash charge in future periods would flow through the financial statements at a 21% rate versus a previously modeled 35% rate. See page 41 for calculation methodology

and details.

7) Adjusted total net revenue is a non-GAAP financial measure that management believes is helpful for readers to understand the ongoing ability of the company to generate

revenue. For purposes of this calculation, GAAP net financing revenue is adjusted by excluding Core OID to calculate net financing revenue ex. core OID. GAAP other

revenue is adjusted for OID expenses, repositioning, and change in fair value of equity securities to calculate adjusted other revenue. Adjusted total net revenue is calculated

by adding net financing revenue ex. core OID to adjusted other revenue. See page 45 for calculation methodology and details.

8) Core net income attributable to common shareholders is a non-GAAP financial measure that serves as the numerator in the calculations of Adjusted EPS and Core

ROTCE and that, like those measures, is believed by management to help the reader better understand the operating performance of the core businesses and their ability to

generate earnings. Core net income attributable to common shareholders adjusts GAAP net income attributable to common shareholders for discontinued operations net of

tax, tax-effected Core OID expense, tax-effected repositioning and other primarily related to the extinguishment of high-cost legacy debt and strategic activities and significant

other, preferred stock capital actions, significant discrete tax items and tax-effected changes in equity investments measured at fair value, as applicable for respective

periods. See pages 40 and 42 for calculation methodology and details.

9) Core original issue discount (Core OID) amortization expense is a non-GAAP financial measure for OID and is believed by management to help the reader better

understand the activity removed from: Core pre-tax income (loss), Core net income (loss) attributable to common shareholders, Adjusted EPS, Core ROTCE, Adjusted

efficiency ratio, Adjusted total net revenue, and Net financing revenue (excluding Core OID). Core OID is primarily related to bond exchange OID which excludes international

operations and future issuances. Core OID for all periods shown is applied to the pre-tax income of the Corporate and Other segment. See page 45 for calculation

methodology and details.

10) Core outstanding original issue discount balance (Core OID balance) is a non-GAAP financial measure for outstanding OID and is believed by management to help the

reader better understand the balance removed from Core ROTCE and Adjusted TBVPS. Core OID balance is primarily related to bond exchange OID which excludes

international operations and future issuances. See page 45 for calculation methodology and details.

11) Core pre-provision net revenue (Core PPNR) is a non-GAAP financial measure calculated by adding GAAP net financing revenue and GAAP other revenue and

subtracting GAAP noninterest expense then adding Core OID and repositioning expenses, excluding provision for credit losses. Management believes that Core PPNR is a

helpful financial metric because it enables the reader to assess the core business' ability to generate earnings to cover credit losses. See page 45 for calculation

methodology and details.

12) Core pre-tax income is a non-GAAP financial measure that adjusts pre-tax income from continuing operations by excluding (1) Core OID, and (2) change in fair value of

equity securities (change in fair value of equity securities impacts the Insurance and Corporate Finance segments), and (3) Repositioning and other which are primarily

related to the extinguishment of high cost legacy debt, strategic activities and significant other one-time items, as applicable for respective periods or businesses.

Management believes core pre-tax income can help the reader better understand the operating performance of the core businesses and their ability to generate earnings.

See page 44 for calculation methodology and details.

Supplemental

Notes on Non-GAAP Financial Measures

2Q 2023 Preliminary Results

36

13) Core return on tangible common equity (Core ROTCE) is a non-GAAP financial measure that management believes is helpful for readers to better understand the

ongoing ability of the company to generate returns on its equity base that supports core operations. For purposes of this calculation, tangible common equity is adjusted for

Core OID balance and net DTA. Ally’s Core net income attributable to common shareholders for purposes of calculating Core ROTCE is based on the actual effective tax rate

for the period adjusted for significant discrete tax items including tax reserve releases, which aligns with the methodology used in calculating adjusted earnings per share.

See page 42 for calculation details.

(1) In the numerator of Core ROTCE, GAAP net income attributable to common shareholders is adjusted for discontinued operations net of tax, tax-effected Core

OID, tax-effected repositioning and other which are primarily related to the extinguishment of high-cost legacy debt, strategic activities and significant other one-

time items, change in fair value of equity securities, significant discrete tax items, and preferred stock capital actions, as applicable for respective periods.

(2) In the denominator, GAAP shareholder’s equity is adjusted for goodwill and identifiable intangibles net of DTL, Core OID balance, and net DTA.

14) Investment income and other (adjusted) is a non-GAAP financial measure that adjusts GAAP investment income and other for repositioning, and the change in fair value

of equity securities. Management believes investment income and other (adjusted) is a helpful financial metric because it enables the reader to better understand the

business' ability to generate investment income.

15) Net financing revenue excluding core OID is calculated using a non-GAAP measure that adjusts net financing revenue by excluding Core OID. The Core OID balance is

primarily related to bond exchange OID which excludes international operations and future issuances. Management believes net financing revenue ex. Core OID is a helpful

financial metric because it enables the reader to better understand the business' ability to generate revenue. See page 45 for calculation methodology and details.

16) Net interest margin excluding core OID is calculated using a non-GAAP measure that adjusts net interest margin by excluding Core OID. The Core OID balance is

primarily related to bond exchange OID which excludes international operations and future issuances. Management believes net interest margin ex. Core OID is a helpful

financial metric because it enables the reader to better understand the business' profitability and margins. See page 10 for calculation methodology and details.

17) Pre-provision net revenue (PPNR) is a non-GAAP financial measure calculated by adding GAAP net financing revenue and GAAP other revenue then subtracting GAAP

noninterest expense, excluding provision for credit losses. Management believes that PPNR is a helpful financial metric because it enables the reader to assess the

business’ ability to generate earnings to cover credit losses and as it is utilized by Federal Reserve's approach to modeling within the Supervisory Stress Test Framework

that generally follows U.S. generally accepted accounting principles (GAAP) and includes a calculation of PPNR as a component of projected pre-tax net income. See page

45 for calculation methodology and details.

18) Tangible Common Equity is a non-GAAP financial measure that is defined as common stockholders’ equity less goodwill and identifiable intangible assets, net of deferred

tax liabilities. Ally considers various measures when evaluating capital adequacy, including tangible common equity. Ally believes that tangible common equity is important

because we believe readers may assess our capital adequacy using this measure. Additionally, presentation of this measure allows readers to compare certain aspects of

our capital adequacy on the same basis to other companies in the industry. For purposes of calculating Core return on tangible common equity (Core ROTCE), tangible

common equity is further adjusted for Core OID balance and net deferred tax asset. See page 42 for calculation methodology and details.

Supplemental

Notes on Non-GAAP Financial Measures

2Q 2023 Preliminary Results

37

Supplemental

1) Change in fair value of equity securities impacts the Insurance, Corporate Finance and Corporate and Other segments. The change reflects fair value adjustments to

equity securities that are reported at fair value. Management believes the change in fair value of equity securities should be removed from select financial measures because

it enables the reader to better understand the business’ ongoing ability to generate revenue and income.

2) Customer retention rate is the annualized 3-month rolling average of 1 minus the monthly attrition rate; excludes escheatment.

3) Estimated impact of CECL on regulatory capital per final rule issued by U.S. banking agencies - In December 2018, the FRB and other U.S. banking agencies

approved a final rule to address the impact of CECL on regulatory capital by allowing BHCs and banks, including Ally, the option to phase in the day-one impact of CECL

over a three-year period. In March 2020, the FRB and other U.S. banking agencies issued an interim final rule that became effective on March 31, 2020 and provided an

alternative option for banks to temporarily delay the impacts of CECL, relative to the incurred loss methodology for estimating the allowance for loan losses, on regulatory

capital. A final rule that was largely unchanged from the March 2020 interim final rule was issued by the FRB and other U.S. banking agencies in August 2020, and became

effective in September 2020. For regulatory capital purposes, these rules permitted us to delay recognizing the estimated impact of CECL on regulatory capital until after a

two-year deferral period, which for us extended through December 31, 2021. Beginning on January 1, 2022, we are required to phase in 25% of the previously deferred

estimated capital impact of CECL, with an additional 25% to be phased in at the beginning of each subsequent year until fully phased in by the first quarter of 2025. Under

these rules, firms that adopt CECL and elect the five-year transition will calculate the estimated impact of CECL on regulatory capital as the day-one impact of adoption plus

25% of the subsequent change in allowance during the two-year deferral period, which according to the final rule approximates the impact of CECL relative to an incurred

loss model. We adopted this transition option during the first quarter of 2020, and beginning January 1, 2022 are phasing in the regulatory capital impacts of CECL based on

this five-year transition period.

4) Estimated retail auto originated yield is a financial measure determined by calculating the estimated average annualized yield for loans originated during the period. At

this time there currently is no comparable GAAP financial measure for Estimated Retail Auto Originated Yield and therefore this forecasted estimate of yield at the time of

origination cannot be quantitatively reconciled to comparable GAAP information.

5) Interest rate risk modeling – We prepare our forward-looking baseline forecasts of net financing revenue taking into consideration anticipated future business growth,

asset/liability positioning, and interest rates based on the implied forward curve. The analysis is highly dependent upon a variety of assumptions including the repricing

characteristics of retail deposits with both contractual and non-contractual maturities. We continually monitor industry and competitive repricing activity along with other

market factors when contemplating deposit pricing actions. Please see our SEC filings for more details.

6) Net charge-off ratios are calculated as annualized net charge-offs divided by average outstanding finance receivables and loans excluding loans measured at fair value

and loans held-for-sale.

7) Repositioning is primarily related to the extinguishment of high-cost legacy debt, strategic activities, and significant other one-time items.

8) U.S. consumer auto originations

▪ New Retail – standard and subvented rate new vehicle loans; Lease – new vehicle lease originations; Used – used vehicle loans; Growth – total originations from

non-GM/Stellantis dealers and direct-to-consumer loans. Note: Stellantis N.V. (“Stellantis”) announced January 17, 2021, following completion of the merger of

Peugeot S.A. (“Groupe PSA”) and Fiat Chrysler Automobiles N.V. (“FCA”) on January 16, 2021, the combined company was renamed Stellantis; Nonprime –

originations with a FICO® score of less than 620

Notes on Other Financial Measures

2Q 2023 Preliminary Results

38

(1) ‘Prime Auto Lender’ - Source: PIN Navigator Data & Analytics, a business division of J.D. Power. The credit scores provided within these reports have been provided by FICO® Risk

Score, Auto 08 FICO® is a registered trademark of Fair Isaac Corporation in the United States and other countries. Ally management defines retail auto market segmentation (unit

based) for consumer automotive loans primarily as those loans with a FICO® Score (or an equivalent score) at origination by the following:

• Super-prime 720+, Prime 620 – 719, Nonprime less than 620

(2) ‘Bank Floorplan Lender’ - Source: Company filings, including WFC and HBAN.

(3) ‘Retail Auto Loan Outstandings’ - Source: Big Wheels Auto Finance Data 2022.

(4) ‘#1 Dealer Satisfaction among Non-Captive Lenders with Sub-Prime Credit’ - Source: J.D. Power.

Supplemental

Page – 19 | Auto Finance

Page – 17 | Ally Bank: Deposit and Customer Trends

(1) Source: FDIC, FFIEC Call Reports and Company filings of branchless banks including Marcus, Discover, American Express, Synchrony.

Page – 22 | Auto Finance: Agile Market Leader

Page – 23 | Insurance

(2) Acquisition and underwriting expenses includes corporate allocations of $23 million in 2Q 2023, $24 million in 1Q 2023, and $22 million in 2Q 2022.

(3) Change in fair value of equity securities impacts the Insurance segment. The change reflects fair value adjustments to equity securities that are reported at fair value. Management

believes the change in fair value of equity securities should be removed from select financial measures because it enables the reader to better understand the business’ ongoing ability

to generate revenue and income.

(1) Noninterest expense includes corporate allocations of $271 million in 2Q 2023, $271 million in 1Q 2023, and $245 million in 2Q 2022.

Page – 24 | Corporate Finance

(2) Noninterest expense includes corporate allocations of $13 million in 2Q 2023, $15 million in 1Q 2023, and $11 million in 2Q 2022.

(3) Change in fair value of equity securities impacts the Corporate Finance segment. The change reflects fair value adjustments to equity securities that are reported at fair value.

Management believes the change in fair value of equity securities should be removed from select financial measures because it enables the reader to better understand the business’

ongoing ability to generate revenue and income.

Additional Notes

Page – 5 | Purpose-Driven Culture

(1) Scores and rankings as measured by a third-party (Glint).

(2) Digital interactions represent the number of online and mobile logins year-to-date across consumer auto (excluding SmartAuction, Insurance and consumer asset management), Ally

Credit Card, Ally Home, Ally Invest.

(3) Ally Bank customer satisfaction rate as of 2Q ‘23.

(4) Customer retention rate is the annualized 3-month rolling average of 1 minus the monthly attrition rate; excludes escheatment.

2Q 2023 Preliminary Results

39

(1) Noninterest expense includes corporate allocations of $24 million in 2Q 2023, $24 million in 1Q 2023, and $30 million in 2Q 2022.

(2) 1st lien only. Updated home values derived using a combination of appraisals, Broker price opinion (BPOs), Automated Valuation Models (AVMs) and Metropolitan Statistical Area (MSA)

level house price indices.

Supplemental

Page – 31 | Corporate and Other

(2) Repositioning and other which are primarily related to the extinguishment of high-cost legacy debt, strategic activities and significant other one-time items, as applicable for respective

periods or businesses.

(3) Change in fair value of equity securities impacts the Corporate and Other segments. The change reflects fair value adjustments to equity securities that are reported at fair value.

Management believes the change in fair value of equity securities should be removed from select financial measures because it enables the reader to better understand the business’

ongoing ability to generate revenue and income.

(4) HFI legacy mortgage portfolio, HFI Ally Lending portfolio and HFI Ally Credit Card portfolio.

(5) Intercompany loan related to activity between Insurance and Corporate for liquidity purposes from the wind down of the Demand Notes program. Includes loans held-for-sale.

(2) Change in fair value of equity securities impacts the Insurance, Corporate Finance and Corporate and Other segments. The change reflects fair value adjustments to equity securities

that are reported at fair value. Management believes the change in fair value of equity securities should be removed from select financial measures because it enables the reader to

better understand the business’ ongoing ability to generate revenue and income.

(3) Repositioning and other which are primarily related to the extinguishment of high-cost legacy debt, strategic activities and significant other one-time items, as applicable for respective

periods or businesses.

Page – 29 | Results by Segment

Page – 25 | Mortgage Finance

Additional Notes

2Q 2023 Preliminary Results

40

Adjusted Earnings per Share ("Adjusted EPS")

2Q 23 1Q 23 4Q 22 3Q 22 2Q 22 1Q 22 4Q 21 3Q 21 2Q 21 1Q 21 4Q 20 3Q 20 2Q 20

Numerator ($ millions)

GAAP net income attributable to common shareholders 301$ 291$ 251$ 272$ 454$ 627$ 624$ 683$ 900$ 796$ 687$ 476$ 241$

Discontinued operations, net of tax - 1 - 1 - - 6 - (1) - - - 1

Core OID 12 11 11 11 10 10 9 9 9 10 9 9 9

Repositioning Items - - 57 20 - - 107 52 70 - - - 50

Change in fair value of equity securities (25) (65) (49) 62 136 66 (21) 65 (19) (17) (111) (13) (90)

Tax on Core OID, Repo & change in fair value of equity securities

(assumes 21% tax rate) 3 11 (4) (20) (31) (16) (20) (26) (13) 1 21 1 17

Significant discrete tax items - - 61 - - - - - (78) - - - -

Core net income attributable to common shareholders [a] 291$ 250$ 327$ 346$ 570$ 687$ 705$ 782$ 868$ 790$ 606$ 473$ 228$

Denominator

Weighted-average common shares outstanding - (Diluted, thousands)

[b]

304,646 303,448 303,062 310,086 324,027 337,812 348,666 361,855 373,029 377,529 378,424 377,011 375,762

Metric

GAAP EPS 0.99$ 0.96$ 0.83$ 0.88$ 1.40$ 1.86$ 1.79$ 1.89$ 2.41$ 2.11$ 1.82$ 1.26$ 0.64$

Discontinued operations, net of tax - 0.00 - 0.00 - - 0.02 - (0.00) - - - 0.00

Core OID 0.04 0.04 0.04 0.03 0.03 0.03 0.03 0.03 0.02 0.03 0.02 0.02 0.02

Change in fair value of equity securities (0.08) (0.21) (0.16) 0.20 0.42 0.19 (0.06) 0.18 (0.05) (0.04) (0.29) (0.04) (0.24)

Repositioning Items - - 0.19 0.06 - - 0.31 0.14 0.19 - - - 0.13

Tax on Core OID, Repo & change in fair value of equity securities

(assumes 21% tax rate) 0.01 0.04 (0.01) (0.06) (0.09) (0.05) (0.06) (0.07) (0.03) 0.00 0.06 0.00 0.05

Significant discrete tax items - - 0.20 - - - - - (0.21) - - - -

Adjusted EPS [a] / [b] 0.96$ 0.82$ 1.08$ 1.12$ 1.76$ 2.03$ 2.02$ 2.16$ 2.33$ 2.09$ 1.60$ 1.25$ 0.61$

QUARTERLY TREND

Supplemental

GAAP to Core Results: Adjusted EPS

2Q 2023 Preliminary Results

41

Supplemental

Calculated Impact to Adjusted TBVPS from CECL Day-1

1Q 20

Numerator ($ billions)

Adjusted tangible book value 12.2$

CECL Day-1 impact to retained earnings, net of tax 1.0

Adjusted tangible book value less CECL Day-1 impact [a] 13.3$

Denominator

Issued shares outstanding (period-end, thousands) [b] 373,155

Metric

Adjusted TBVPS 32.8$

CECL Day-1 impact to retained earnings, net of tax per share 2.7

Adjusted tangible book value, less CECL Day-1 impact per share [a] / [b] 35.5$

Ally adopted CECL on January 1, 2020. Upon implementation of CECL Ally recognized a reduction to our opening retained earnings balance of approximately $1.0 billion, net of income

tax, which reflects a pre-tax increase to the allowance for loan losses of approximately $1.3 billion. This increase is almost exclusively driven by our consumer automotive loan portfolio.

GAAP to Core Results: Adjusted TBVPS

Adjusted Tangible Book Value per Share ("Adjusted TBVPS")

2Q 23 1Q 23 4Q 22 3Q 22 2Q 22 1Q 22 4Q 21 3Q 21 2Q 21 1Q 21 4Q 20 3Q 20 2Q 20

Numerator ($ billions)

GAAP shareholder's equity 13.5$ 13.4$ 12.9$ 12.4$ 14.0$ 15.4$ 17.1$ 17.3$ 17.5$ 14.6$ 14.7$ 14.1$ 13.8$

less: Preferred equity (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) - - - -

GAAP common shareholder's equity 11.2$ 11.1$ 10.5$ 10.1$ 11.7$ 13.1$ 14.7$ 15.0$ 15.2$ 14.6$ 14.7$ 14.1$ 13.8$

Goodwill and identifiable intangibles, net of DTLs (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.4) (0.4) (0.4) (0.4) (0.4) (0.4)

Tangible common equity 10.3 10.2 9.6 9.2 10.7 12.2 13.8 14.6 14.8 14.2 14.3 13.7 13.4

Tax-effected Core OID balance

(assumes 21% tax rate) (0.6) (0.7) (0.7) (0.7) (0.7) (0.7) (0.7) (0.7) (0.8) (0.8) (0.8) (0.8) (0.8)

Adjusted tangible book value [a] 9.7$ 9.5$ 9.0$ 8.5$ 10.1$ 11.5$ 13.1$ 13.9$ 14.1$ 13.4$ 13.5$ 12.9$ 12.6$

Denominator

Issued shares outstanding (period-end, thousands) [b] 301,619 300,821 299,324 300,335 312,781 327,306 337,941 349,599 362,639 371,805 374,674 373,857 373,837

Metric

GAAP shareholder's equity per share 44.9$ 44.5$ 43.0$ 41.4$ 44.7$ 47.1$ 50.5$ 49.5$ 48.3$ 39.3$ 39.2$ 37.8$ 37.0$

less: Preferred equity per share 7.7 7.7 7.8 7.7 7.4 7.1 6.9 6.6 6.4 - - - -

GAAP common shareholder's equity per share 37.2$ 36.7$ 35.2$ 33.7$ 37.3$ 40.0$ 43.6$ 42.8$ 41.9$ 39.3$ 39.2$ 37.8$ 37.0$

Goodwill and identifiable intangibles, net of DTLs per share (2.9) (3.0) (3.0) (3.0) (2.9) (2.8) (2.8) (1.1) (1.0) (1.0) (1.0) (1.0) (1.0)

Tangible common equity per share 34.2 33.8 32.2 30.6 34.3 37.1 40.8 41.8 40.9 38.3 38.2 36.7 35.9

Tax-effected Core OID balance

(assumes 21% tax rate) per share (2.1) (2.2) (2.2) (2.2) (2.2) (2.1) (2.1) (2.0) (2.1) (2.2) (2.2) (2.2) (2.2)

Adjusted tangible book value per share [a] / [b] 32.1$ 31.6$ 30.0$ 28.4$ 32.2$ 35.0$ 38.7$ 39.7$ 38.8$ 36.2$ 36.1$ 34.6$ 33.7$

QUARTERLY TREND

2Q 2023 Preliminary Results

42

Core Return on Tangible Common Equity ("Core ROTCE")

2Q 23 1Q 23 4Q 22 3Q 22 2Q 22 1Q 22 4Q 21 3Q 21 2Q 21 1Q 21 4Q 20 3Q 20 2Q 20

Numerator ($ millions)

GAAP net income attributable to common shareholders 301$ 291$ 251$ 272$ 454$ 627$ 624$ 683$ 900$ 796$ 687$ 476$ 241$

Discontinued operations, net of tax - 1 - 1 - - 6 - (1) - - - 1

Core OID 12 11 11 11 10 10 9 9 9 10 9 9 9

Repositioning Items - - 57 20 - - 107 52 70 - - - 50

Change in fair value of equity securities (25) (65) (49) 62 136 66 (21) 65 (19) (17) (111) (13) (90)

Tax on Core OID, Repo & change in fair value of equity securities

(assumes 21% tax rate) 3 11 (4) (20) (31) (16) (20) (26) (13) 1 21 1 17

Significant discrete tax items & other - - 61 - - - - - (78) - - - -

Core net income attributable to common shareholders [a] 291$ 250$ 327$ 346$ 570$ 687$ 705$ 782$ 868$ 790$ 606$ 473$ 228$

Denominator (Average, $ billions)

GAAP shareholder's equity 13.5$ 13.1$ 12.6$ 13.2$ 14.7$ 16.2$ 17.2$ 17.4$ 16.1$ 14.7$ 14.4$ 14.0$ 13.7$

less: Preferred equity (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) (2.3) (1.2) - - - -

GAAP common shareholder's equity 11.1$ 10.8$ 10.3$ 10.9$ 12.4$ 13.9$ 14.8$ 15.1$ 14.9$ 14.7$ 14.4$ 14.0$ 13.7$

Goodwill & identifiable intangibles, net of deferred tax liabilities ("DTLs") (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.7) (0.4) (0.4) (0.4) (0.4) (0.4) (0.4)

Tangible common equity 10.2$ 9.9$ 9.4$ 10.0$ 11.4$ 13.0$ 14.2$ 14.7$ 14.5$ 14.3$ 14.0$ 13.6$ 13.3$

Core OID balance (0.8) (0.8) (0.8) (0.9) (0.9) (0.9) (0.9) (0.9) (1.0) (1.0) (1.0) (1.0) (1.1)

Net deferred tax asset ("DTA") (1.1) (1.1) (1.2) (1.1) (0.8) (0.4) (0.6) (0.9) (0.6) (0.1) (0.1) (0.1) (0.2)

Normalized common equity [b] 8.4$ 8.0$ 7.4$ 8.0$ 9.8$ 11.7$ 12.7$ 12.9$ 13.0$ 13.1$ 12.9$ 12.4$ 12.0$

Core Return on Tangible Common Equity [a] / [b] 13.9% 12.5% 17.6% 17.2% 23.2% 23.6% 22.1% 24.2% 26.7% 24.1% 18.7% 15.2% 7.6%

QUARTERLY TREND

Supplemental

GAAP to Core Results: Core ROTCE

2Q 2023 Preliminary Results

43

Supplemental

GAAP to Core Results: Adjusted Efficiency Ratio

Adjusted Efficiency Ratio

2Q 23 1Q 23 4Q 22 3Q 22 2Q 22

Numerator ($ millions)

GAAP noninterest expense 1,249$ 1,266$ 1,266$ 1,161$ 1,138$

Insurance expense (358) (315) (286) (290) (300)

Repositioning items - - (57) (20) -

Adjusted noninterest expense for efficiency ratio [a] 891$ 951$ 923$ 851$ 838$

Denominator ($ millions)

Total net revenue 2,079$ 2,100$ 2,201$ 2,016$ 2,076$

Core OID 12 11 11 11 10

Repositioning items - - - - -

Insurance revenue (366) (407) (387) (260) (178)

Adjusted net revenue for the efficiency ratio [b] 1,725$ 1,704$ 1,825$ 1,767$ 1,908$

Adjusted Efficiency Ratio [a] / [b] 51.7% 55.8% 50.6% 48.2% 43.9%

QUARTERLY TREND

2Q 2023 Preliminary Results

44

Supplemental

(1) Non-GAAP line items walk to Core pre-tax income, a non-GAAP financial measure that adjusts pre-tax income. See page 35 for definition.

Note: Change in fair value of equity securities impacts the Insurance, Corporate Finance and Corporate and Other segments. The change reflects fair value adjustments to equity securities that are reported at fair

value. Management believes the change in fair value of equity securities should be removed from select financial measures because it enables the reader to better understand the business’ ongoing ability to generate

revenue and income.

Non-GAAP Reconciliation: Core Income

($ millions)

GAAP

Core OID

Change in fair

value of equity

securities